Comments

- No comments found

There’s a sort of paradox in the current US labor market.

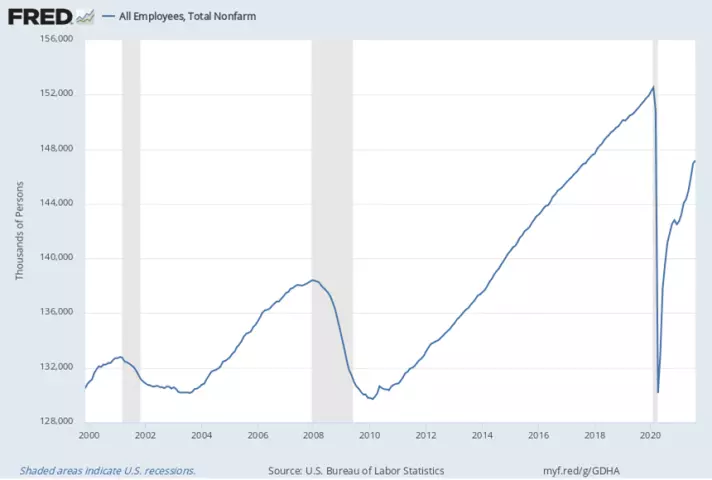

By a standard measure, there is strong demand by employers to hire more workers. By a standard measure, there is a strong supply of workers willing to take these jobs. But even with at first glance appears to be strong demand and supply for labor, the number of jobs remains well below pre-pandemic levels. There’s a simple explanation for this which I’m sure is part of the truth, and a more complex explanation that I suspect is a bigger part of the answer.

A standard measure of demand for labor is the number of job openings. Here’s what it looks like based on data from the Job Openings and Labor Turnover Survey done by the Bureau of Labor Statistics.

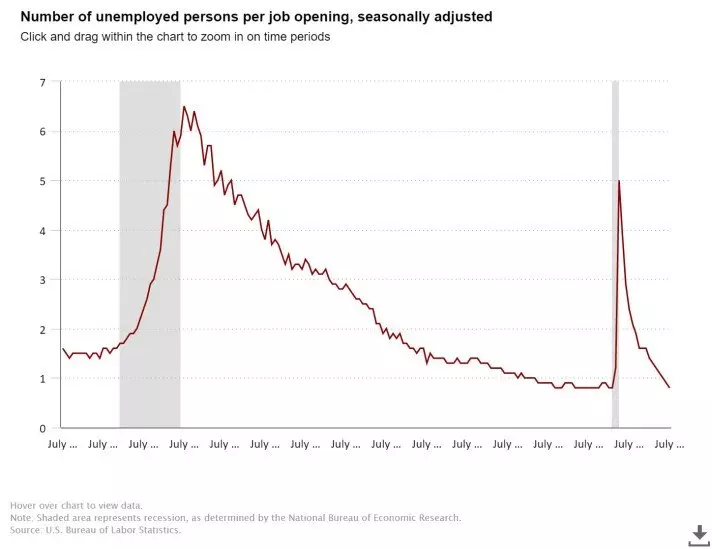

Here’s a figure from the latest JOLTS data, showing the ratio of unemployed workers to job openings. In the latest data, the ratio is 0.8–that is, there are more job openings than unemployed workers.

A standard measure of the willingness of workers to supply labor, perhaps counterintuitively, is to look at the rate at which workers are quitting their jobs. The pattern here is that when jobs are scarce, workers tend to hang on to their existing jobs; when jobs seem plentiful, workers are more likely to quit an existing job because they are headed for a different job. As the figure shows, the number of quits has also been soaring.

The unemployment rate in August was down to 5.2%, which by conventional standards is pretty good. But to be counted as unemployed, you need to be both out of work and also out looking for a job. This definition has its own logic: after all, it wouldn’t make intuitive sense to say that retired adults or adults who are voluntarily staying home looking after children are “unemployed.” But on the other hand, it raises the possibility that there are people who are out of the labor force, in the sense that they are not looking for work, but who were in the labor force not that long ago and might be willing to be in the labor force again. To see the issue, consider the total number of jobs, which despite what looks like lots of job openings and lots of willingness to take those jobs, has not yet recovered to pre-pandemic levels.

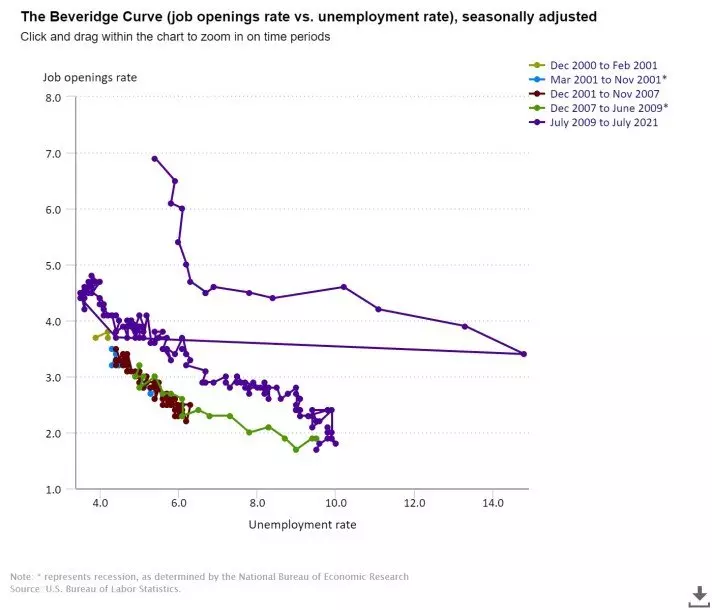

For a vivid illustration of how this combination of patterns represents a break with past labor market patterns, consider what’s called the “Beveridge curve,” which plots the unemployment rate on the horizontal axis and the job openings rate on the vertical axis. The job openings rate is calculated by dividing the number of job openings by the sum of employment and job openings and multiplying that quotient by 100.

There are two ways to characterize the expected pattern here. One is that it will tend to have a downward slope: that is, more job openings will tend to be associated with lower unemployment, and vice versa. The other pattern is that the Beveridge curve will form a loop over time: in a recession, job openings fall and unemployment rises, so the points in the Beveridge curve tend to move down to the right. Then as the economy expands, job openings start rising and the unemployment rate falls, so the month-by-month data moves back up and to the left. (For a couple of previous explanations of the Beveridge curve, see this and this.)

Here’s the most recent Beveridge curve from the JOLTS data. You can see in the pre-pandemic data the generally downward-sloping shape and the loop, as expected. You can also see how the short, sharp two-month pandemic recession just destroyed these patterns. First unemployment shot up with very little change in job openings. Since then, the job openings rate has been climbing to very high levels, and while unemployment has declined, the job openings rate is far higher than at other times when the unemployment rate has been in the range of 5.2%.

What’s going on here? Some explanations are fairly obvious. One is that the stimulus of the US economy through fiscal and monetary policy has been plenty strong to encourage employers to hire, as one can see by the level of job openings. Another is that lots of workers received unemployment payments that did not just replace their earlier earnings, but were substantially above their earlier earnings. These high payments are just now phasing out, but while they lasted, people’s incentives to find and accept a job that would pay less than their benefits was surely muted.

But along with these factors, I suspect something bigger is happening, too. Every recession involves a reorganization and restructuring of the economy. In a standard recession, this involves a larger-than-usual number of companies going broke, and workers needing to scramble for different jobs. But the restructuring in the pandemic recession–and in continuing restructuring in the pandemic that has continued even though the pandemic recession ended back in April 2020–is of a different sort. There are new dividing lines across the labor force like who can work from home, and what sectors of the economy have been more affected by the pandemic on an ongoing basis, and whether parents can rely on sending their children physically off to school. There are concerns about what working environments are more or less safe.

These issues are playing out in different ways across major employment sectors of the economy: health care, education, retail sales, manufacturing. entertainment, tourism, and others. The strange mixture of conditions in the labor market has occurred as millions of potential workers hold their collective breath, and decide when or if they are willing to jump back into the labor market.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest