Imagine that an entrepreneur who is running a promising business wants to change over from being a privately-held company and to become a publicly-owned company--that is, to get an infusion of money in exchange for becoming accountable to shareholders. How might this be done?

There have traditionally been two main choices. One option is to have an "initial public offering"--that is, to create stock and sell it to the public. The other option is for the entrepreneur to sell the company to an established firm, thus becoming accountable to the shareholders of that firm. But in the last year or so, a new option has emerged called the SPAC, which stands for "special purpose acquisition company."

The Knowledge@Wharton website recently published "Why SPACs Are Booming" (May 2, 2021), which is a short descriptive overview of a one-hour video presentation called "Understanding SPACs," in which "Wharton finance professors Nikolai Roussanov and Itamar Drechsler explained how SPACs work and their pros and cons for investors. Another useful overview is a paper just called "SPACs," by Minmo Gahng, Jay R. Ritter, and Donghang Zhang (working paper at the SSRN website, last revised March 2, 2021). Let's run through the basic questions here: how does it work, how many are there, why do it, and should investors be worried.

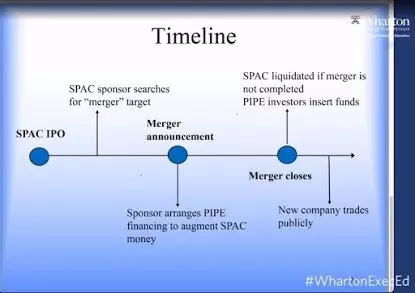

Here's a figure from the Wharton presentation showing the SPAC process.

The first step is to form a SPAC. This is sometimes called a "blank check" company. It is a publicly-listed company--that is, it raises money by having own initial public offering in which it sells shares to investors--but at the start the SPAC doesn't own anything. The company does not have to identify in advance what it plans to do with its money. Presumably, investors buy stock in such a company based on the reputation of those who started it. As the Wharton write-up explains:

From the time a SPAC lists and raises money through an IPO, it has 18 to 24 months to find a private operating company to merge with. If a SPAC can’t find an acquisition target in the given time, it liquidates and returns the IPO proceeds to investors, who could be private equity funds or the general public.

When the SPAC finds a target company, it often seeks out some additional investors known as PIPEs, for "private investors in public equity." If the SPAC fails to merge with the target firm, then investors get their money back. IF the SPAC does merges with the target firm, then the owners of the target firm get a payoff and that target firm now has a set of stockholders.

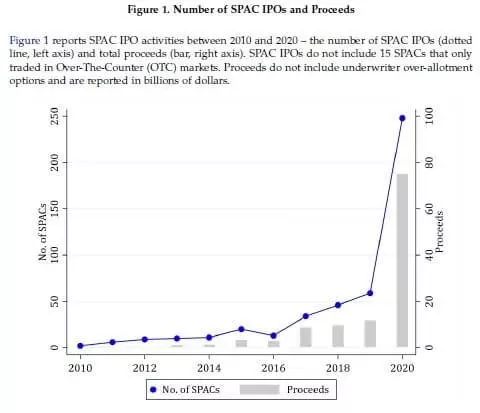

SPACs have taken off lately. Here's a figure from the Gahng, Ritter, and Zhang paper, where the blue dots (left axis) show the number of SPACs and the gray bars (right axis) show the dollar value of the initial public offerings used to form these SPACs. As you can see, SPACs are not brand-new--they have been around for a few years--but the number and volume was gradually rising up through 2019 before taking off in 2020.

Why was the number of SPACs on the rise in 2020? One simple reason is that with stock prices high, more companies are trying to find ways to cash in.

Another reasons involves the regulation of initial public offerings. Specifically, a firm going through an IPO is only allowed to describe its past historical performance, and is forbidden from making forecasts of future earnings. Obviously, this tends to favor somewhat established firms, and to rule out young start-up companies, especially those with little little history and little revenue. The time and energy and cost and regulatory requirements cancel out the benefits. A firm being purchased by a SPAC can make forecasts of future earnings, and the entire process can happen in a couple of months. Similarly, if you are an outside investor who would like to own a diversified portfolio of young start-up companies, hoping that a few of them will hit it big, investing in SPACs gives you the opportunity to do that without having inside connections to venture capitalists, angel investors, or private equity firms.

For a firm thinking about being merged into a SPAC, one main disincentive is that the sponsor of the SPAC typically takes 20% of the value of the original firm as its reimbursement. This does give the sponsor of the SPAC a strong incentive to remain involved and to hellp shepherd the firm toward growth and profitability. But the target firm is in effect giving up 20% of the value of the firm in exchange for the cash infusion.

What are the potential problems with the SPAC approach? The obvious issue is that an investor in a SPAC is essentially trusting the SPAC to make a smart decision about which firm to merge with, and at what price, and additional trusting the SPAC management to keep pushing the firm forward after the merger is completed. When retail investors are looking at promises about what might happen with young firms, and displaying some perhaps irrational exuberance, a less obvious issue is how the IPO for a SPAC is structured for investors. The Wharton write-up explains:

Investors in the IPO of a SPAC typically buy what are called units for $10 each. The unit consists of a common share, which is regular stock, and a derivative called a warrant. Warrants are call options and they allow investors to buy additional shares at specified “exercise” prices. After the merger with the shell company, both the shares and the warrants are listed and traded publicly. If some SPAC investors change their minds and do not want to participate in the merger with the shell company, they could redeem their shares and get back the $10 they paid for each. However, they can retain the warrants.

Yes, you read that correctly. When you buy a "unit" in a SPAC IPO, you can sell back the "unit" at the original purchase price and essentially keep the warrant--that is, the option to purchase stock at a locked-in lower price even if the stock price goes up--for free. The economic justification for this is that it provides an incentive for the SPAC sponsor to negotiate a good deal, because if the deal is perceived to be a bad one, the original money raised by the SPAC could evaporate. The warrants can be viewed as compensation for tying up your funds while the SPAC tries to negotiate a merger with a target firm. But this stock-plus-a-warrant-for-free structure is being criticized within the industry and has come under the eagle eye of regulators, and may not last.

For investors, the past record of SPACs looks good if you are part of the original IPO--that is, one of the people giving the SPAC a blank check--but not especially good if you are buying in as one of the "private investors in public equity" stage. The Gahng, Ritter, and Zhang team reports using data from 2010 up through May 2018: "While SPAC IPO investors have earned 9.3% per year, returns for investors in merged companies are more complex. Depending on weighting methods, they have earned -4.0% to -15.6% in the first year on common shares but 15.6% to 44.3% on warrants."

SPACs in some form seem here to stay, unless the initial public offering rules are revised in a way that works better for young companies without a clear history of revenue growth. But they have now come under regulatory scrutiny. On April 8, John Coates at the Securities and Exchange Commission made a statement on "SPACs, IPOs and Liability Risk under the Securities Laws." He began (footnotes omitted):

Over the past six months, the U.S. securities markets have seen an unprecedented surge in the use and popularity of Special Purpose Acquisition Companies (or SPACs). Shareholder advocates – as well as business journalists and legal and banking practitioners, and even SPAC enthusiasts themselves – are sounding alarms about the surge. Concerns include risks from fees, conflicts, and sponsor compensation, from celebrity sponsorship and the potential for retail participation drawn by baseless hype, and the sheer amount of capital pouring into the SPACs, each of which is designed to hunt for a private target to take public.With the unprecedented surge has come unprecedented scrutiny, and new issues with both standard and innovative SPAC structures keep surfacing.

A few days later the SEC issued "accounting guidance" that made the warrants less attractive, by requiring that they be treated as a liability of the original SPAC. The number of SPACs promptly plummeted. Again, I suspect SPACs aren't going away, but they are definitely an innovation in flux.

Leave your comments

Post comment as a guest