Comments (3)

Stephen Walker

Well explained

Alex Thomson

Interesting read

Sam Bowden

Cash can escape into the shadows

The standard argument for government regulators who supervise the extent of bank risk is that if banks take on too much risk in the pursuit of short-term profits, but also raise the risk of becoming insolvent, there are dangers not just to the banks themselves, but also risk to to bank depositors, the supply of credit in the economy, and other intertwined financial institutions.

To put it another way, if the government is likely to end up bailing out individuals, firms, or the economy itself, then the government has a reason to check on how much risk is being taken.

But what if countries start to load up the bank regulators with a few other goals at the same time? What tradeoffs might emerge? Sasin Kirakul, Jeffery Yong, and Raihan Zamil describe the situation in "The universe of supervisory mandates – total eclipse of the core?" (Financial Stability Institute Insights on policy implementation No 30, March 2021).

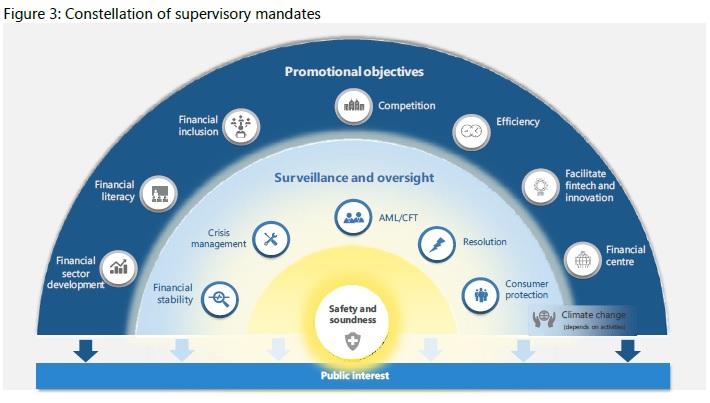

Specifically, they look at bank regulators across 27 jurisdictions. In about half of these, the central bank also has the job of bank supervision; in the other half, a separate regulatory agency has the job. In all these jurisdictions, the bank regulators are to focus on "safety and soundness. But the authors identify 13 other jobs that are simultaneously being assigned to bank regulators--and they note that most bank regulators have at least 10 of these other jobs. They suggest visualizing the responsibilities with this diagram:

The basic goal of supporting the public interest is at the bottom, with the core idea of safety and soundness of banking institutions right above. This is surrounded by five of what they call "surveillance and oversight" goals: financial stability; crisis management; AML/CFT, which stands for anti-money laundering/combating the financing of terrorism; resolution, which refers to closing down insolvent banks, and consumer protection. The outer semicircle then includes seven "promotional objective, which refers to promoting financial sector development, financial literacy, financial inclusion, competition in the financial sector, efficiency, facilitating financial technology and innovation, and positioning the domestic market as an international financial center. Then off to the right you see "climate change," which can be viewed as either an oversight/surveillance goal (that is, are banks and financial institutions taking these risks into account) or a promotional goal (is sufficient capital flowing to this purpose).

There are ongoing efforts to add just a few more items to the list. For example, some economists at the IMF have argued that central banks like the Federal Reserve should go beyond the monetary policy issues of looking at employment, inflation, and interest rates, and also beyond the financial regulation responsibilities that many of them already face, and should also look at trying to address inequality.

For the United States, the current statutory goals for financial regulators include safety and soundness as well as the first five surveillance and oversight goals--although in the US setting these goals are somewhat divided between different agencies like the Federal Reserve, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Commission. There are also statutory directives for certain agencies to pursue consumer projection and and financial inclusion, and non-statutory mandates to promote financial literacy, fintech/innovation, and to in some way take climate change concerns into account.

In some situations, of course, these other goals can reinforce the basic goal of safety and soundness in banking. In other situations, not so much. For example, during a time of economic crisis, should the financial regulator also be pressing hard to make sure all banks are safe and sound, or should it give them a bit more slack at that time? Does "developing the financial sector" mean building up certain banks to be more profitable, while perhaps charging consumers more? What if promoting fintech/innovation could cause some banks to become weaker, thus reducing their safety and soundness and perhaps leading to less competition? Does the climate change goal involve bank regulators in deciding what particular firms or industries are "safe" or "risky" borrowers, and thus who will receive credit?

There's a standard problem that when you start aiming at many different goals all at once, you often face some tradeoffs between those goals. For example, imagine a person planning a dinner with the following goals: tastes appealing to everyone; also tastes different and interesting; includes fiber, protein, vitamins, all needed nutrients; low calorie; locally sources; easily affordable; can prepare with no more than one hour of cooking time; and freezes well for leftovers. All the goals are worthy ones, and with some effort, one can often find a compromise solution that fits most of them. But you will almost certainly need to do less on some of the goals to make it possible to meet other goals. (Pre-pandemic, one of the last dinner parties my wife and I gave was for guests who between them were vegetarian, gluten-free, dairy- free, and no beans or legumes. Talk about compromises on the menu!)

In the case of the regulators who supervise banks, the more tasks you give them to do, the less attention and energy they will inevitably have for the core "safety and soundness" regulation. Also, more goals typically mean that the regulators have more discretion when trading off one objective against another, and thus it becomes harder to hold them to account. Those who need to aim at a dozen or more different targets are likely to end up missing at least some of them, much of the time.

Well explained

Interesting read

Cash can escape into the shadows

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest