Comments

- No comments found

One of the strange aspects of the collapse of Silicon Valley Bank back in March was the realization that many banks hold deposits much larger than $250,000.

Thus, the depositors are not covered by federal deposit insurance and are ready to participate in a bank run if the bank looks shaky.

An obvious question arises: For these large depositors–often businesses using the bank account to receive payments for sales and to make payments to workers and suppliers–why not spread out their bank accounts over several or many banks, so that each account would be covered by deposit insurance? In the modern financial sector, is this really so hard to do?

Dylan Ryfe and Alessio Saretto of the Dallas Federal Reserve provide an explainer on how this process was already going on before the downfall of Silicon Valley Bank in “Reciprocal deposit networks provide means to exceed FDIC’s $250,000 account cap” (Federal Reserve Bank of Dallas, November 28, 2023).

The authors point out that there are about $16 billion US bank accounts covered by deposit insurance. About 99% of those accounts are below the $250,000 limit. But the other 1% of accounts hold $7 billion–about 43% of the total. They write:

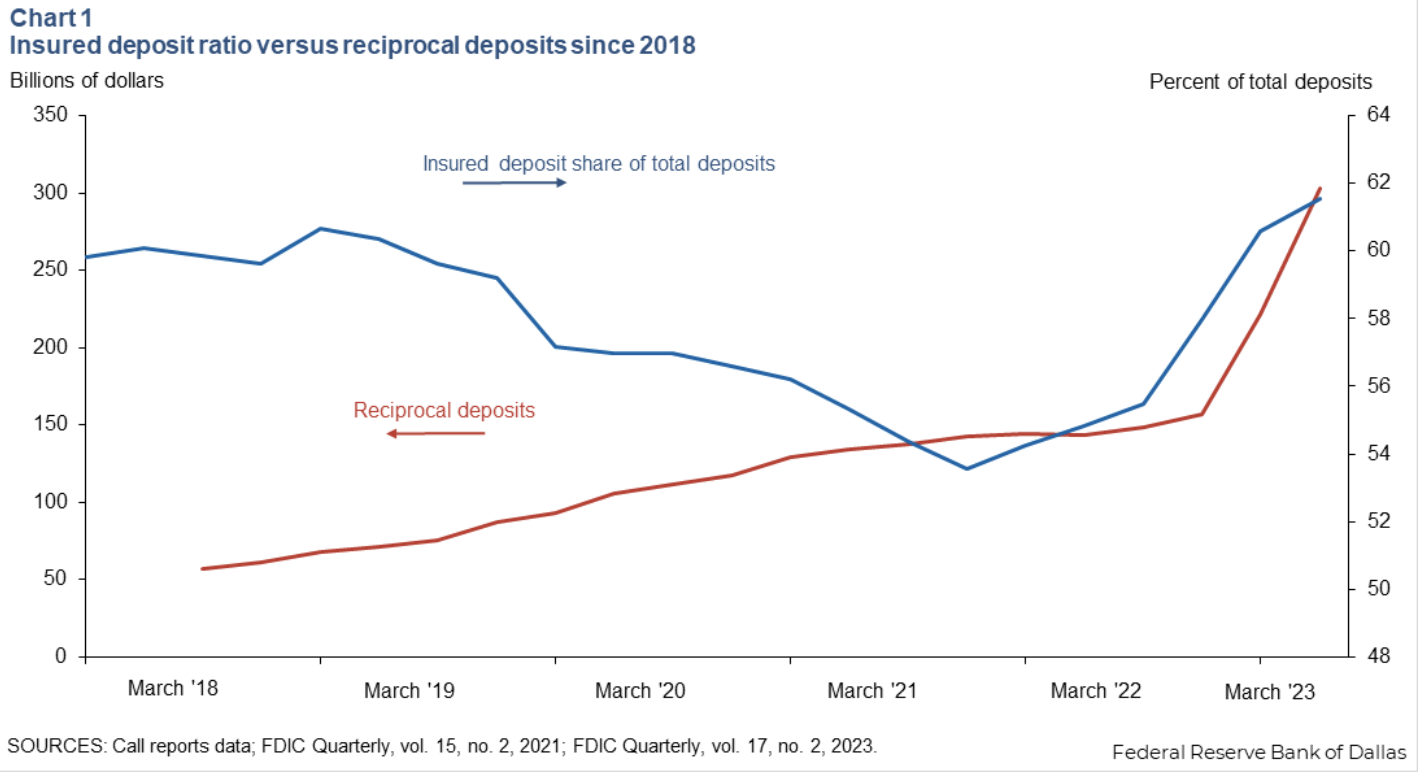

Reciprocal deposit networks have aided this recent growth of insured deposits. These networks, which have been around since the early 2000s, essentially offer a matching service that allows banks to interchange deposits in order to increase exposure to FDIC insurance. Reciprocal deposits rose to more than $300 billion in the second quarter 2023, up from almost $157 billion at the end of 2022.

The idea is that big depositors in one bank can go through networks like IntraFi or R&T Deposit Solutions and “swap” with big depositors at another bank–thus spreading out bigger deposits over many banks so they can be covered by deposit insurance.

One of the main beneficiaries of reciprocal deposit networks seems to be medium-sized banks. Such banks might have trouble attracting big corporations as customers, if the big corporations reason (perhaps unfairly) that a medium-sized bank is a less secure place for deposits. But if the medium-sized bank uses reciprocal deposits to provide a federal insurance guarantee for all deposits, then the big corporation doesn’t have to worry about the solvency of the bank. Apparently, one after-effect of the Silicon Valley Bank failure was a movement of big deposits away from medium-sized banks, and then the banks responding with an expanded use of reciprocal deposits (as reflected in the figure above).

How do bank regulators look at a situation where banks are participating in reciprocal accounts? Up to a certain amount, they don’t worry about it much: that is, “up to the lesser of $5 billion or 20 percent of liabilities for low-risk, well-capitalized banks.” To put it another way, $5 billion would allow for 20,000 swaps of $250,000. Above those levels, regulators would start taking a closer look at the risks involved.

But there are big-picture issues here as well. One of the dynamics of current banking regulation is that the 99% of accounts holding deposits below $250,000 don’t need to worry about whether their bank is safe, because they can rely on deposit insurance. However, the 1% with larger deposits should be worrying, at least a little! Together with federal regulators, outside investors, and financial press, those big depositors are part of the network that gathers information and provides feedback about bank safety. As Ryfe and Sarreto put it:

More deposit insurance can alleviate safety concerns and instill faith and security in the banking system, increase depositor welfare and incentivize small-versus large bank competition. However, it also raises concerns that banks, due to this increased perceived security, might engage in more aggressive profit-seeking activities …

Of course, none of this explains why the supposedly super-sharp venture capitalists, who had put their funds into the companies that held large deposits at Silicon Valley Bank, were not already requiring the use of reciprocal deposit arrangements before March 2023. A blind spot that big makes one worry about the existence of other blind spots.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest