Comments

- No comments found

The crypto industry is obsessed with figuring out if digital assets are actually backed by anything, but they should be careful what they wish for, they might actually find out.

Inthe wake of FTX’s spectacular collapse, amidst a hailstorm of fraud and mismanagement allegations, focus was naturally switched to the world’s largest surviving cryptocurrency exchange that was still standing— Binance.com.

Over the course of several days, a whopping US$6.4 billion worth of cryptocurrencies and stablecoins were withdrawn from Binance.com, more or less seamlessly, save for hiccups with respect to the stablecoin USDC, but otherwise, with little issue.

Binance.com’s ability to satisfy any withdrawals out of its exchange helped to assuage concerns over its solvency and that depositor assets were fully backed, leading to net inflows to the exchange in recent days.

But are investors and traders asking the right questions?

Since the first Tether (a dollar-denominated stablecoin) was minted, questions have been raised ever since about the true circumstances backing a stablecoin or cryptocurrency.

For an industry founded on the decentralized ethos of Bitcoin, that obsession with backing has always been somewhat peculiar — if the value of a cryptocurrency is its consensus mechanism (a shared agreement that the token is of value), then why this fixation with whether or not a token is backed?

The main issue of course is that consensus isn’t a static construct and it manifests itself through the price mechanism.

Price equilibrium is a reflection of consensus, albeit an imperfect one, and as any trader will attest, a fleeting circumstance.

As such, stablecoins such as Tether, were born of that desire to achieve some form of equilibrium within the cryptocurrency markets, a brief respite in a vast ocean of volatility, and with it, the desire to make sure that equilibrium was more actual than perceived.

As evidenced by the experience with FTX, cryptocurrency traders have long run the gauntlet of centralized exchanges, judging them more on marketing and the personalities who led them, instead of demanding full audits and greater transparency.

The absence of a global regulatory framework to govern cryptocurrency exchanges hasn’t helped transparency or investor protection either, with the world’s biggest exchanges regularly plying the unsavory trade of regulatory arbitrage with impunity.

And that brings us to Binance.com, an exchange which in the aftermath of the FTX collapse could possibly have come out to set industry best practices, but instead has raised more questions than were even asked.

It would be naïve to associate centralized cryptocurrency exchanges with a strong desire to be regulated.

Outside of perhaps the listed U.S. cryptocurrency exchange Coinbase and its competitor Gemini, the world’s biggest exchanges have often chosen to domicile themselves in jurisdictions with “light touch” regulation, to manage their affairs away from the prying eyes of perhaps more zealous regulators in global financial centers.

But the long arm of the law reaches out to even the most far flung locales, which is why both FTX and Binance.com had localized, sanitized versions in major jurisdictions, which have long been suspected of serving as red herrings to throw regulators off the scent of what was really going on behind the scenes.

As recently as October 2022, Reuters uncovered proof that Binance.com incorporated its U.S. entity to serve as a decoy for regulators to chew at, a strategy that the cryptocurrency exchange is believed to have long employed to always stay one step ahead of regulators.

And while entities such as Binance.US and Binance France remain highly visible, few even know where the exchange that matters — Binance.com is actually domiciled (most likely the Cayman Islands).

Binance.com is privately held, and so it is under no obligation to disclose even the most basic financial information, not its revenue, profit, cash reserves, or balance sheet.

While Binance.com, just like FTX, issues its own token, BNB, it doesn’t reveal what role BNB plays on its balance sheet.

Binance.com also lends customers money against their cryptocurrencies, allowing them to take ludicrous amounts of leverage (up to 125 times) and trade on margin, but without revealing how big those bets are, how exposed the exchange is to that risk nor its ability to finance withdrawals.

Because Binance.com hasn’t had to raise outside funding since 2018, it also hasn’t had to share financial information by way of pitch decks to venture capitalists either.

As black boxes go, Binance.com’s appears to be hermetically sealed and attempts to at least have some semblance of external validation are meeting stiff resistance.

In recent days, accounting firm Mazars indicated that they would be temporarily halting work for cryptocurrency clients globally, including for Binance.com, which was a client.

Having the accountant quit on Binance.com just as investigators from the U.S. Department of Justice are circling is not a good look, and the timing could not be more inconvenient.

Yet even if Mazars hadn’t quit on Binance.com, it’s less clear what the value that work (if any) was.

Mazars had been tasked with examining just the Bitcoin holdings of Binance.com as they existed at the end of one day in November and in a December 7 report, the accounting firm reported that just Binance.com’s Bitcoin holdings alone exceeded its customer Bitcoin liabilities.

Although Binance.com claimed the report to be an audit, Mazars clarified that it was an “agreed-upon procedures engagement” and was “not an assurance engagement.”

But audits in and of themselves are not silver bullets.

Even when auditors have been called in to inspect the books in other cases, that hasn’t stopped grifters from grifting.

Take Arif Naqvi’s Dubai-based private equity firm The Abraaj Group for instance, which collapsed under an avalanche of fraud and misuse of funds and which had one of its funds audited by “Big Four” accounting firm KPMG.

At the time, Naqvi moved money around various funds under control of The Abraaj Group so that when auditors at KPMG inspected the bank accounts of the fund in question, it appeared that the monies were present, only to be spirited away the very next day.

Such is the limitation of asset “snapshots” which do little other than to quell any momentary queasiness as to the solvency or integrity of a firm’s balance sheets.

Short of a full scale audit of Binance.com, few outside of Changpeng Zhao or CZ as he is better known, and several other members of his inner circle, are likely to have a holistic view of what is under the hood of a cryptocurrency exchange that is said to do trillions in trading volume annually.

It also doesn’t help that recently Mazars took down the webpage containing its report on Binance.com’s Bitcoin reserves “due to concerns regarding the way these reports are understood by the public.”

But whether Binance.com has all of the reserves it says it has, isn’t necessarily the biggest issue for investors, but what the quality of those reserves actually is.

And that analysis requires investigation of a little-known stablecoin — TUSD.

If you’ve never heard of TrueUSD or TUSD, that’s probably because you’ve not needed it.

Created in 2018, TUSD is a dollar-backed stablecoin issued by TrustToken, but with an interesting feature — the name on the bank account that TUSD could be redeemed to would also need to be the same name held with your TrustToken account.

And for convenience, the good people at TrustToken made sure that the Ethereum wallet addresses used at TrustToken were extremely simple to recall with plenty of 0s.

But which were the banks that were allowing the receipt of TUSD proceeds into their accounts?

Because most banks would close bank accounts linked to large cryptocurrency transactions, it was only a select clutch of banks that were willing to process TUSD redemptions.

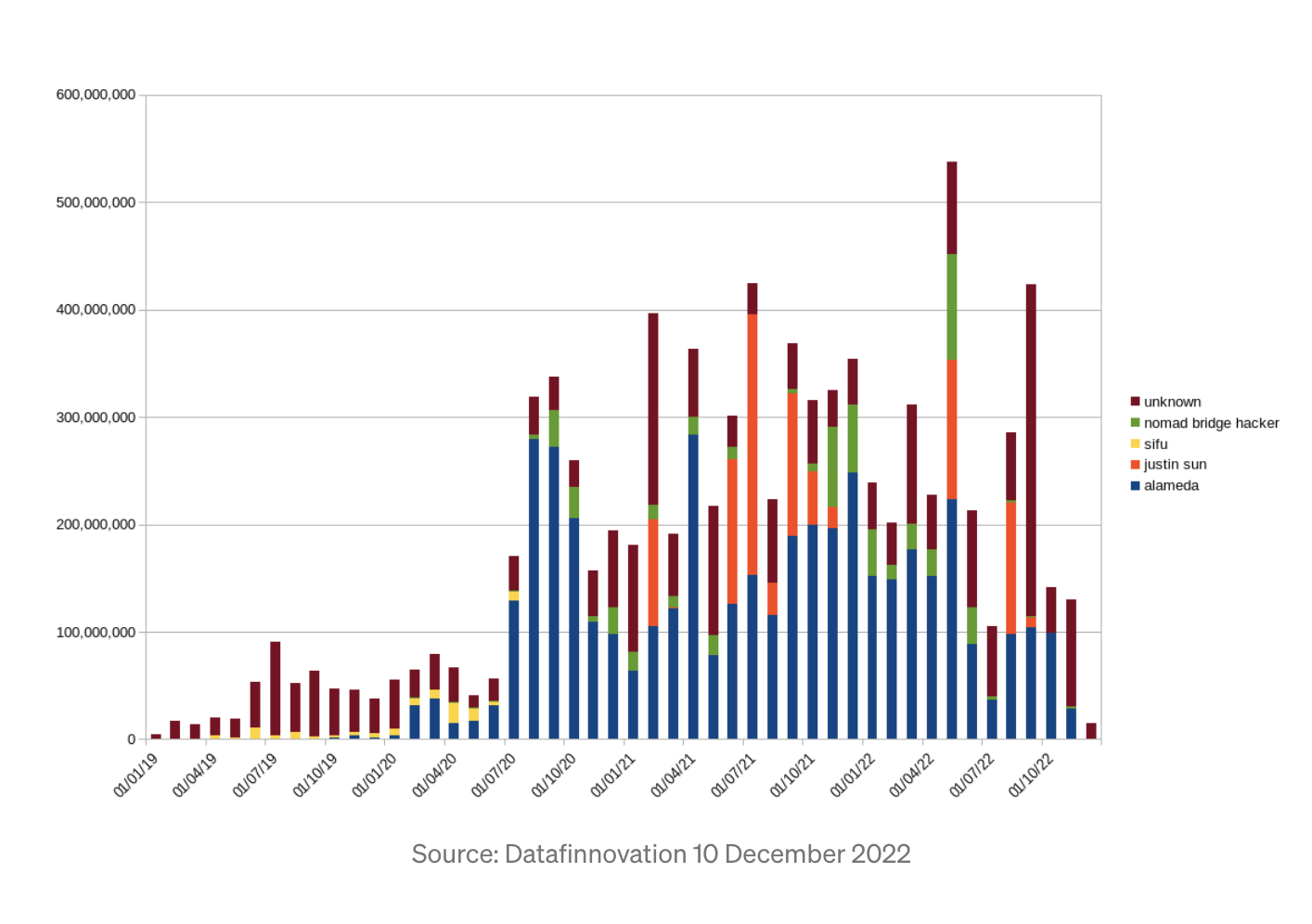

And who redeemed that TUSD will raise no shortage of eyebrows as revealed by the excellent research from DataFinnovation.

Over 70% of all TUSD redemptions were conducted by just 4 parties, with Alameda Research making the bulk of those redemptions at US$4.4 billion.

In the early days, Genesis Block, a Hong Kong-based company, facilitated millions and possibly billions of dollars worth of cash-for-crypto transactions, with lines running around the corner and the store closing on occasion having run out of coins to sell.

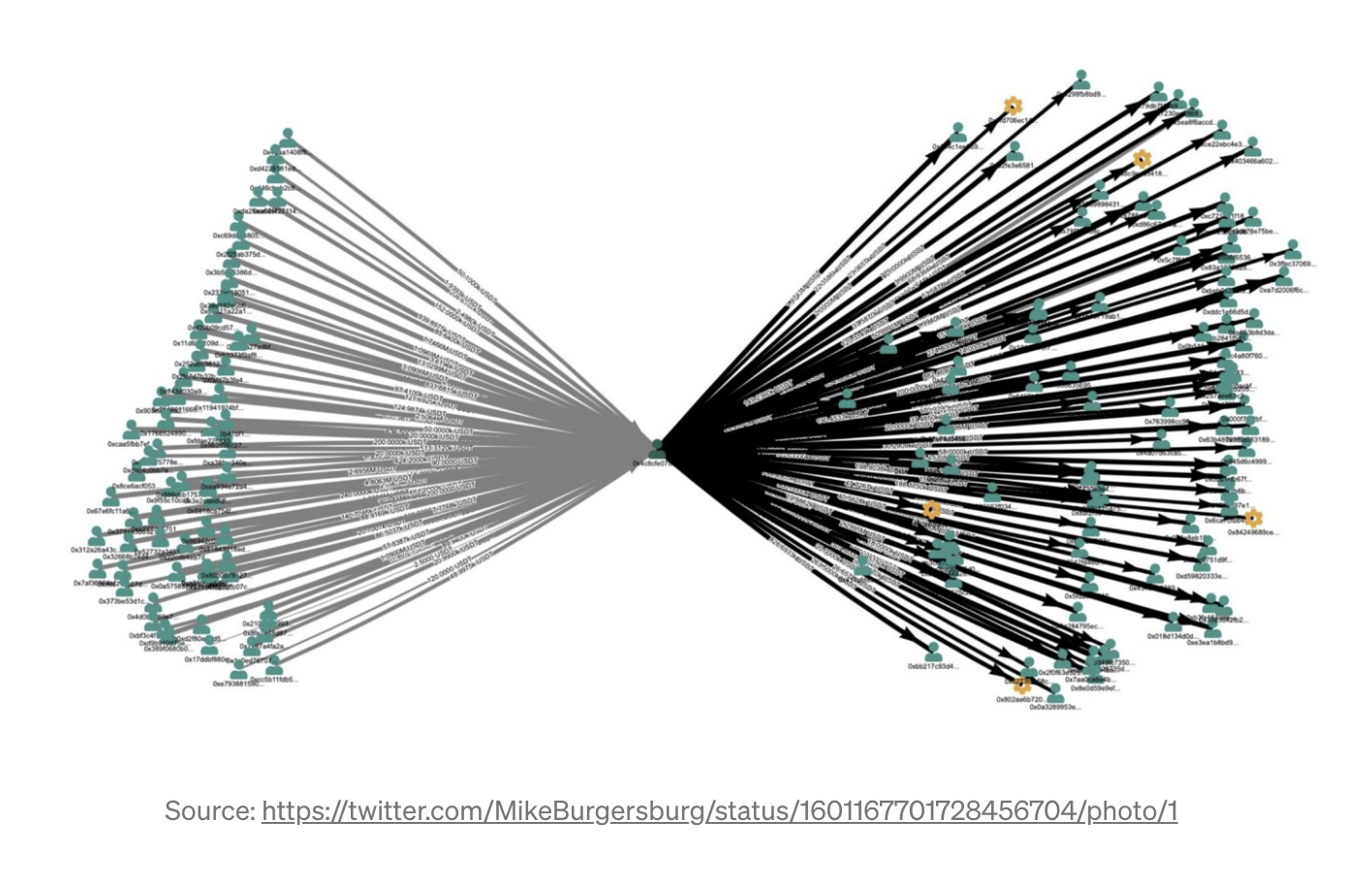

Independent research by Mike Burgersburg suggests that Genesis Block was essentially a front for Alameda Research, with the “hedge fund” then funneling transfers to its wallets out to a whole range of targets — not how a hedge fund wallet would typically be expected to behave.

Further research by DataFinnovation also revealed that the TUSD minted on Binance.com was eventually funneled into USDT and redeemed via FTX into USD.

Which is where the connection between Binance, FTX, Alameda Research and Genesis Block converges — the group appeared to be actively involved in these transactions and sharing the same bank accounts to boot (recall that the redemption address ownership for TUSD had to match the bank account ownership).

Given that TUSD appears to have no real use case outside of these transfers from cash to cryptocurrencies for getting dollars back into the banking system, not much imagination is needed to figure out the “true” purpose of these transactions (pun intended).

But where that TUSD ends up is perhaps even more interesting — through a clutch of banks that were willing to off ramp TUSD transactions.

The availability of these banking relationships allowed FTX and Binance.com to facilitate transfers from cash-to-crypto and back into the banking system, a strategy that worked well for the two exchanges.

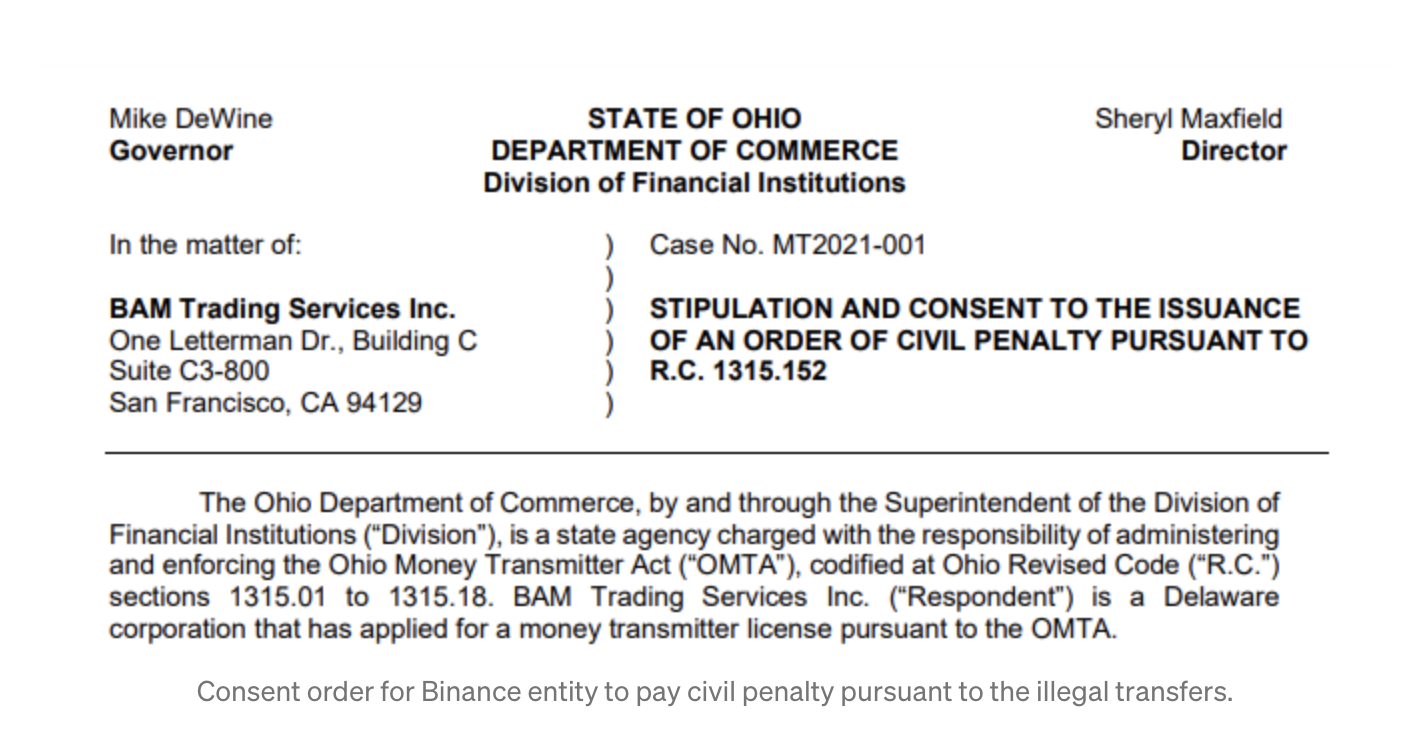

Unlike FTX though, Binance.com went about its business quietly, and when its U.S. entity was fined US$241,000 by State of Ohio for US$138 million in illegal transfers, proceeded to apply for a money transmission license the very same day.

By September 28, 2020, Binance.com went ahead to apply for a money transmitter license, with evidence that BAM Trading Services Inc., a Binance.com-held entity, had been engaged in transactions from as early as 2019, with such transactions denominated solely in cryptocurrencies.

The collapse of FTX is only the tip of the iceberg and even though Binance.com may have accelerated the destruction of its rival cryptocurrency exchange through its purported sale of FTT tokens, the investigation of FTX will no doubt uncover just how close the two rivals once were.

And that may be where things become altogether too interesting for Binance.com.

From as early as 2018 and as reported by Reuters, the U.S. Department of Justice had been investigating Binance.com for evading and contravening U.S. anti-money laundering laws and sanctions.

It was uncovered earlier in 2022 that Binance.com laundered as much as US$8 billion for Iranian firms, in contravention of sanctions.

A history of interesting transfers between Binance.com’s U.S. entities and links to TUSD as well as the cash-for-crypto transactions involving Genesis Block uncovered from the implosion of FTX is now inviting even more attention on Binance.com, which it would clearly rather avoid.

Ostensibly FTX and Binance.com may have been bitter rivals, but recall that at one time, the latter had invested a whopping US$2.1 billion in the former, cementing just how close the two entities once were.

The two “rival” exchanges even shared bank accounts for off-ramping TUSD where convenient.

And while U.S. prosecutors may be divided over whether now is the time to commence legal action against Binance.com, the implosion of FTX may provide them with unprecedented access to the records they need to make a case against the Binance.com, given how intertwined the two exchanges were at one point in time.

Unlike FTX, Binance.com has always insisted in utmost secrecy, using communication channels like Telegram with disappearing messages so as not to keep a record of conversations or correspondence, as reported by Reuters.

FTX insiders on the other hand communicated openly and even though they kept poor accounting records and had no risk management, communication records, emails, interviews and a treasure trove of information and documents on transactions, including banking, may help shed some light on involvement with Binance.com.

More significantly, as the wreckage of FTX is sifted through and if evidence is uncovered that Binance.com facilitated money laundering or other forms of financial crimes, the ensuing actions by U.S. authorities may have major implications on deposits remaining with Binance.com, not least of which is the freezing of any dollar-denominated accounts in the U.S. banking system.

Let’s not forget that not so long ago, Washington froze out Russia’s overseas dollar-denominated foreign reserves, in retaliation for the Kremlin’s invasion of Ukraine, even going so far as to target the Russian central bank.

Should Binance.com be found to have committed money laundering or other heinous financial crimes, U.S. authorities are unlikely to flinch when tasked to freeze any dollar-denominated accounts that may be in the exchange’s control.

And therein lies the real question investors and traders continuing to run the gauntlet on Binance.com should be asking.

It’s not that Binance.com doesn’t have the dollars, it most likely does.

And it’s not that Binance.com can’t facilitate withdrawals, it most likely can.

But those are the wrong questions.

If Binance.com gets frozen or sanctioned by U.S. authorities, it won’t matter how many dollars or tokens it has backing the exchange, because they may be tainted and therefore, liable to be frozen.

Patrick is an innovative entrepreneur and a lawyer passionate about cryptocurrencies and the business world. He is the CEO of Novum Global Technologies, a cryptocurrency quantitative trading firm. He understands the business concerns of founders and business people helping them to utilise the legal framework to structure their companies to take advantage of emerging technologies such as the blockchain in order to reach greater heights. His passion for travel, marketing and brand building has led him across careers and continents. He read law at the National University of Singapore and graduated with Honors in the Upper Division and joined one of Singapore’s top law firms, Allen & Gledhill where he was called to the Singapore Bar as an Advocate & Solicitor in 2005. He created Purer Skin, a skincare and inner beauty company which melds the traditional wisdom of ancient Asian ingredients such as Bird's Nest with modern technology. In 2010, his partner and himself successfully raised $589,000 from the National Research Foundation of Singapore under the Prime Minister’s Office. He has played a key role in the growth of Purer Skin from 11 retail points in Singapore to over 755 retail points in Singapore and 2 overseas in less than a year. He taught himself graphic design, coding, website design and video editing to create the Purer Skin brand and finished his training at a leading Digital Media Company.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest