The US Dollar Index has lost 10% from its March highs and many press comments have started to speculate about the likely collapse of the US Dollar as world reserve currency due to this weakness.

These wild speculations need to be debunked.

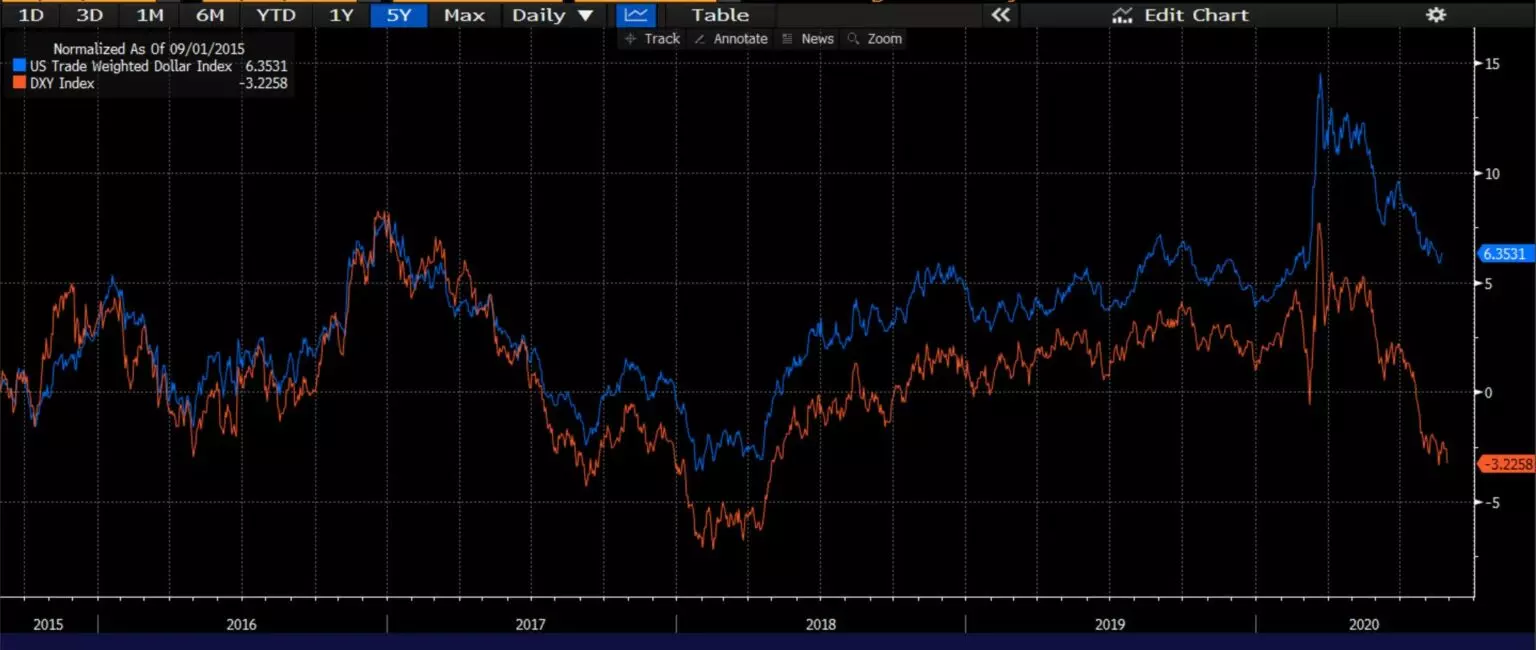

The US Dollar year-to-date (August 2020) has strengthened relative to 96 out of 146 currencies in the Bloomberg universe. In fact, the U.S. Fed Trade-Weighted Broad Dollar Index has strengthened by 2.3% in the same period, according to data compiled by Bloomberg.

The speculation about countries abandoning the U.S. Dollar as reserve currency is easily denied. The Bank Of International Settlements reports in its June 2020 report that global US-dollar denominated debt is at a decade-high. In fact, US-dollar denominated debt issuances year-to-date from emerging markets have reached a new record.

China’s dollar-denominated debt has risen as well in 2020. Since 2015, it has increased 35% while foreign exchange reserves fell 10%.

The US Dollar Index (DXY) shows that the United States currency has only really weakened relative to the yen and the euro, and this is based on optimistic expectations of European and Japanese economic recovery. The Federal Reserve’s dovish announcements may be seen as a cause of the dollar decline, but the evidence shows that the European Central Bank (BOJ) and the Bank Of Japan (BOJ) conduct much more aggressive policies than the U.S. while economic recovery stalls. Recent purchasing manager index (PMI) declines have shown that hopes of a rapid recovery in Europe and Japan are widely exaggerated, and the Daily Activity Index published by Bloomberg confirms it. Furthermore, the balance sheet of the ECB is at the end of August more than 54% of the eurozone GDP and the BOJ´s is 123% versus the Federal Reserve’s 33%.

What we have witnessed between March and August has just been a move back from an overbought exposure to the DXY Index due to the severity of the crisis, as investors increased positions in safe havens in February and March, only to reverse it as markets and the economy recovered.

The lesson most governments should learn is that economies do not become more competitive or deliver stronger growth and exports with a weak currency. Emerging markets have shown in the past years how a weak currency does not help, and the eurozone has had a weak euro vs the US dollar for years just as its economy delivered disappointing growth.

The reason why the US Dollar World Reserve Currency status is not at risk is simple: There are no contenders. The euro has redenomination risk, and the constant political and economic concerns about the union’s solvency make the currency weaken, as the historical performance has shown. It tends to strengthen relative to the US Dollar when investors place unjustified hopes on the eurozone growth only to weaken afterwards when poor growth adds to an overly aggressive ECB policy, with negative rates and massive money supply growth. The yuan cannot become a world reserve currency if the country maintains capital controls and concerns about legal and investor security remain. The China Central Bank (PBOC) is also extremely aggressive for a currency that is only used in 4% of global transactions according to the Bank of International Settlements.

We are living a period of unprecedented financial repression and monetary expansion. The US Dollar reserve status grows in these periods where countries ignore real demand for their domestic currency and decide to copy the Federal Reserve policies without understanding the global demand for their currency. When the tide turns, most central banks find themselves with poor reserves and lower demand for domestic currency risk, and the position of the US dollar as reserve currency strengthens.

This is not a year of US Dollar weakness or the end of its supremacy as reserve currency, what we are witnessing is a generalized fiat currency debasement through extreme monetary policy. That is the reason why gold and silver continue to rise despite hopes of an economic recovery that seems to be stalling. The US Dollar will likely remain the most demanded fiat currency, but the excessive monetary stimulus will ultimately damage the confidence in most fiat currencies.

Leave your comments

Post comment as a guest