Comments

- No comments found

Back in 2000, the Deputy Governor of the Bank of England, Mervyn King, gave a speech about monetary policy that has been often-quoted by central bankers around the world (“Balancing the Economic See-Saw,” April 14, 2000). He said:

[O]ur ambition at the Bank of England is to be boring. Not, I hasten to add, at events like this. But in our management of the economy where our belief is that boring is best. Macroeconomic policy has, for most of our lifetime, been rather too exciting for comfort. … Our aim is to maintain economic stability. A reputation for being boring is an advantage – credibility of the policy framework helps to dampen the movement of the see-saw. If love is never having to say sorry, then stability is never having to be exciting.

King’s reference to the “see-saw” is pointing out that monetary policy involves movements between looser and tighter monetary policy. Some such movement is inevitable. But of course, the goal is to have the see-saw of macroeconomic policy involve small adjustments, rather than big swings. King argued that central banks should be willing to take small actions sooner, because otherwise they are likely to need to take bigger actions later. He said:

The longer the correction is left, the sharper the required adjustment will be. The higher one end of the see-saw, the greater the subsequent lurch will be. … In one of the most influential contributions to monetary policy in the post-war period, Milton Friedman wrote that the characteristic of most central banks was that “too late and too much has been the general practice”.

The often-heard recent complaint about the Federal Reserve and inflation was that it waited too long after inflation started in 2021, and then had to act more aggressively to raise interest rates starting in 2022 than would otherwise have been needed. The current concern about monetary policy is that perhaps the Fed has already taken sufficient actions to bring down inflation, but it takes some time for the past hike in interest rates to work through the macro-economy. By not waiting to see what happens from its past actions, the Fed runs a risk of overreacting. The best description of this phenomenon that I know come from Alan Blinder, who was vice-chair of the Fed in the mid-1990s. He wrote in a 1997 article in the Journal of Economic Perspectives:

[H]uman beings have a hard time doing what homo economicus does so easily: waiting patiently for the lagged effects of past actions to be felt. I have often illustrated this problem with the parable of the thermostat. The following has probably happened to each of you; it has certainly happened to me. You check in to a hotel where you are unfamiliar with the room thermostat. The room is much too hot, so you turn down the thermostat and take a shower. Emerging 15 minutes later, you find the room still too hot. So you turn the thermostat down another notch, remove the wool blanket, and go to sleep. At about 3 a.m., you awake shivering in a room that is freezing cold …”

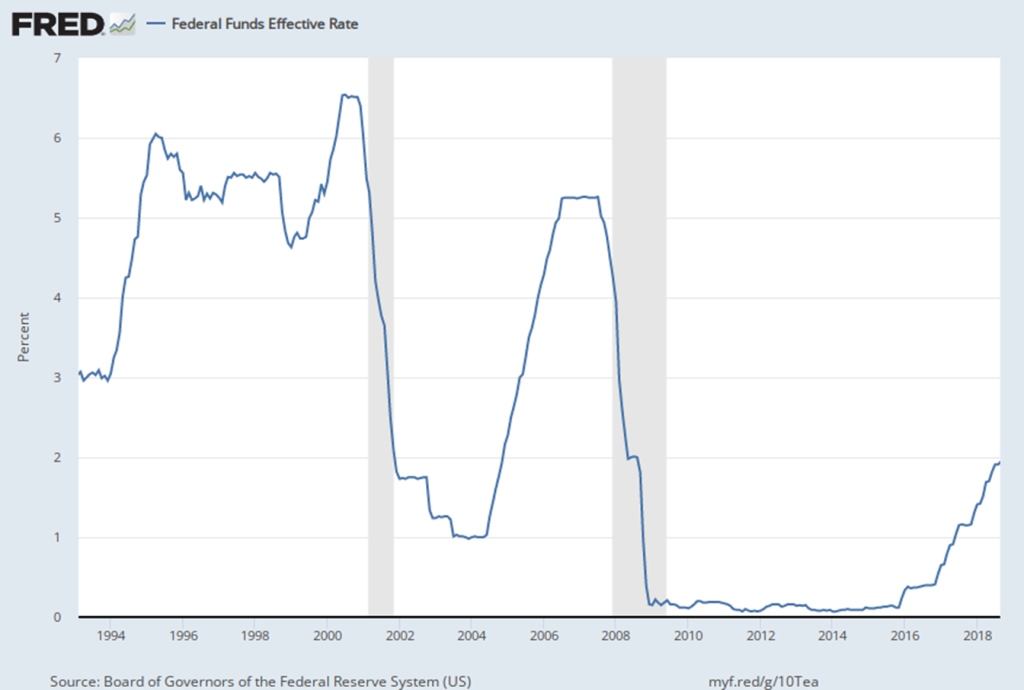

But setting aside the questions of whether the Fed waited too long to act (I think it did) or whether it is currently in danger of overreacting (I think not yet), perhaps the bigger complaint is that when one thinks back over the last 20 years or so of monetary policy, what Mervyn King called the “see-saw” of policy has shown dramatic shifts. It’s not just the rise and fall of the federal funds interest rate–the policy interest rate targeted by the Fed.

It’s also the policies of quantitative easing, due to which the Fed now holds about $8 trillion in Treasury bonds and mortgage-backed securities. I It’s the shift toward the use of “forward guidance,” in which the Fed seeks to shift interest rates and financial conditions in the present by making announcements about the likely course of future Fed policy.

It’s the fact that the Fed has fundamentally shifted its tools of monetary policy policy. A couple of generations of economics students were taught about the three tools of monetary policy: open market operations, reserve requirements, and the discount rate. But the Fed abolished reserve requirements in 2020, and open market operations only worked because banks wanted to avoid not holding enough reserves. Instead of discount rates, the Fed now creates funds for short-term liquidity, which spring up during the Great Recession or the pandemic recession to reassure markets, and then vanish again. The Fed now seeks to control the federal funds interest rate now through payment of interest on bank reserves held at the Fed, which didn’t start until 2008, and using overnight reverse repurchase agreements, which didn’t start until 2013.

One can add to this some of the recent debates over whether the goals of Federal Reserve policy should reach beyond the standard see-saw of balancing risks of unemployment and inflation, and also try to take into account possible effects of monetary and banking regulation policy on issues like inequality and climate change.

Of course, the most recent example of the Fed policy see-saw is the meltdown at Silicon Valley Bank and its aftermath. Apparently, neither the Federal Reserve’s monetary policy arm nor its bank regulation arm managed to notice the elementary fact that a monetary policy decision to raise interest rates would affect the value of fixed-interest-rate bonds held by banks (as well as the value of similar assets held by the Fed itself). As a result, the Fed ended up making a rather sudden decision to guarantee all bank deposits , even those above the previous limit of $250,000, at certain “strategic” banks–a guarantee which in practice seems likely to apply to just about any bank in trouble.

It remains true in 2023, as Mervyn King said back in 2000: “Macroeconomic policy has, for most of our lifetime, been rather too exciting for comfort.” I have a reasonably good understanding of the reasons and rationales for the various Fed policy changes in the last 20 years. But it’s worth remembering King’s other ambition as well: The Federal Reserve, along with other central banks around the world, needs to be more boring.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest