Comments

- No comments found

Understanding the complex world of sales tax in the online economy has become a significant challenge for businesses.

With the rise of e-commerce, the issue of whether online sellers should be required to collect and remit state sales tax has become a subject of debate.

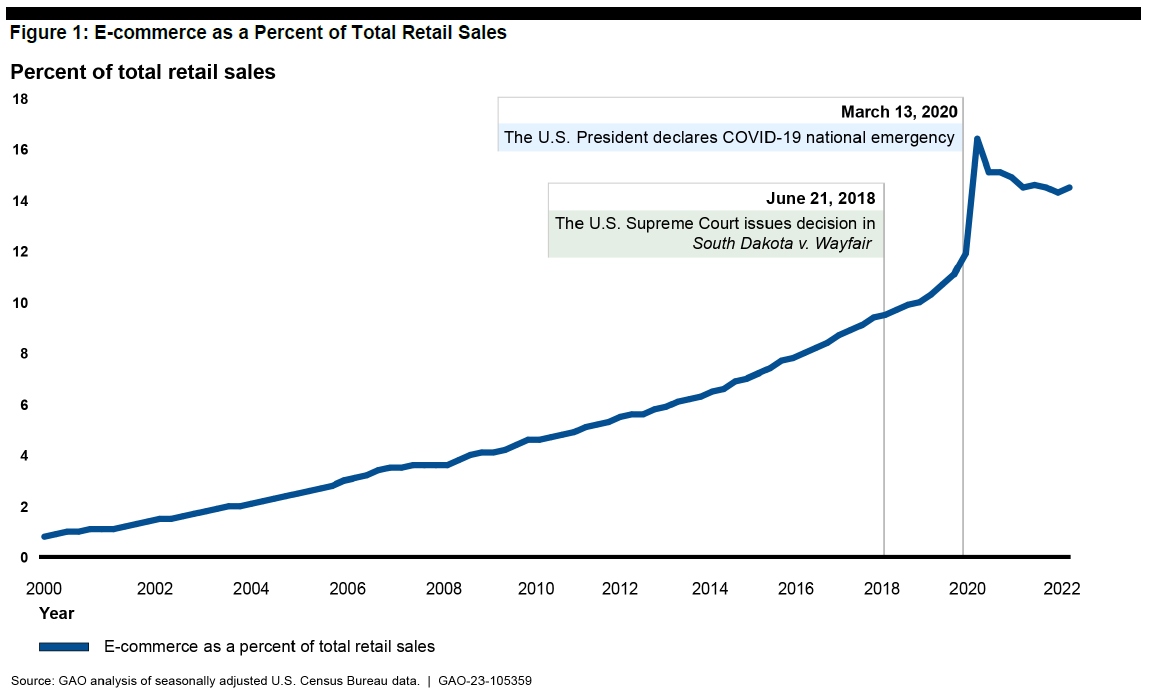

When I was first looking at issues of state-level sales taxes, many years ago, the issue was when buyers went outside a jurisdiction with a sales tax: for example, people buying cars in New Hampshire (with no sales tax) to avoid the Massachusetts sales tax. But the online economy has brought a much bigger version of this problem. If a business has no physical presence in a state, but sells online to people in that state, does it owe state sales tax? In the case of South Dakota vs. Wayfair (2018), the US Supreme Court held that states could apply their sales tax to out-of-state online sellers.

The decision seems reasonable to me, but it opened a new can of worms. It meant that an online seller now was supposed to comply with different sales tax rules across the United States. The Government Accountability Office (GAO) reviews the issues in “Remote Sales Tax: Federal Legislation Could Resolve Some Uncertainties and Improve Overall System”.

The GAO report notes that online sales have been a rising share of retail sales overall.

The challenge for sellers, faced with the Supreme Court decision, is how to comply with the tax rules of states. It’s worth remembering that most online sellers are not Amazon–which is sometimes called a “market facilitator. According to GAO, most businesses with remote online sales are pretty small: 85% have fewer than 10 employees and 74% have fewer than five employees.

Many states have sales taxes, and many additional have local-level sales taxes as well. GAO writes:

Of the 45 states with a statewide sales tax, 37 also have local sales taxes. In addition, while Alaska does not have a statewide sales tax, it does have local sales taxes. Local sales tax authority varies widely. In some states, only selected jurisdictions may impose a sales tax, while in others a broad range of jurisdictions—such as counties, municipalities, and various local authorities—may opt, either by ordinance or local referendum, to impose a sales tax. Tax policy specialists have estimated that approximately 30,000 local jurisdictions in the U.S. have the authority to impose sales taxes and that between 10,000 and 12,000 do impose sales taxes. While technically imposed on the purchaser, both state and local sales taxes are usually accompanied by a collection requirement—sellers are required to collect the tax at the time of purchase.

For sellers, knowing the tax rates for the different jurisdictions is just the start. Many states have thresholds to exempt smaller firms from the sales taxes, sometimes defined in terms of number of transactions and sometimes in value of sales. GAO writes:

[A]s of September 2022, 22 states and the District of Columbia had adopted economic nexus threshold values of $100,000 in sales or 200 transactions into the state each year. Three large-population and large-Gross Domestic Product states (California, New York, and Texas) adopted higher monetary thresholds of $500,000. More recently, some states (including Florida, Kansas, and Missouri) adopted monetary thresholds without an accompanying transactional threshold. Other states (including Iowa and Maine) eliminated previously-established transactional thresholds in favor of monetary-only thresholds. Some states also raised or lowered their previously-established monetary thresholds, including Tennessee, which moved from $500,000 to $100,000.

The timing of these thresholds is calculated in various ways: for example, sometimes the previous calendar year, sometimes the previous 12 months from the current date, sometimes the previous four quarters. In addition, some states exempt certain items from the sales tax. If an out-of-state firm exceeds the thresholds, it typically needs to register with the tax authorities of each relevant state.

Imagine a firm located in a state that doesn’t have a sales tax: now, it needs to be set up to deal with 45 different state sales taxes.

There are a number of uncertainties here. For example, is a firm making out-of-state sales subject to being audited separately by every state where it has customers? The Supreme Court decision focused on state sales tax, but can states also collect local sales taxes? As GAO notes, some states have a substantial number of taxing authorities:

According to our review of state documentation and other third-party legal analysis, Alabama has more than 300 local tax authorities, Alaska has more than 100, Colorado has 70, and Louisiana has 64. Each of these states has a centralized system to streamline registration and filing for remote businesses.

This fragmentation of sales tax rules across states and localities just can’t be the best way to collect sales tax on online purchases. The GAO estimates that states are currently collecting about $30 billion a year on sales tax from out-of-state online sellers, so these tax liabilities are not going away. But if one believes, as I do, that online sales are a boon to consumers (greater choice, often lower prices, reduced time in transit), then it makes sense to think about a simpler system.

Broadly speaking, there are two options here. One is to establish a set of state-level guidelines for describing their remote sales taxes–rates, thresholds, exemptions, everything. This would at least make it easier for the sellers. The more sweeping choice would be to have an interstate collaborative mechanism: if states want to collect from online sellers in other states, they would register with the interstate organization. In taking this step, the state would submit a comprehensive form that covered all aspects of its sales taxes. Private companies that sell accounting and tax software would be able to access this combined data. The idea is that an online seller would have one place to turn for all the needed information, and complying with the information available from that centralized site would fulfill its legal obligations as a taxpayer.

The task of coordinating such a collaborative mechanism isn’t a simple one. The federal government has limited power to tell the states what to do in this area. However, the question of setting up this kind of mechanism isn’t an especially partisan question: every state can retain its own tax rules. Thus, it’s really a test of the ability of state-level governments to solve a nuts-and-bolts practical problem.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest