Comments

- No comments found

A stablecoin is a type of cryptocurrency designed to maintain a stable value by pegging it to a reserve of assets or a fiat currency.

Unlike many other cryptocurrencies that experience significant price volatility, stablecoins aim to minimize fluctuations in value, making them more suitable for everyday transactions and a reliable store of value.

One reason why cryptocurrencies like Bitcoin don’t work well as a medium of exchange for typical transactions (along with difficulties like slow transactions and high cost per transaction compared with standard currencies) is that their value fluctuates so much. When a person or a company promised to make or receive a payment in a few weeks or even a few months, it wants to know, in the present, what that payment will be worth.

As a result, a number of companies have been launched to offer “stablecoins.” The goal is to have a cryptocurrency with a fixed and stable value. But how well are they succeeding? Anneke Kosse, Marc Glowka, Ilaria Mattei and Tara Rice provide an overview of stablecoins in “Will the real stablecoin please stand up?” (Bank of International Settlements, November 2023, BIS Papers No 141). The authors point out that stablecoins have four different ways to implement their commitment to have a value that doesn’t rise or fall. They write:

Stablecoins may use various approaches to maintaining parity with their peg. At a high level, a distinction can be made between the following four types of stablecoin based on whether they claim to hold a pool of reserve assets to back their value (ie whether they are collateralised or not), and if so, the type of these reserve assets:

Fiat-backed stablecoins: stablecoins that claim to be backed by assets

denominated in a fiat currency. Examples include Tether and USD Coin.

Crypto-backed stablecoins: stablecoins that claim to be backed by other cryptoassets. Examples include Dai and Frax.

Commodity-backed stablecoins: stablecoins that claim to be backed by

commodities. Examples are PAX Gold and Tether Gold.

Unbacked stablecoins: stablecoins that do not claim to be backed by any reserves, but rather seek to maintain a stable value through, for instance, algorithms or protocols. Examples include TerraClassicUSD and sUSD.

Note that fiat-backed, commodity-backed and crypto-backed stablecoins are sometimes also defined as collateralised stablecoins, with the first two referred to as “off-chain collateralised” and the latter “on-chain collateralised” stablecoins.

The big player in this market is Tether, which is backed by US dollar assets. Indeed, when Bitcoin falls, it’s not unusual for some cryptocurrency investors to shift money into Tether. A prominent unbacked “stablecoin” called TerraUSD at first earned returns of 20% for investors by lending out the stablecoin holdings in a decentralized bank for crypto investors, but then the value of the TerraUSD stablecoins fell to 2% of their original value. The stablecoin market as a whole has also suffered a series of negative news stories–some more directly related to stablecoins, and some not. Here’s an overview of recent events from the BIS authors:

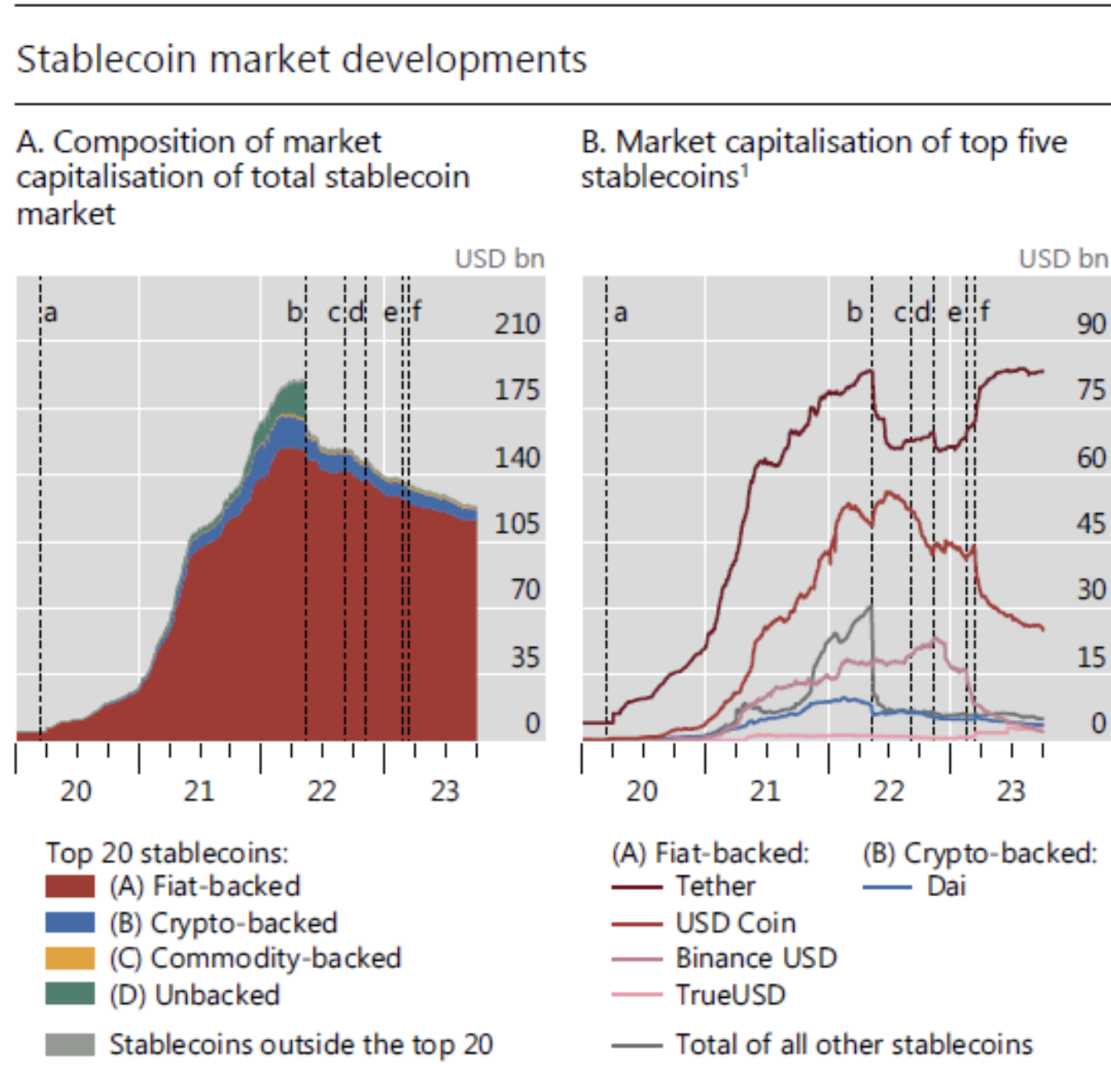

It took several years before stablecoins obtained significant traction (Graph 1). The first stablecoin (BitUSD) was issued in July 2014, and five years later the total market capitalisation had grown to roughly five billion US dollars. It was not until the start of the Covid-19 pandemic that the market capitalisation started to rise steeply (Graph 1.A, event a). This has been attributed to the turbulence in the traditional financial markets following the Covid-19 outbreak and the sharp decline of the price of Bitcoin, which led investors to turn to stablecoins. Over the course of two years, the market capitalisation grew more than ninefold, and in March 2022, it was more than 35 times higher than at the onset of the pandemic.

Most of the growth was driven by a strong increase in the market capitalisation of Tether. Tether was launched in 2014. While it quickly became the largest stablecoin, it started to gain traction only in 2021. Many other stablecoins were also launched during the pandemic: the total number of active stablecoins grew from 13 at the beginning of 2020 to 40 at the end of 2021. Initially, the stablecoin market consisted mainly of fiat-backed stablecoins. However, various stablecoins that entered the market over the course of 2021 were crypto-backed or unbacked stablecoins. In April 2022, fiat-backed stablecoins accounted for around 80% of the total stablecoin market in terms of market capitalisation.

The growth of the stablecoin market came to a halt in the first half of May 2022 when the crypto ecosystem was shaken up by the crash of various cryptoassets. Among these was Terra’s (unbacked) stablecoin “TerraUSD”, the third largest stablecoin at the time (Graph 1.A, event b). TerraUSD’s collapse was caused by its inability to redeem users’ holdings at par. The TerraUSD crash caused unbacked stablecoins to lose almost all of their value. It also undercut the market capitalisation of fiat-backed and crypto-backed stablecoins. Overall, by the end of September 2022, the total market capitalisation of stablecoins had shrunk by more than a fifth to $151.4 billion.

The stablecoin market continued to shrink into 2023. Between April 2022 and the end of January 2023, the total capitalisation of the stablecoin market had shrunk by more than 25% to $138 billion. While much of the fall was triggered by the TerraUSD collapse, the bankruptcy filing of FTX, a major crypto exchange, in November 2022, accelerated the declining trend, although not as strongly as the May turmoil.

The left-hand panel shows a breakdown of the stablecoin market by how the assets are backed: as you can see, those backed by fiat currency (like the US dollar, as is the case with Tether) have most of the market. The right-hand panel shows the top five stablecoins by market size.

The authors emphasize that no stablecoin has yet managed to maintain a truly fixed value. Even Tether “had an average daily price volatility of about 2 percentage points between end-September 2022 and end-September 2023. This shows that to date, no stablecoin has been able to meet an important prerequisite of becoming a safe store of value – guaranteeing full price stability.” Unbacked stablecoins, although a small share of the overall market, can be just as volatile as any non-stablecoin cryptocurrency.

It’s not clear to me that stablecoins have yet evolved in a way that they are more than a niche market. But I’m hoping anyone who plays around with these asset understands that they are not regulated like banks or other traditional financial markets. Some cryptocurrencies that refer to themselves as “stablecoins” are not actually backed by anything. And even the largest and best-known stablecoins can have their value move a few percent in a day.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest