Comments

- No comments found

Perhaps the key question about the higher level of US inflation is whether it is likely to be transitory, and thus to fade away on its own, or whether it is likely to be permanent unless aggressive policy steps are taken–like additional increases in interest rates by the Federal Reserve.

The case that the current inflation is likely to fade away on its own often argues that inflation has been caused by a confluence of events that probably will not last: people spending money in certain limited sectors of the economy when pandemic restrictions shut down other parts of the economy, supply chain hiccups that occurred partly as a result, and the spike in energy prices. The hope or expectation is that as these factors fade, inflation will fade, too.

The argument that inflation is likely to be permanent is linked to the “Great Resignation” in US labor markets. Firms are trying to hire. Job vacancy rates are sky-high. The result is that upward pressures on wages are likely to keep inflation high, unless or until the Fed unleashes additional interest rate increases that are likely to bring on a recession in the next year or two. Let’s walk through some of the evidence on job vacancies and inflation, and then address the obvious concerns in “blaming” higher wages for causing inflation.

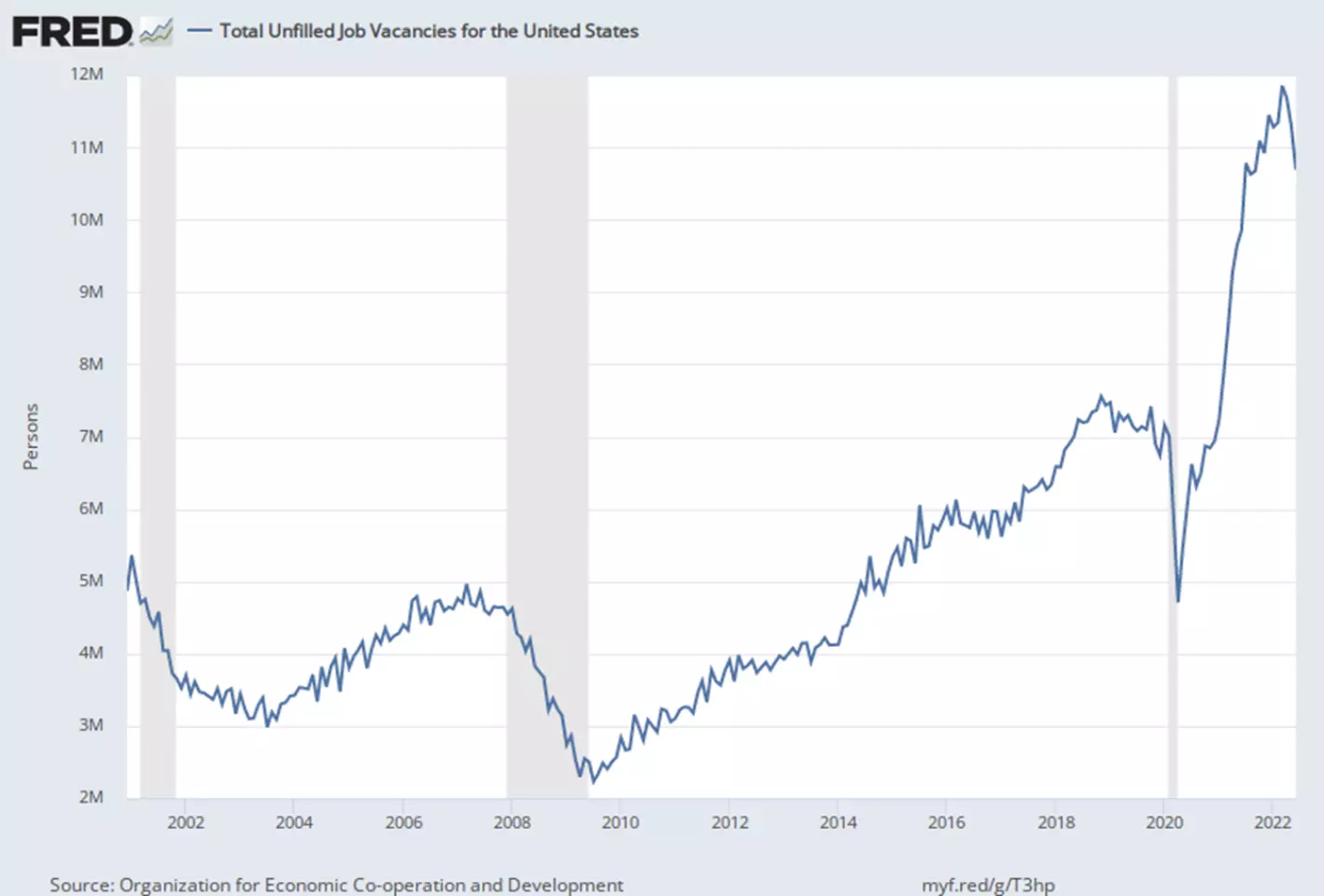

As a starter, here’s the basic numerical count of job vacancies since 2000. Notice that the number was rising even before the pandemic recession in 2020. Indeed, if you squint really hard, you can imagine a more-or-less straight line from the vacancy trends before the pandemic to vacancy numbers that are not too far from current levels.

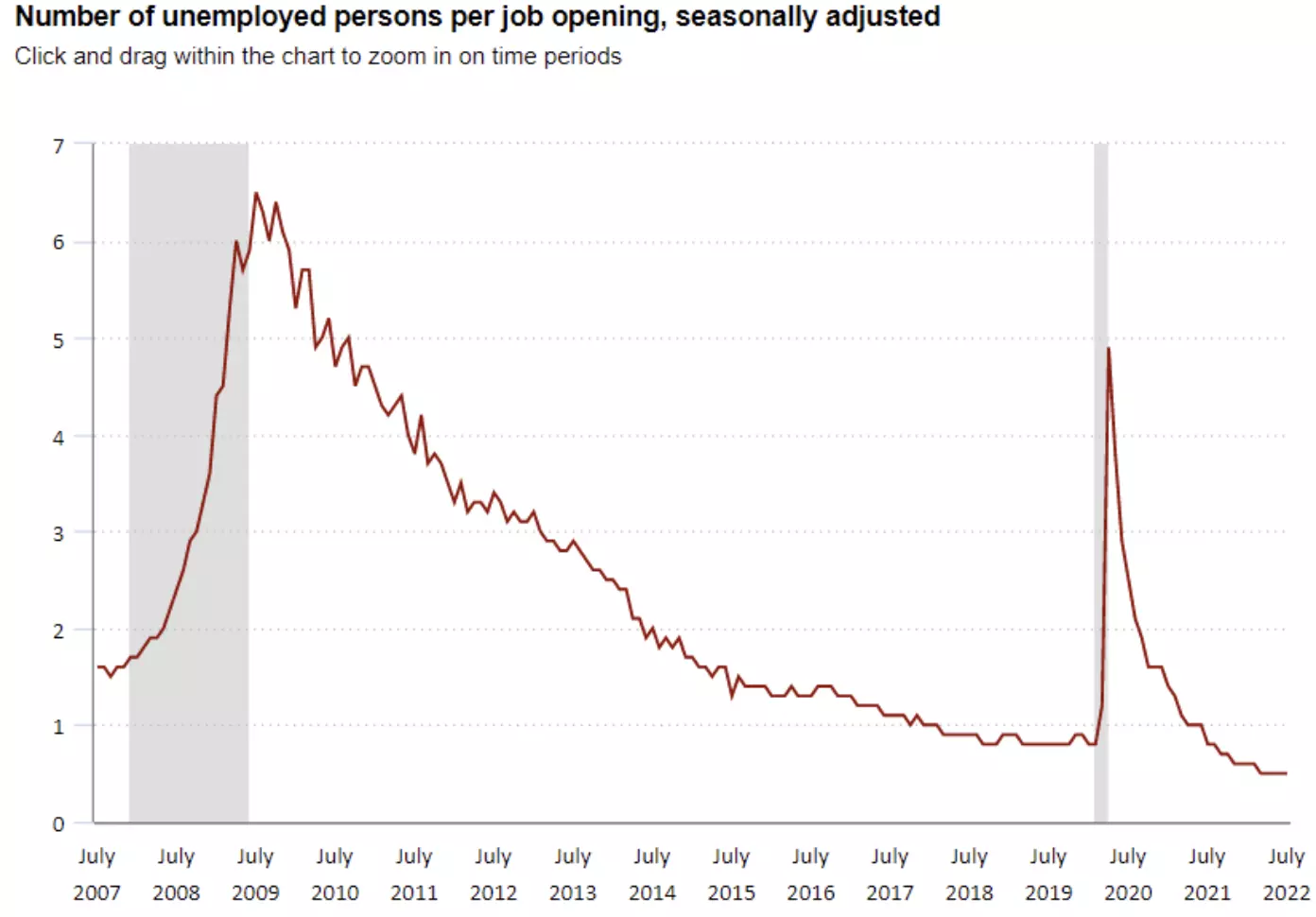

But from the standpoint of inflation, what really matters is job vacancies relative to the number of unemployed people. The concerns over wage inflation arise when there are lots of vacancies and a relatively small number of unemployed people seeking those jobs. Here’s the ratio of unemployed people to job vacancies from the Job Openings and Labor Turnover (JOLTS) survey by the US Bureau of Labor Statistics. Again, notice that this ratio was already trending lower before the pandemic. Also, notice that when this ratio falls below 1, the number of unemployed people is lower than the number of job vacancies.

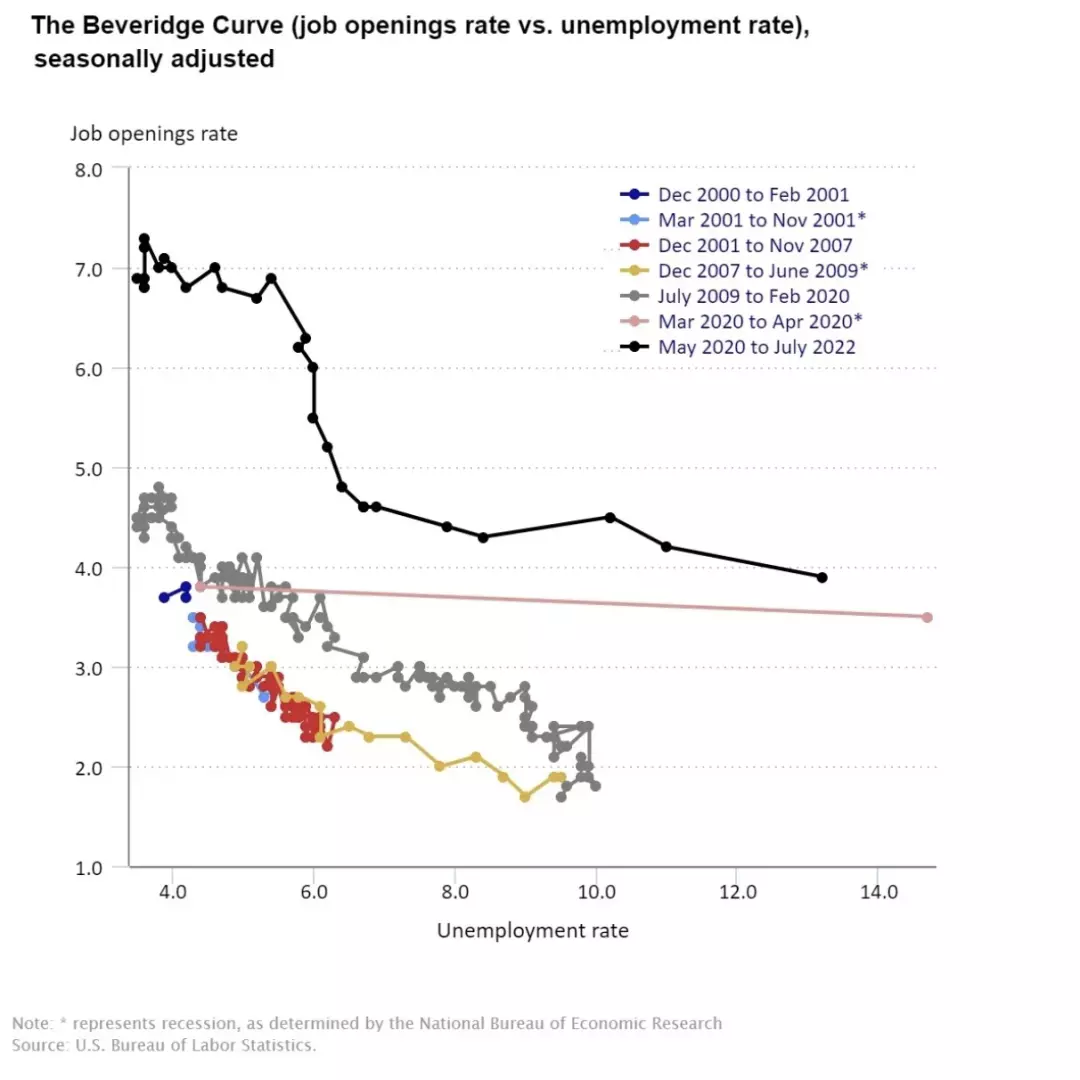

The “Beveridge curve” is another way to look at this data. This curve graphs the unemployment rate on the horizontal axis and the rate of job openings rate on the vertical axis. The usual pattern here is a generally downward-sloping relationship, which is intuitively sensible: that is, times of higher unemployment also tend to be times with lower rates of job openings. Indeed, you can see in the bottom set of colored lines, all jumbled together, the economy in the first decade of the 2000s was basically moving back and forth along a Beveridge curve.

But then the Beveridge curve shifts up during the period from July 2009 to February 2020: that is, for any given level of unemployment rate, the job vacancy rate was higher than before. And since the pandemic, the Beveridge curve has bumped up still higher to the black line: again, for any given level of unemployment rate, the rate of job vacancies is higher than it used to be. To put it another way, employers are seeking to fill more jobs now than they were at previous times when unemployment rates were roughly this low.

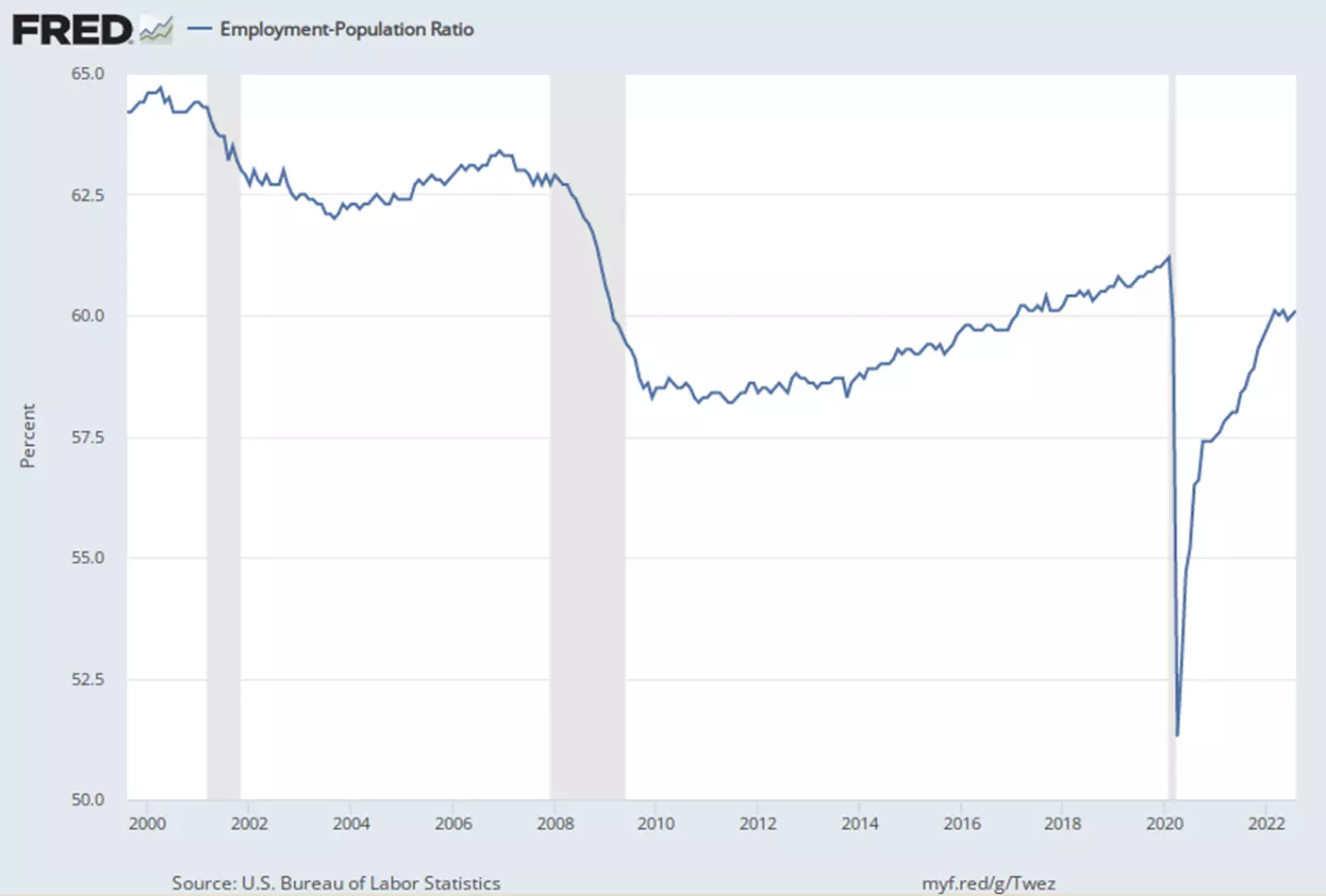

In short, no matter how you look at it, job vacancies are really high right now. I don’t think this phenomenon is yet well-understood. But workers are quitting jobs at high rates, often to take an alternative preferred job, and the employment/population ratio for US adults has not yet returned to pre-pandemic levels.

These job vacancy patterns set the stage for the research paper by Laurence Ball, Daniel Leigh, and Prachi Mishra,” Understanding U.S. Inflation During the COVID Era,” just published as part of the Brookings Papers on Economic Activity (Fall 2022, text as well as video of presentations and comments available). The research paper is full of models and calculations, and will not be especially accessible to the uninitiated. But the basic idea is straightforward.

The authors look at the recent rise in inflation, They find that when one looks at the overall inflation rate, the changes are indeed often due to factors like supply chain issues, energy price spikes, and the like. But if you focus only on “core” inflation, with changes in food and energy prices stripped out, then they find that the ratio of job vacancies to the unemployment rate is the major driving force. In other words, yes, some of the inflation of the last couple of years is temporary, but not all of it. In addition, they find that breaking the back of this underlying core inflation is likely to require additional interest rate increases by the Fed and higher unemployment rate–which sounds to me like the kind of multidimensional economic downturn in product and labor markets that is called a “recession.”

One common response to discussions of how higher wages can drive up inflation is to accuse the teller of the tale of just being opposed to higher wages. This response has a nice “gotcha” zippiness. One can readily imagine a group of sympathetic listeners nodding vigorously and yelling “you tell ’em” and “preach it” and the like. But in an analytical sense, the response is confused. Over time, the only way to have sustainable broad-based higher wages is if they are built on a foundation of sustainable broad-based higher labor productivity. Perhaps the workplace-related innovations unleashed by the pandemic experience will lead to a surge of productivity, but at least so far, that isn’t apparent in the data. Otherwise, higher wages can unleash what used to be called the wage-price spiral: that is, higher wages driving prices up, and higher price levels pushing higher wages. The appropriate social goal is to have higher wages that also have greater buying power, not higher wages that are just perpetually chasing higher price levels.

The Ball, Leigh, and Mishra paper is of course just one set of estimates, albeit from a well-regarded set of economists and published in a high-profile publication outlet. But they are not alone in suggesting that the pattern of very high job vacancies given the level of unemployment may be the key factor driving core inflation higher.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest