Comments

- No comments found

The evolution of banking shows a gradual shift from the analog to the digital, over the past few decades, with computers replacing teller machines and virtual data replacing the money in our wallets.

The e-commerce giant, Amazon, talked about getting into online banking this March. The Wall Street Journal reported of early stage talks between Amazon and leading financial institutions like J P Morgan Chase for launching online checking accounts for its customers. The report, however, clears the fact that though the system will closely resemble that in offline banks, Amazon is not turning itself into a bank. A recently conducted survey revealed that nearly 45% of the population is open to Amazon as their primary baking account. Looking back at Amazon’s venture into banking, we realize that banking, as an institution, has adapted and evolved with the changing times and technologies. The initial moneylender business that lent money, charged interest, run by dapper bank officers, sitting behind counters, processing our checks and approving our withdrawals, has come a long way since its inception. The evolution of banking has been advancing in accordance with the needs of the common man to safeguard his valuables. Moreover, technology has impacted the way we view and work with our money. Coins, paper bills, credit and debit cards, and now cryptocurrency are all proof of how the banking sector absorbed technology while catering to the need for investment, trading, and expenditure. However, while all the basic principles of banking have stayed the same, the methods we apply to carry them out have changed. And this change definitely makes banking more organized, more secure, and far more efficient.

The merchant clan, who offered grain loans to farmers, is said to be the first prototype of banks. The critical development of banks, however, is positioned around the Renaissance era, when financial institutions flourished in Europe. From their initial roots, banks have seen ups and downs in the economy across the world, and they will probably be around till man nurtures his instinct of safekeeping.

William Scott, an American economist, authored a book called, Banking, in 1914, talking about the banking systems that existed then. In the book, he outlines the four primary services that banks work on providing their customers:

In the context of these services, one can safely say that the evolution of banking showed tremendous transformation while shifting centuries. While the 21st century banks revolve more around the digital, the 20th century banks were designed in an analog fashion with minimal involvement of technology.

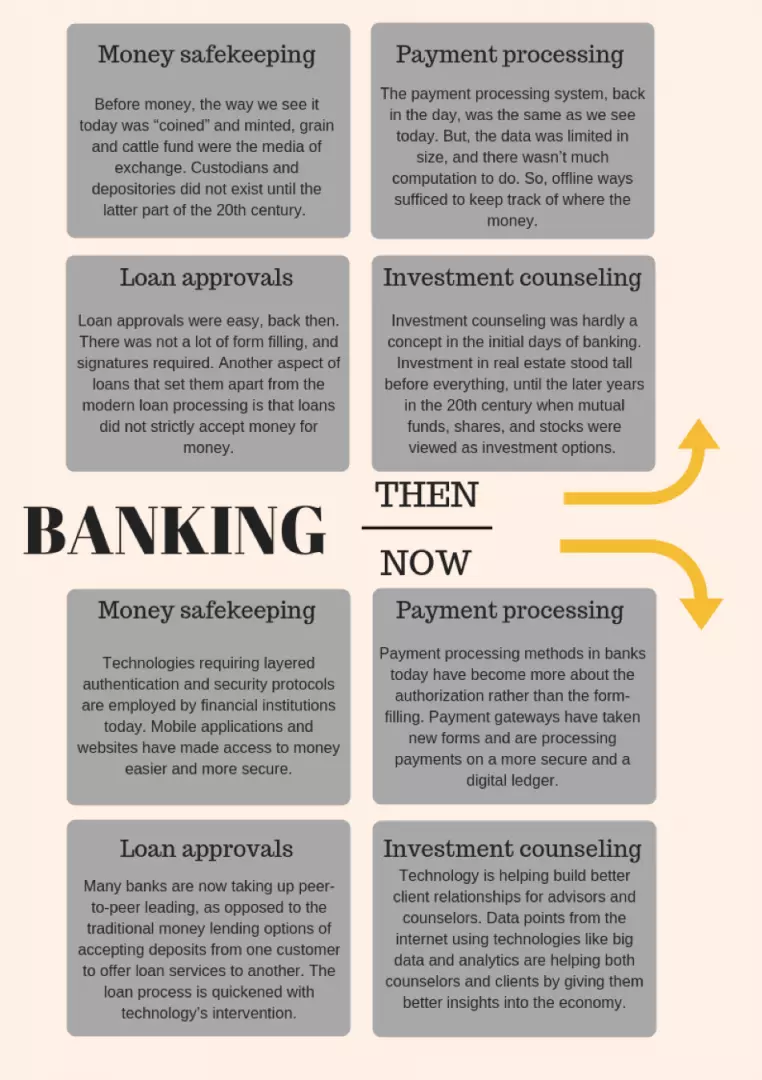

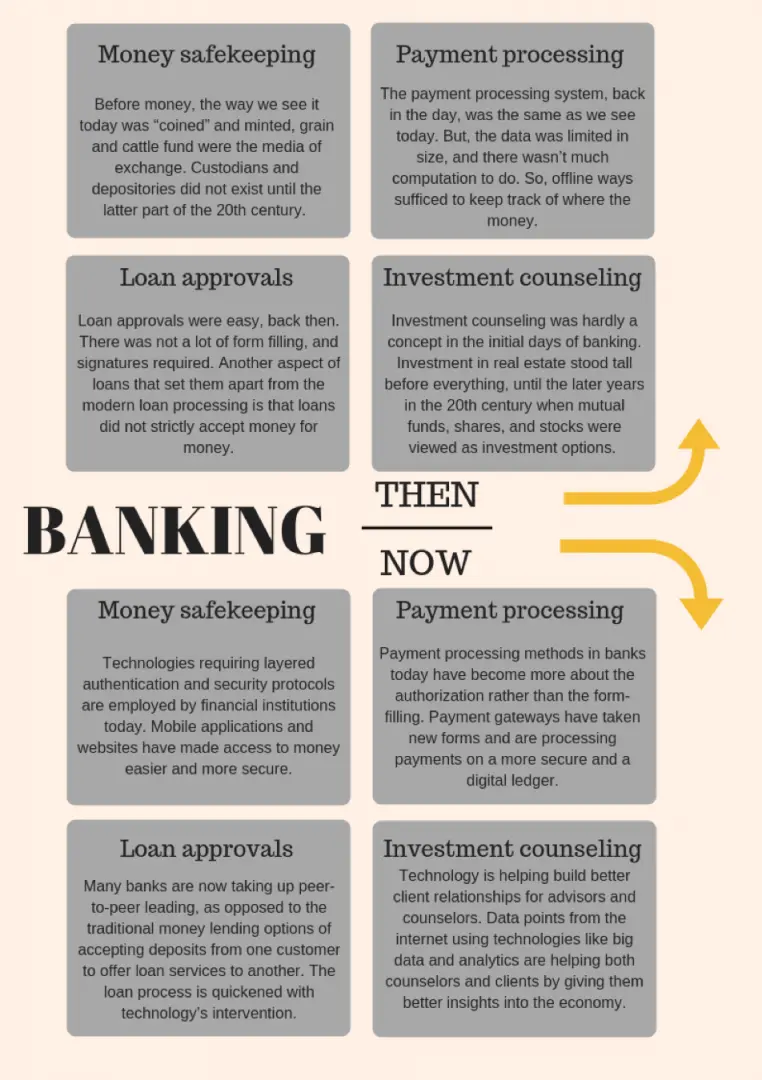

As mentioned earlier, banking in and before the 20th century lied on the analog end of the spectrum. Before money, the way we see it today was “coined” and minted, grain and cattle fund were the media of exchange. Custodians and depositories did not exist until the latter part of the 20th century. The, then bankers, moneylenders, and goldsmith mortgaged kind for cash or anything of value. As printed money started earning popularity, banks and merchant bankers began exchanging money for money with calculated interests.

The payment processing system, back in the day, was the same as we see today. Every money lender would maintain a registry, with the details of each debt the loan borrowers owed him. The data was limited in size, and there wasn’t much computation to do. So, offline ways sufficed to keep track of where the money was going and coming from. Loan approvals were easy back then. There was not a lot of form filling and signatures required. Anyone in dire need of money would simply request the money lords and the request would get approved in return for something valuable as a mortgage. Another aspect of loans that set them apart from the modern loan processing is that loans did not mean repaying only in money.

Investment counseling was hardly a concept in the initial days of banking. Investment in real estate stood tall before everything, until the later years in the 20th century when mutual funds, shares, and stocks were viewed as investment options. Even then, banks did not actively involve themselves in investment counseling or proposed their plans for the same.

Banking, today, is all about the data and the network it possesses. We hardly go to banks for depositing money or encashing checks alone. Our money is saved in a small chip on a card, allowing us to pay for our transactions without actually having to go the bank. Besides, banks and bank records today are highly secure and difficult to tamper with. Here are some key applications of banking in our daily lives:

Banks today are highly competent in safeguarding the money customers keep with them. Financial institutions employ technologies requiring layered authentication and security protocols. Mobile applications and websites have made access to money easier and more secure. A simple withdrawal requires the user passing authentication standards like passwords, security questions, or mobile OTPs to access the account. Every transaction on the account is informed to the account holder via messaging services, email threads, and in-app notifications on personal devices. Facilities like limited login attempts keep brute-force attacks at bay. Some banks like USAA employ fingerprints, face and voice recognition, biometric techniques to detect and prevent fraudulent activities. All these measures ensure that the money in the banks, or so to say, is protected from any form of physical or cyber threats.

One of the pronounced changes of the evolution of banking is the payment processing. Payment processing methods in banks today, have become more about the authorization rather than the form filling. Banking operations are empowered with technology to minimize the paperwork. ATM centers have automated withdrawal operations with no involvement of the teller at all. Some machines also are equipped with systems that can process checks with optical character recognition. The machine understands the characters on the check and reflects the appropriate action on the account. Payment gateways have taken new forms. EMV technology, Mobile Point of Sale machines (mPos), Near Field Communication (contactless) payments, the newest form of fintech, and bitcoins are part and parcel of our lives today. These sophisticated technologies are transforming payments and their processing on a more secure and digital ledger.

Fintech is changing the loan approval model. The evolution of banking has now enabled peer-to-peer lending, as opposed to the traditional money lending option of accepting deposits from one customer to offer loan services to another. The loan process is quickened with technology’s intervention. Earlier banks would take time to approve the loan applications. The ways to verify the applicant’s financial background for the loan were offline. However, Internet today, helps with verification completion within 24 hours. The same fast approval methods are being applied to credit and debit cards too. Banks are also collecting data from various online sites to determine the repayment abilities of the loan borrower. Earlier, word of mouth and written documentation would be enough proof that the loan borrower would repay the loan amount.

Technology is helping build better client relationships for advisors and counselors. A recent study by Cap Gemini, the consulting firm, said that nearly 64% of the people undergoing the survey expected their future investment management to be digital. Data points from the Internet using technologies, like big data and analytics, are helping both counselors and clients understand the trends in the market, thus giving them better insights into the economy. To add to this, the presence of a client’s data on the Internet has given banks more access and power to make the best of the market situation for maximized return on investment.

In conclusion, the evolution of banking has been accelerated by technology. All aspects of banking - communication, data sharing, data processing, and forecasting -have been enhanced by technology. Realizing the potential fintech brings in an organization, the banking sector is creating digital value for themselves and their customers, alike. These new roadmaps are predicted to take not just the banking industry but the entire financial sector to new places in the future, with opportunities equally favorable for its customers and the company.

Naveen is the Founder and CEO of Allerin, a software solutions provider that delivers innovative and agile solutions that enable to automate, inspire and impress. He is a seasoned professional with more than 20 years of experience, with extensive experience in customizing open source products for cost optimizations of large scale IT deployment. He is currently working on Internet of Things solutions with Big Data Analytics. Naveen completed his programming qualifications in various Indian institutes.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest