Valuing companies has always been more art than science and with shares of companies trading at multiples of infinity, should ICOs be revisited and even (gasp) revived?

Parole at 4 pm, regardless of behavior. (Image by Holly Dornak from Pixabay)

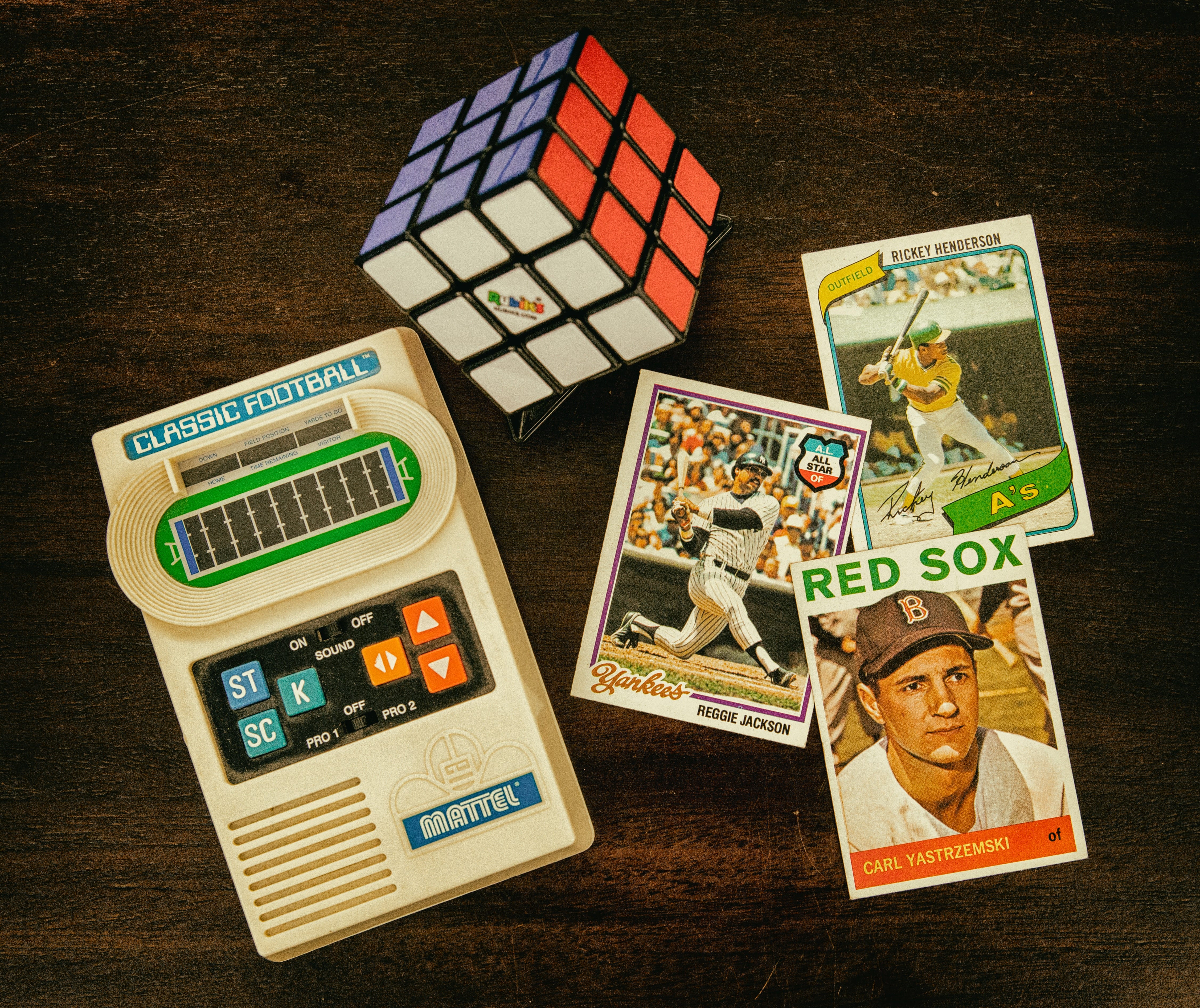

Thomas Myers glanced up at the clock in his classroom wall for what was probably the fifth time in six minutes.

“When was this day ever going to end?” he thought quietly to himself.

As his fourth-grade math teacher droned on about fractions, Myers drifted off to the only thing on his mind at the moment — baseball cards.

Since he was a young boy, Myers had been hooked on collecting and trading baseball cards.

And today was a big day for Myers because the 1952 Topps Mickey Mantle card — his hero — would be released.

As soon as the final bell for school rang, Myers rushed to the corner store and placed down the princely sum of 2 cents for the prized Mickey Mantle card.

From cigarette package inserts designed to both promote the brand as well as prevent the cigarettes themselves from being crushed, baseball cards, small cardboard pieces with the images of baseball players, haven’t always had a cult following.

But the value of baseball cards, especially in the early years, was suspect at best.

Cheap to manufacture and infinitely reproducible, baseball cards were the cardboard equivalent of cryptocurrency.

And as Myers grew up, started a family and had children of his own, he eventually passed down his prized collection of baseball cards to his son, who then passed it on to his son.

With each subsequent generation of Myers men, the care instructions for the prized Topps baseball card collection was simple,

“Take good care of them, they will be worth something someday.”

So when Thomas Myers III finally inherited his grandfather’s prized Topps baseball card collection, including the 1952 Topps Mickey Mantle, he went to have the collection appraised by an expert, expecting it to fetch perhaps only slightly more than its weight in cardboard.

Hall of the 80s had some new exhibits. (Photo by Mick Haupt on Unsplash)

When the professional baseball card appraiser saw Myers’ mint condition 1952 Topps Mickey Mantle, he almost fell off his stool.

“Son do you know how much this card is worth?”

“No sir, I do not.”

“Son, this card alone, excluding the rest of your collection, is worth at least US$2.5 million.”

Thomas Myers III almost fainted.

What were seemingly worthless squares of cardboard, were now worth many times more than their weight in gold.

Sitting in the office of the professional baseball card appraiser, Myers III thought back to what his grandfather used to say,

“Tommy, you have to understand, people often know the price of everything, but the value of nothing.”

Value Is As Value Does

Yet bankers and analysts from London to New York, Mumbai to Moscow and everything in between have for years been hawking the price of shares in the hottest initial public offerings (IPO) as if they were somehow representative of the value, of that which they were selling.

There was a time when being listed on a stock exchange was a badge of honor that needed to be earned, which included years of profits, a proven business model and a credible track record.

Warning: Flashbacks may cause nostalgia. (Image by Виктория Бородинова from Pixabay)

But in the go-go 80s, investment banks such as Merrill Lynch, JP Morgan, and Goldman Sachs started using a new technique called “book-building” to ramp up demand for shares of a company that was about to be listed on the stock exchange in order to pump prices up on their first day of listing.

Rather than only tapping retail investors, investment bankers went on roadshows across the country, pitching blocks of shares to money managers such as Blackrock and Fidelity Investments to increase the pool of capital available to an IPO.

But the “book-building” practice has had a tawdry reputation.

In the late 1990s, during the dotcom boom, investment bankers deliberately underpriced IPOs so that they would rocket in price on the first day of trading.

In exchange for fat fees from the underwriting business, investment bankers would dole out supposedly “hot” IPOs to money managers, who would spin and flip shares of these IPOs for massive returns.

As the spins got bigger and bigger and the stories in the “book” got built higher and higher, price, became more and more disconnected from value.

And as retail investors poured into “hot” technology IPOs, the money managers who were allocated juicy chunks of pre-IPO stocks dumped the same on unwitting retail investors.

Old Dog, Old Tricks

And judging by the string of “hot” IPOs of the past decade, one would be forgiven for thinking that the cloud of reality which had hovered over technology stock IPOs had finally been cleared.

Companies that had never seen a single profitable day in their entire business history were listing on NASDAQ, including the likes of Uber, Snapchat, Lyft, Peloton, leading many to think that profits were no longer necessary as long as the story was big or the investors thick.

But all that changed when investors balked at the prospect of taking on yet another money-burning IPO in the form of WeWork — essentially an office rental firm masquerading as a “hot” technology startup.

After announcing a high profile IPO, WeWork canceled its prospective listing, with the company’s valuation plunging over 90% in as many days from a high of US$104 billion to now barely US$8 billion.

As Softbank, one of WeWork’s key backers scrambled to throw the embattled company a US$9.5 billion lifeline, its founder and now ex-CEO Adam Neumann walked away with a golden handshake while staff at the office rental firm were sent away empty-handed.

More of bricks and mortar business than may appear. (Photo by Eloise Ambursley on Unsplash)

Against that backdrop, vultures started circling for other weakened prey and soon found it in another “hot” IPO — Beyond Meat.

Over the past week, shares in Beyond Meat, till date one of the runaway IPO success stories this year after its stock soared more than ninefold in two months following its stellar listing, have since languished.

Short sellers now account for 47.2% of the plant-based meat substitute group’s freely traded shares — the second-highest ratio in the Russell 1000 index of the biggest U.S.-listed companies.

After a market debut of US$25 a share in May this year, Beyond Meat hit an intraday peak of US$230 in July.

Last week, shares in Beyond meat plummeted below US$100 for the first time since June and now stays well below that level.

And short sales of Beyond Meat’s stock ballooned ahead of the expiry of the company’s “lock-up” period on October 29, which allowed company insiders and pre-IPO investors to dump their holdings for the first time.

Up to 48 million shares or about 80% of Beyond Meat’s outstanding stock become freely traded in the public markets for the first time and traders bet that this would send the stock downwards.

True to form, the market did not disappoint, with shares in the plant-based meat company (if ever there were a greater oxymoron) plummeting over 20% in less than 24 hours.

The pillars in the front are for propping IPO prices up. (Photo by Aditya Vyas on Unsplash)

Given the relatively high price since its IPO, venture capital funds and other early investors are likely to sell their shares in Beyond Meat in the coming days and are likely to continue doing so.

Despite the string of positive announcements from Beyond Meat in the past few months, including McDonald’s testing a plant-based burger in Canada using the firm’s patties, as well as the nationwide rollout of the Beyond Sausage sandwich by Dunkin’, the tide for “hot” money-burning IPOs may have turned, due in no small part to WeWork’s disastrous IPO attempt.

A Confidence Game

And as surely as a butterfly flapping its wings in New Mexico causes a typhoon in China, jitters over pricey and indefinitely unprofitable IPOs are causing the IPO markets in Asia as well to seize up.

PropertyGuru, a KKR-backed property-listing portal that is believed to have raised some US$250 million and sought to list on the Australian Securities Exchange has since abandoned its bid, citing “uncertainty in the current IPO market.”

In the United States, large venture-backed IPOs that raised over US$1 billion, so-called “unicorns” are struggling, with four out of six tradings well below their IPO price and underperforming benchmark indices — including such well-known names as Uber, Lyft, SmileDirectClub and Peloton.

Speaking to Singapore’s Business Times, National University of Singapore Business School associate professor Mak Yuen Teen offers,

“Maybe we will see investors demanding that just because you’re a tech company doesn’t mean you’re that special.”

“Your corporate governance has to be up to scratch.”

But well-funded tech startups may eventually abandon the pursuit of an IPO altogether.

“So if we spend this much of our runway on software, we’ll have this much left to spend on beer.” (Photo by Austin Distel on Unsplash)

Jake Robson, a partner at law firm Morrison and Foerster suggests,

“If they (the startups) carry on doing these fundraising rounds, raising half a billion or a billion dollars at a time, each time with a new series of shares and rights attached to those shares which trump the previous rounds, it gets incredibly difficult to manage.”

Since the first pump of the dot-com bubble, investors at large have always granted technology companies a sort of leeway which has afforded the venture capitalists on Sand Hill road sufficient margins to profit off investor largess.

Because many of these venture capitalists were former technology entrepreneurs themselves, managing these so-called “black boxes” was seen as a higher-order skill that most average investors could not grasp with.

Concepts like “profitability”, “price-to-book ratio”, “break-up value” and “price-to-earnings ratio” were considered antiquated concepts that had little bearing on technology companies that were going to “disrupt the world.”

And while Sand Hill road’s finest are livid at the seeming ignorance of institutional investors to prop up the jaw-dropping valuations of these technology startups, ironically, Wall Street is having a moment of introspection.

Investment banks like Goldman Sachs and Morgan Stanley are now starting to ask whether the traditional IPO, however lucrative for them, remains the best means to bring tech firms to the public markets or to even raise capital for that matter.

Racketeering By Another Name

A typical IPO today starts with a grueling global tour that would make even your most road-hardened rock band throw up.

Starting in a private jet may sound glamorous, but the schedule of meetings and pitches for an IPO is so jam-packed to catch the attention of as many investors as possible and to elicit orders from them — a process known in the business as “building the book.”

For the underwriter of the IPO, the trick is to divine an IPO price that satisfies both the greediest and loudest voices in the company and one which is “value-driven” enough that it whets the appetite of investors, providing a “pop” for the IPO stock on the first day of trading.

“Pssh, are you looking to score some IPO action?” (Image by George Tudor from Pixabay)

Most underwriters play it safe and underprice IPOs despite having a strong incentive to maximize the IPO price — fees can go as high as 7% of the value of the IPO.

But in practice, underwriters tend to underprice the IPO to favor big investor clients, with money managers paying higher trading commissions in exchange for access to the hottest IPOs.

If this predictable, repeatable process sounds familiar, that’s because it is — it’s called a “racket” and the mafia has been running them for decades.

But what are the possible alternatives to an IPO?

Firms have other roads to access public money if they so choose.

One method is to auction shares to the highest bidders as Google did in 2004, selling shares directly in the public markets without underwriters and without raising capital.

But auctions remain unpopular despite Google’s success.

A study conducted by Ann Sherman, of DePaul University in Chicago, Ravi Jagannathan, and Andrei Jirnyi of Northwestern University, found that IPO auctions in 25 countries, including Singapore, Taiwan, and France were all but abandoned.

Another method is a direct listing, which is starting to create a buzz in Silicon Valley.

Well-capitalized startups with healthy balance sheets may favor such listings because they already have lots of cash and no pressing need to raise more through an IPO.

Direct listings, because they don’t require an underwriter, are also far cheaper to execute and allow the sale of lots of shares quickly — the higher levels of liquidity (no lock-up periods) also draw in investors.

“We’ll build a wall and retail investors will pay for it.” (Photo by Rick Tap on Unsplash)

But shares of both Spotify and Slack, which took this route, have languished, which has put off Airbnb which was mulling a direct listing next year.

To be sure, the direct listing route to access public markets has not been unequivocally proven to be paved in gold.

But whatever the method, listing a company requires investors to value that company, which has never been an easy task.

In Devil Take the Hindmost, as far back as Cicero’s time, buying new shares or partes, in ventures fulfilling government contracts was seen, even by the most speculative Romans in ancient times, as a step too far.

Richard Sylla of New York University’s Stern School of Business notes that America’s first public offering in 1781, of the Bank of North America, flopped.

A decade later, that of the Bank of the United States surged like a “hot” stock.

Yet the values of both stocks had more to do with the backdrop of the time than with anything inherent in the companies themselves — the revolutionary war and its buoyant aftermath.

However much anyone re-engineers the process, valuing companies will always be a shot in the dark, which is why it may perhaps be time for a different path.

How should companies raise capital anyway?

IPOs To ICOs?

“When you have eliminated the impossible, whatever remains, however improbable, must be the truth.”

— Sir Arthur Conan Doyle

Make no mistake about it, in the throes of the initial coin offerings (ICOs) wave, the alternative means for startups to raise finance, attracted no shortage of scams and get-rich-quick schemes.

And even the projects that were not scams have struggled to construct commercially viable products or services.

But not all ICOs were bad, just as not all IPOs are bad either.

While many critics derided ICOs as just another vehicle by which to fleece unwitting investors of their monies, it is important to draw a clear distinction between the subject matter and the vehicle.

There have been IPOs as well which were scams — including many from the class of dotcom companies of the late 1990s and early 2000s — but should the experience of a few necessarily tarnish the entire IPO industry as a whole?

I would argue that it ought not.

Similarly, just because ICOs were a vehicle for scams and other schemes should not mean that regulators, investors and startup founders ought to abandon the vehicle altogether.

ICOs at the very least, afforded retail investors the opportunity to profit off the initial rise of a digital token’s issuance.

The ICO process was far cheaper, with almost absent regulatory burdens on unregulated exchanges.

Moving forward of course, this is far from a sustainable way to run ICOs — they do require some degree of regulation, but there are many other advantages to the vehicle.

What Is An ICO Anyway?

For the uninitiated, an ICO is basically the release of a firm’s digital tokens on a blockchain, typically the Ethereum blockchain (many others exist as well), which investors buy using other more liquid cryptocurrencies such as Bitcoin or Ether.

The premise is that the startup will then use these more liquid cryptocurrencies, convert them to fiat currencies as necessary to fund their startup activities and create new products or services, which run off their issued digital token.

Presumably, these same digital tokens issued by the startup ought to appreciate in value, if and when the startup finally rolls out valuable products and services, because the digital tokens themselves could be used to purchase those products or services, sometimes at substantial discounts to what they may be worth.

To understand this in layman terms, consider someone who’s a brilliant hairstylist who wants to set up her own hair salon, but is somewhat strapped for cash to startup.

There was quite a line to see the stylist. (Image by Santa3 from Pixabay)

Now she could go to a bank and get a loan, but given her credit history, she would not be able to find an affordable one. Instead, our hairstylist decides that she will sell coupons for future services at her soon-to-be-built hair salon.

But because people who pre-buy these services are taking the risk that the hair salon may never be built, they need to receive a discount for their early vote of confidence and sometimes these discounts can be quite substantial.

So when our talented hairstylist finally starts up her hair salon with the pre-buys, those who had purchased the coupons can now redeem them for the actual hair services.

Now, and this is an important distinction, under normal circumstances, the hairstylist would also serve other customers who had not committed to pre-buys, but in the case of our hairstylist, she must not do so — this creates a “closed” ecosystem — where the only way for someone to gain access to this hair stylist’s services is to either to buy coupons from the hair salon directly (the issue of these coupons may be infinite or capped), or from existing holders of those coupons.

And if the demand for our hair stylist’s services is particularly robust, the perceived value and therefore the price of those coupons ought to go up as well.

Furthermore, our hairstylist also commits to release only a fixed amount of coupons, ever, which creates scarcity — which in theory should only drive the price of these same coupons higher.

Such was the premise of an ICO — it was a pre-purchase of digital tokens for future products or services that would presumably create demand.

There are of course issues with this model.

As a currency in a closed ecosystem, it is important that the ecosystem itself has no or few alternatives — and this is an important distinction.

In our example above, the reason why the coupons would not rise indefinitely is simply because there is more than one hairstylist in the world.

Similarly, many ICO projects had competitors releasing similar products or offering similar services.

So not all business models would benefit from an ICO.

But few understood this distinction in the heady rush to “moon” or “Lambo” in late 2017 and early 2018.

An ICO For WeWork?

Yet there are some companies that could potentially have raised capital through an ICO and one of these is WeWork.

Although it may not be immediately obvious, WeWork, currently one of the biggest tenants in key cities like New York and London, enjoys certain monopolies that other firms would struggle to replicate.

One of these monopolies is space.

Either you are the landlord of an office space or you are not — the issue is strictly binary.

So if WeWork occupies key office space in downtown Manhattan, no other firm is able to do so.

There may only be one building with the unique qualities that WeWork occupies.

Millions of people work there, but it’s the business model that’s not working. (Photo by Charles Koh on Unsplash)

Against this backdrop, if WeWork were to pre-sell digital tokens that would allow tenants to rent that space, at a substantial discount to what they would pay if they used cash, there would be an immediate demand for such a digital token — because presumably, companies will always need a place to house their employees — not all businesses can be run remotely.

But, and this is an important caveat — the price of WeWork’s digital token would not rise indefinitely or indiscriminately — for starters, the price of the digital token would be calculable because it could not rise such that it becomes more expensive than the nearest, closest competing office space that could be rented with the same amount.

For instance, if it costs (I have taken some liberties here) US$1,000 a month to rent a 200 square foot office space in downtown Manhattan, the value of WeWork’s coins that could rent the equivalent in the next building over could not be more than 10 WeWork coins worth US$100 a piece for the same level of access.

Whilst I am simplifying a lot of other factors here, such as level of service, access, and network, you get the idea.

A WeWork token, as crazy as it may sound, would be a far more efficient way to raise capital in a less speculative model because purchasers of such tokens presumably want to use WeWork’s shared serviced offices.

And since shared office services are not easily replicable for reasons such as location and network, the value of such digital tokens would presumably increase in price — but to a point.

When you consider that the shares of some technology companies are trading at 100 times price to earnings ratios — in other words, investors are paying US$100 for every US$1 of earnings — implying it could take the company as long as a century to pay back that investment — an ICO may not sound so ludicrous after all.

Trippin’ on some crypto. (Photo by Pawel Janiak on Unsplash)

And it’s not just WeWork whose digital tokens would have value, DropBox (a cloud storage company) tokens, Airbnb tokens, Booking.com tokens, basically any business whose services are unique enough or possess a network effect great enough to hold the value of the future use of their tokens — a case could be made for an ICO instead of an IPO — even Facebook — of which Libra is a sort of token issuance.

Corporate finance is changing.

Whereas IPOs used to be the promised land, the WeWork experience has shown that, particularly for cash-burning companies, investors are no longer willing to fund startup proclivity.

And while ICOs may not be a silver bullet either, presumably those which are not scams and which are truly trying to create valuable products or services, would no doubt seek to build that value into the digital tokens they are issuing themselves.

Digital tokens these days bear far more nuances and capabilities than a simple stock.

To be sure, a share, particularly a minority share, has limited value both in terms of decision making as well as control over a company’s activities.

Whereas many digital tokens today come built-in with voting rights on the protocol’s direction, influence over the developmental directions and even in some cases, the supply of the token itself.

These powers far outweigh the purely legal value of a share certificate and many digital tokens today resemble securities with benefits.

Consider that your average retail investor who has a minority share in a listed company basically rides along with whatever decisions a company makes and it’s not difficult to see how a digital token with the same rights as a share, plus influence over development and direction of a blockchain protocol is far more “valuable.”

Add to that the ability to build-in proportional representation to entertain a diversity of views in a token-voting structure and the permutations for ICOs are almost limitless.

WeWork I would argue, was a watershed moment for IPOs, could it be then time to relook ICOs?

Patrick is an innovative entrepreneur and a lawyer passionate about cryptocurrencies and the business world. He is the CEO of Novum Global Technologies, a cryptocurrency quantitative trading firm. He understands the business concerns of founders and business people helping them to utilise the legal framework to structure their companies to take advantage of emerging technologies such as the blockchain in order to reach greater heights. His passion for travel, marketing and brand building has led him across careers and continents. He read law at the National University of Singapore and graduated with Honors in the Upper Division and joined one of Singapore’s top law firms, Allen & Gledhill where he was called to the Singapore Bar as an Advocate & Solicitor in 2005. He created Purer Skin, a skincare and inner beauty company which melds the traditional wisdom of ancient Asian ingredients such as Bird's Nest with modern technology. In 2010, his partner and himself successfully raised $589,000 from the National Research Foundation of Singapore under the Prime Minister’s Office. He has played a key role in the growth of Purer Skin from 11 retail points in Singapore to over 755 retail points in Singapore and 2 overseas in less than a year. He taught himself graphic design, coding, website design and video editing to create the Purer Skin brand and finished his training at a leading Digital Media Company.

Leave your comments

Post comment as a guest