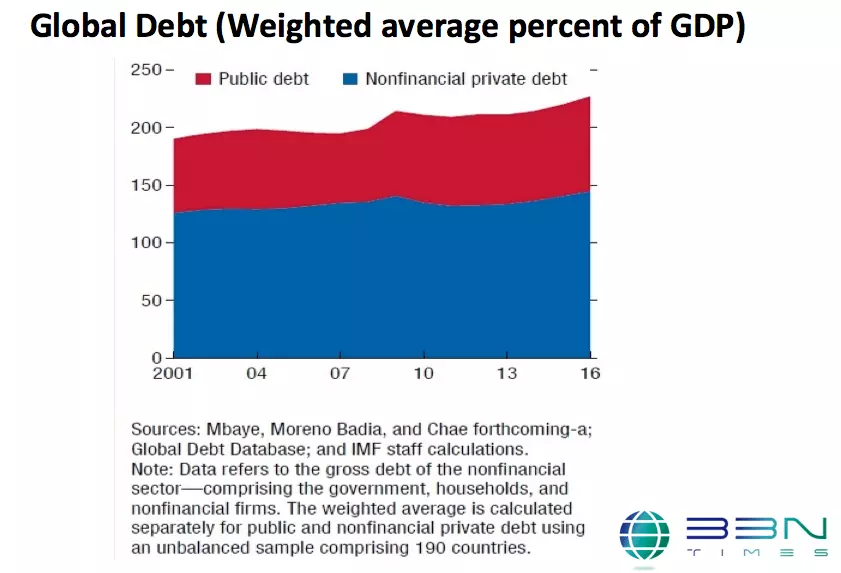

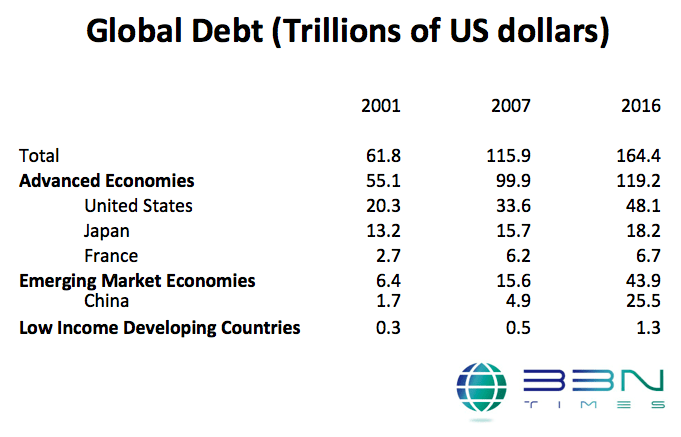

"At $164 trillion—equivalent to 225 percent of global GDP—global debt continues to hit new record highs almost a decade after the collapse of Lehman Brothers. Compared with the previous peak in 2009, the world is now 12 percent of GDP deeper in debt, reflecting a pickup in both public and nonfinancial private sector debt after a short hiatus (Figure 1.1.1). All income groups have experienced increases in total debt but, by far, emerging market economies are in the lead. Only three countries (China, Japan, United States) account for more than half of global debt (Table 1.1.1)—significantly greater than their share of global output."

Thus notes the IMF in the April 2018 issue of Fiscal Monitor (Chapter 1: "Saving for a Rainy Day," Box 1.1, as usual, citations omitted from the quotation above for readability). Here's the figure and the table mentioned in the quotation.

The figure shows public debt in blue and private debt in red. In some ways, the recent increase doesn't stand out dramatically on the figure. But remember that the vertical axis is being measured as a percentage of the world GDP of about $87 trillion, so the rising percentage represents a considerable sum.

Here's an edited version of the table, where I cut a column for 2015. The underlying source is the same as the figure above. As noted above, the US, Japan, and China together account for half of total global debt.

The rise in debt in China is clearly playing a substantial role here. Explicit central government debt in China is not especially high. But corporate debt in China has risen quickly: as the IMF notes of the period since 2009, "China alone explains almost three-quarters of the increase in global private debt."

In addition, China faces a surge of off-budget borrowing from financing vehicles used by local governments, which often feel themselves under pressure to boost their local economic growth. The IMF explains:

"The official debt concept [in China] points to a stable debt profile over the medium term at about 40 percent of GDP. However, a broader concept that includes borrowing by local governments and their financing vehicles (LGFVs) shows debt rising to more than 90 percent of GDP by 2023 primarily driven by rising off-budget borrowing. Rating agencies lowered China’s sovereign credit ratings in 2017, citing concerns with a prolonged period of rapid credit growth and large off-budget spending by LGFVs.

"The Chinese authorities are aware of the fiscal risks implied by rapidly rising off-budget borrowing and undertook reforms to constrain these risks. In 2014, the government recognized as government obligations two-thirds of legacy debt incurred by LGFVs (22 percent of GDP). In 2015, the budget law was revised to officially allow provincial governments to borrow only in the bond market, subject to an annual threshold. Since then, the government has reiterated the ban on off-budget borrowing by local governments, while more strictly regulating the role of the government in public-private partnerships and holding local officials accountable for improper borrowing. Given these measures, the authorities do not consider the LGFV off-budget borrowing as a government obligation under applicable laws.

"There is some uncertainty regarding the degree to which these measures will effectively curb off-budget borrowing. "

An underlying theme of the IMF report is that when an economy is in relatively good times, like the US economy today, it should be figuring out ways to put its borrowing on a downward trend for the next few years. A similar lesson applies to China, where there appears to be some danger that the high levels of borrowing from firms and from local governments are creating future risks.

One old lesson re-learned in the global financial crisis is that high levels of debt can be dangerous. If stock prices rise and then fall, investors will be unhappy that they lost their gains--but for many of them, the gains were only on paper, anyway. But debt is different. If circumstances arises where debts are less likely to be repaid, then financial institutions may well find it hard to raise capital, and will be pressured to cut back on lending. If borrowing was helping to hold asset prices high (including housing, land, or stocks), then a decline in borrowing can cause those asset prices to drop. Lower asset prices make it harder to repay borrowed money, tightening the financial crunch, and slowing an economy further.

When global debt as a share of GDP is hitting an all-time high, it's worth paying attention to the risks involved.

Leave your comments

Post comment as a guest