Comments

- No comments found

One year ago in March 2023, Silicon Valley Bank melted down, quickly followed by similar meltdowns at Signature Bank and First Republic Bank.

Measured by the nominal size of bank assets, these were three of the biggest four US bank failures in history. (The failure of Washington Mutual Bank in 2008 remains the largest.) Was this just a one-off, or a problem that has already been fixed? Or do the underlying causes continue to linger?

Tobias Adrian, Nassira Abbas, Silvia L. Ramirez, and Gonzalo Fernandez Dionis take on these issues in “The US Banking Sector since the March 2023 Turmoil: Navigating the Aftermath (IMF Global Financial Stability Notes, March 2024).

I’ve discussed different angles on failure of Silicon Valley Bank a few times on this blog already: for example, see “An Autopsy of Silicon Valley Bank from the Federal Reserve” , “Was Bailing out the Silicon Valley Bank Depositors the Right Decision?”, “Why are the Recent US Bank Runs So Much Faster?”, and “Spreading Accounts Across Banks for the Deposit Insurance” (November 29, 2023). For an all-in-one-place overview with some additional time for reflection, I recommend Andrew Metrick’s essay, “The Failure of Silicon Valley Bank and the Panic of 2023” in the Winter 2024 issue of Journal of Economic Perspectives (38:1, 133-52).

(Full disclosure: I’ve been Managing Editor of the Journal of Economic Perspectives since 1986, so the articles therein are necessarily of interest to me. However, the articles are also all freely available to all compliments of the American Economic Association, from the most recent to the first issue of the journal.)

In some ways, the banks that failed had problems that were not widely shared. Bank deposits in the US are insured up to $250,000 by the Federal Deposit Insurance Corporation. Thus, no one with deposits smaller than that amount has reason for concern about whether their bank might fail. However, companies might at times hold more in their bank accounts, and companies at the Silicon Valley Bank, in particular, were holding a lot of money that they had received from venture capitalists. Indeed, a whopping 94% of the deposits at Silicon Valley Bank were above the $250,000 limit, and thus uninsured. This is not the situation for most banks.

However, some problems of Silicon Valley Bank were more widespread across the banking sector. In particular, if you are holding a financial asset that pays a fixed rate of interest, like most US Treasury bonds, and interest rates rise, then the value of that lower-interest-rate bond will decline. Many banks hold US Treasury bonds, although Silicon Valley Bank holds more than most.

As the IMF authors note,

In March after the failure of SVB [Silicon Valley Bank] and SBNY [Signature Bank], depositors and investors became concerned, first about liquidity and then about the financial soundness of banks matching a certain profile with various attributes including: (1) sizable deposit outflows; (2) high concentrations of uninsured deposits; (3) reliance on borrowing and higher use of liquidity facilities, (4) substantial unrealized losses; and (5) high exposure to CRE [commercial real estate. Although, the high level of uninsured deposits and sizable deposit outflows were unique characteristics of the failed institutions (SVB, SBNY, and FRB [First Republic Bank]), our analysis identifies a group of small and regional banks that have sizable uninsured deposits to total deposits, sizable unrealized losses, high concentration to CRE, and increased reliance on borrowings after the March 2023 stress.

The issue of commercial real estate wasn’t a problem for Silicon Valley Bank. But many regional banks have made substantial loans for those who are building commercial real estate. With the shift to a work-from-home economy, the value of commercial real estate has dropped and the risk of these loans has increased. The authors note:

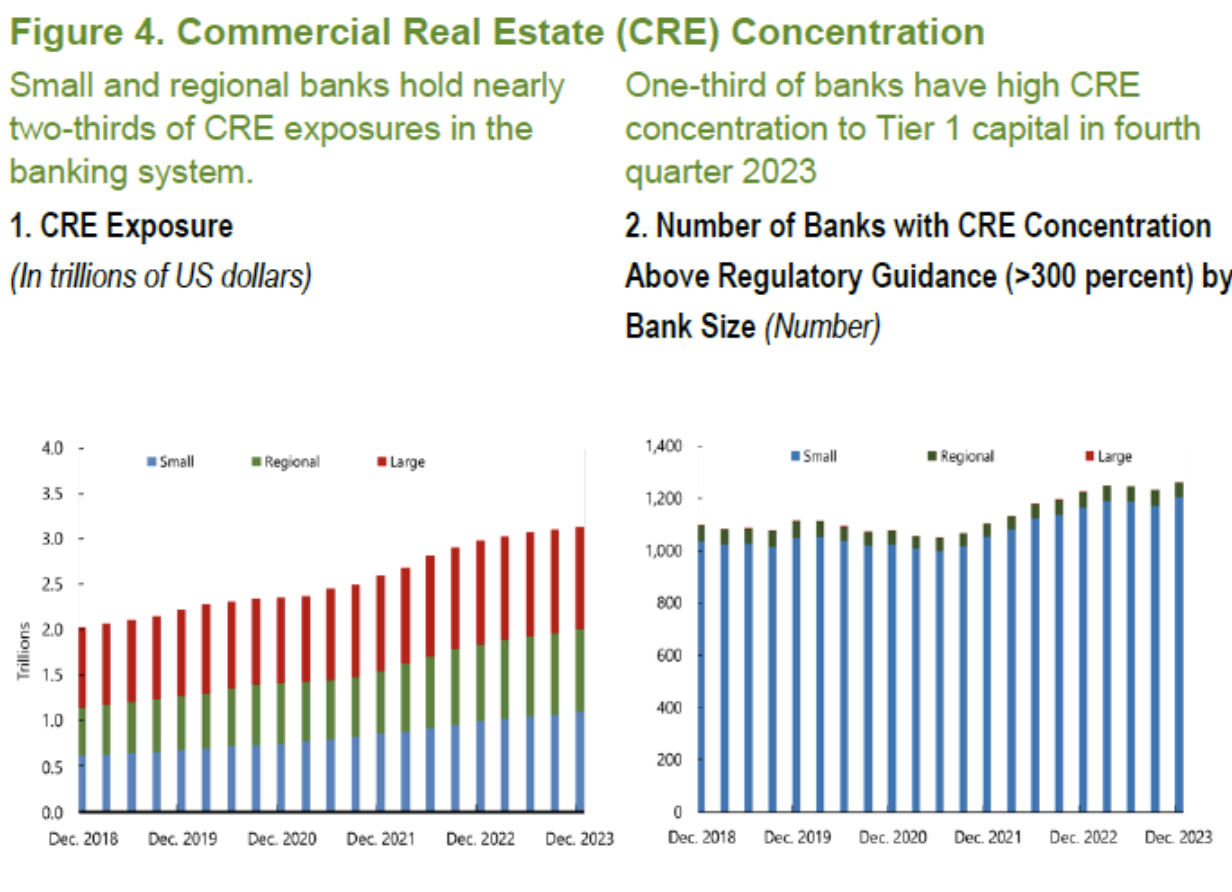

Beyond the unrealized losses due to higher interest, the credit risk carried by some institutions, particular their exposure to CRE [commercial real estate], is at the center stage of investors’ fears today. Small and regional banks are substantially exposed with about two thirds of the $3 trillion in CRE exposures in the US banking system (Figure 4, panel 1). In January 2024, shifts in market expectations regarding the timing and pace of interest rate cuts in the United States, coupled with substantial losses announced by a large bank heavily exposed to CRE, prompted a 10 percent decline in the regional bank’s stock index.

The high concentration of CRE exposures represents a serious risk to small and large banks amid economic uncertainty and higher interest rates, potentially declining property values, and asset quality deterioration. … One-third of US banks, mostly small and regional banks, held exposures to CRE exceeding 300 percent of their capital plus the allowance for credit losses, representing 16 percent of total banking system assets (Figure 4, panel 2).

The IMF authors are not doom-saying here. They refer to this issue as a “weak tail” of banks, by which they mean that it takes the confluence of all five factors they mention to cause a bank failure. But reading between the lines, I wouldn’t be surprised to see the bank regulator forcing mergers on some of the small and regional banks in the “weak tail,” and trying to do so before a bank’s financial situation becomes dire.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest