Comments

- No comments found

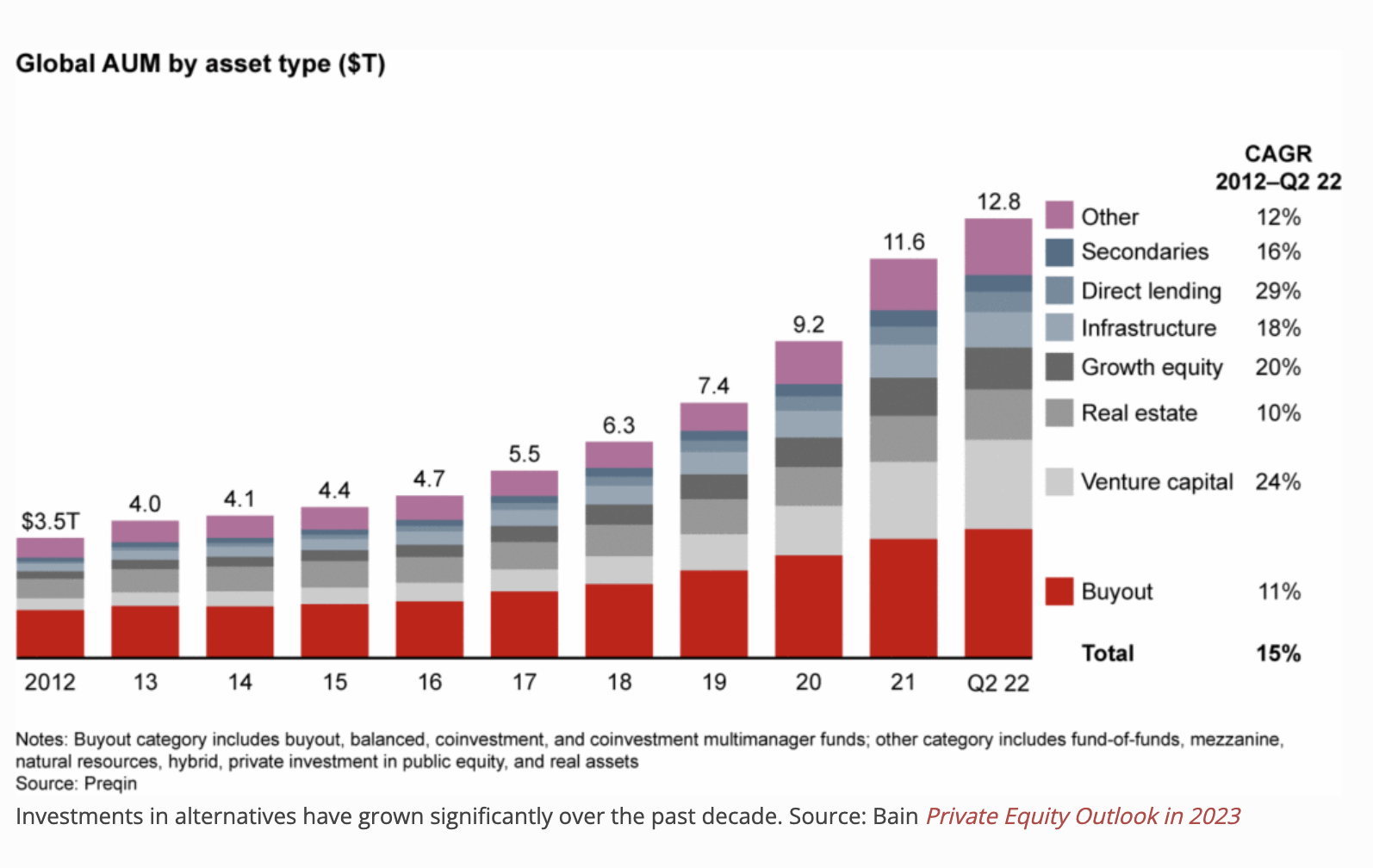

Investments in alternative assets (alternatives) have grown tremendously over the past decade.

Drawn to their professed portfolio benefits, investors have reallocated capital from more traditional assets, like public equities and bonds, into various alternative investments. Some can hardly get enough. Yet, for all the affection, there’s nothing truly alternative about alternatives. They’re simply different flavors of the same investment options.

Investments in alternatives have grown significantly over the past decade. Source: Bain Private Equity Outlook in 2023

To be sure, I take no issue with alternatives. The more investment choices the better, as far as I’m concerned. However, properly understanding one’s risk exposures is vital for investing success. Treating alternatives as separate assets deserving of allocation, in my opinion, only obfuscates them. There’s only credit and equity risk, even in alternatives.

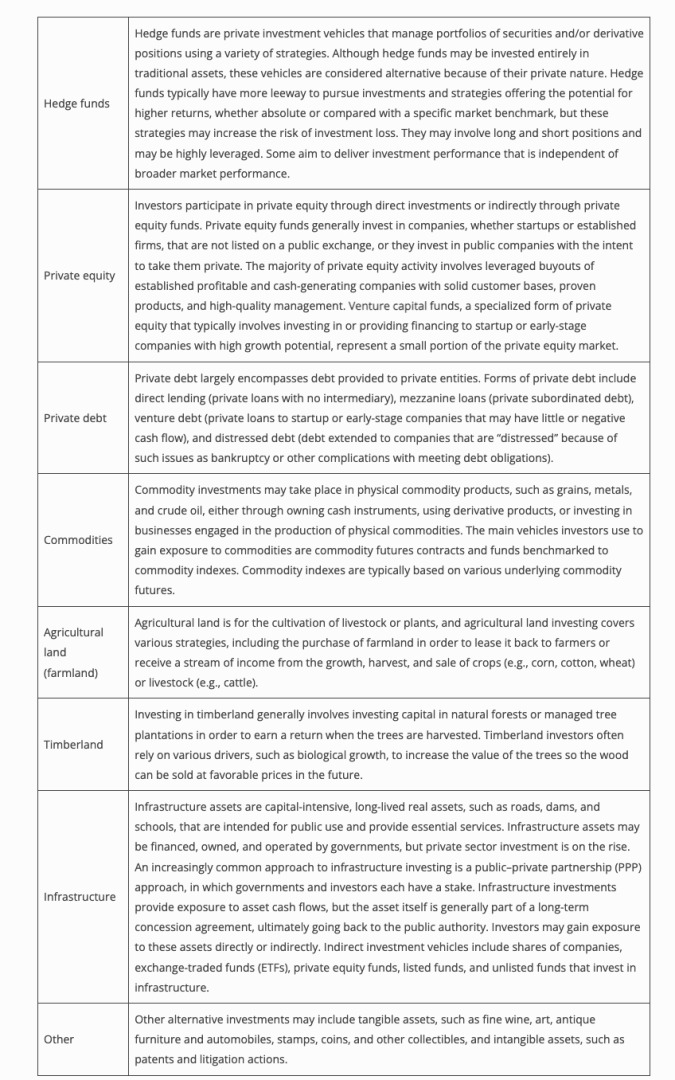

Alternatives encompass a wide variety of assets. In fact, it’s easier to describe what they are not than what constitutes one. Alternatives comprise most assets and strategies other than long-only, publicly traded stocks, bonds, and cash (a.k.a. “traditional” assets). Common types include private equity, venture capital, hedge funds, private debt, and “real assets”, like real estate, commodities, and even collectibles like wine and art.

While definitions vary, below are some general descriptions of common alternatives.

Source: CFA Institute, Introduction to Alternative Investments

While some alternative managers traffic in traditional assets like stocks, they can employ different tactics and tools in their investing. For example, alternative managers might use leverage, utilize derivatives, take short positions, and purchase illiquid and non-traded assets in their portfolios like stakes in start-ups. They may also hold more concentrated positions and limit investors’ abilities to redeem their stakes to certain times of the year.

However, the most common trait shared by alternatives is the way in which investors access them. Since they are not publicly traded instruments, constructing adequately diversified portfolios can be challenging. Alternatives are difficult to trade. Their prices aren’t listed on transparent exchanges. Buyers and sellers must first be found and then prices individually negotiated. As a result, investors frequently invest via funds with specialized managers, like private equity and venture capital firms, who provide liquidity, diversification, and expertise.

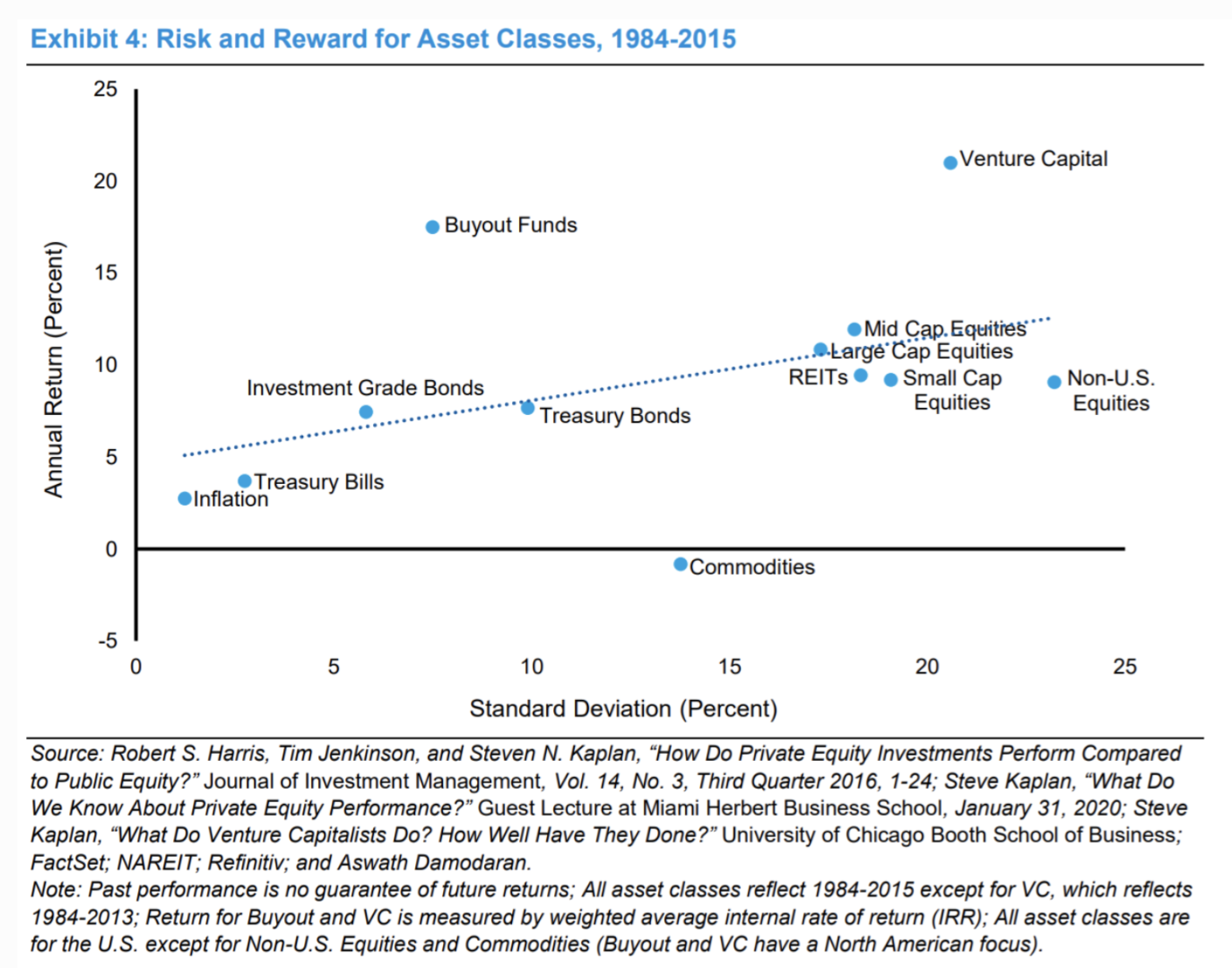

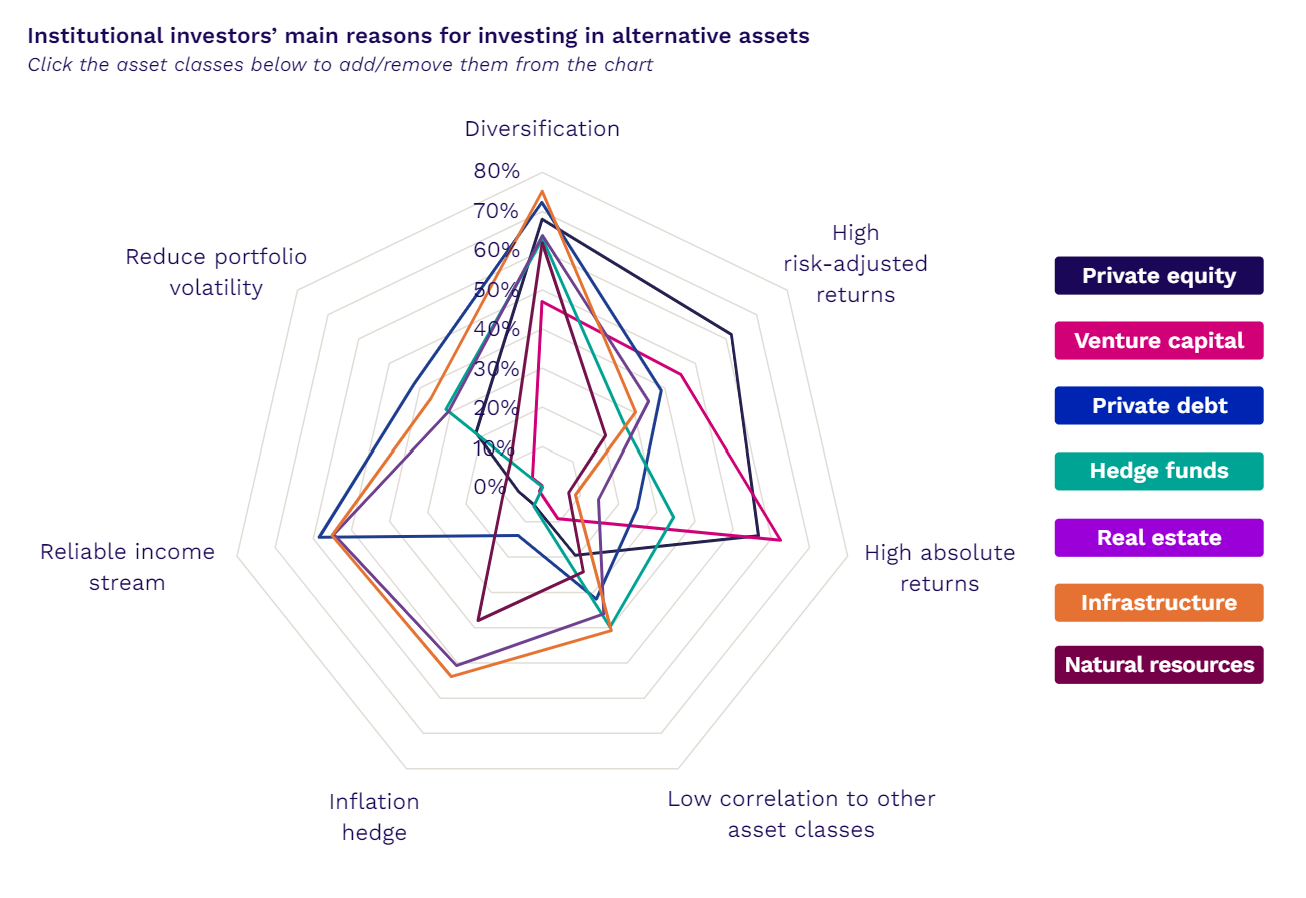

Investors allocate to alternatives for two primary reasons. Historically speaking, they offered higher returns than public securities. Including alternatives in a traditional portfolio also yielded diversification benefits due to their lower correlations with stocks and bonds. Thus, alternatives raised returns and dampened volatilities for investors—the Holy Grail of investing.

Alternatives like buyout funds and venture capital produced better risk-adjusted returns than other assets. Source: Morgan Stanley Investment Management

To be sure, these characteristics are hotly debated. Since prices for alternatives are not publicly available (or even exist!), assessing them with traditional, price-based risk measures is questionable at best. Alternative prices are often “marked” by their owners using models or benchmarking them to the available prices of comparable public securities. While acceptable, conflicts of interest are unavoidable. The desire to show superior performance could bias managers’ valuation processes. An alternative’s true market price might be lower and/or more volatile than holders might like. We simply can’t know for sure.

Some believe that alternatives’ price opacity fools investors into thinking that they are more beneficial than they really are. Greater price swings might reveal higher correlations to traditional assets and lower risk-adjusted returns, negating their alleged portfolio benefits. However, one study concludes that the manipulation of private equity returns is a feature demanded by investors rather than an undesired bug. Some investors want to be fooled.

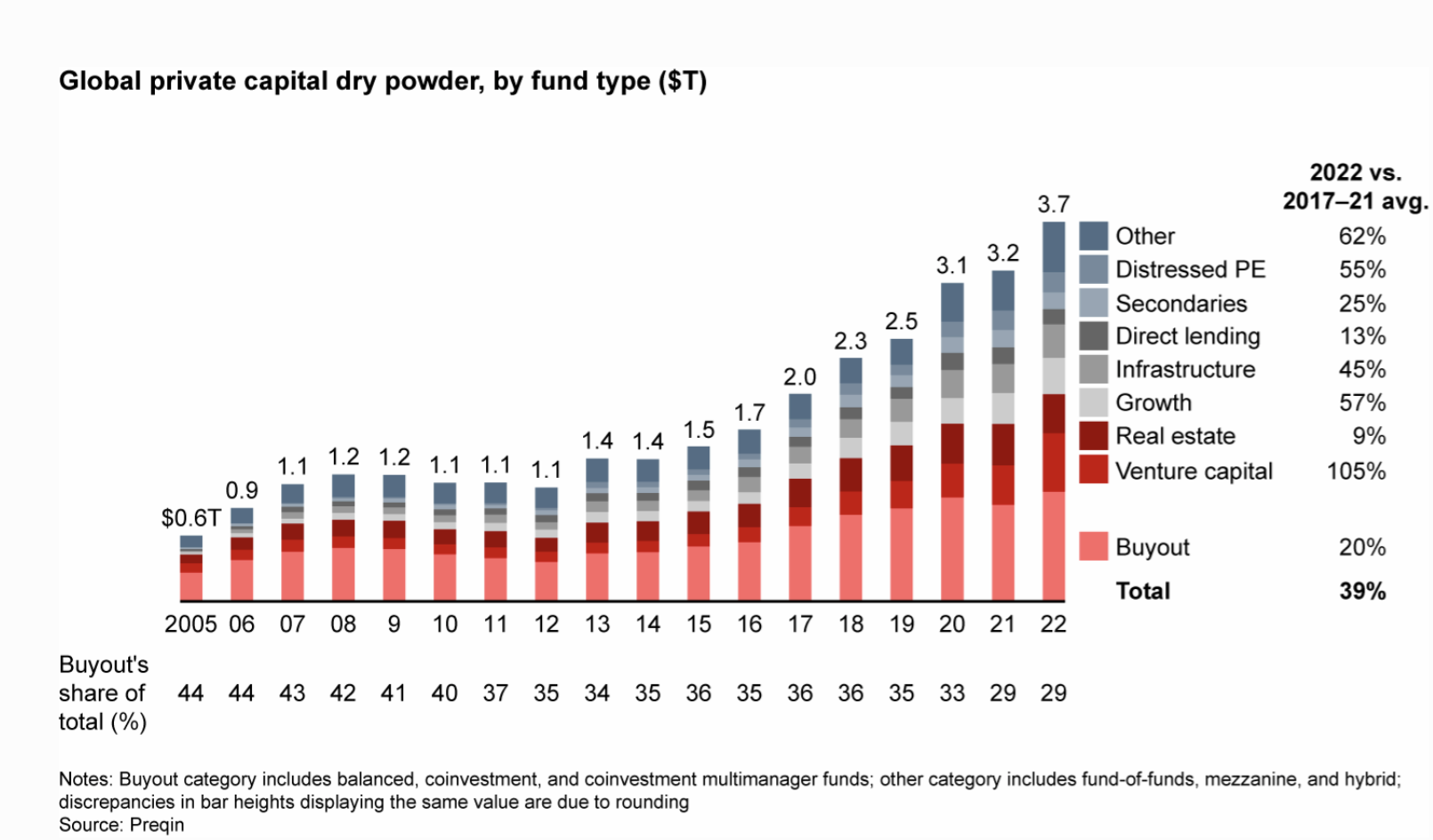

True or not, investors are increasingly allocating capital to alternative assets. Their inflows have continued to rise with their popularity. As a result, alternative asset managers can now access record amounts of capital that they will ultimately need to invest (or return to investors).

Alternative fund managers have record amounts of capital to invest. Source: Bain Private Equity Outlook in 2023

Investors typically attribute alternatives’ higher returns to several factors. One relates to market efficiency. Less participation creates opportunities for savvy investors to exploit mispriced trading opportunities. These can arise due to regulatory hurdles, such as accredited investor requirements, or practical barriers related to the large capital requirements for some strategies, like purchasing entire companies. Higher complexity, more esoteric assets, and less liquidity—or the ease of transacting in alternatives without materially disrupting prices—are other cited reasons.

Note, that none relate to the different investment risks that alternatives may carry. Rather, most link alternatives’ higher returns to certain market structures or dynamics surrounding these assets. Yet, diversification remains a key reason for investment. Exactly what risks are investors trying to diversify away?

At its core, investing is the process of making money from money, strictly through the purchase (or short-sale) of assets. Investors profit from cash flows contractually linked to assets—such as interest payments and dividends—their appreciation in value, or both. There’s no other way.

Thus, investors assume two types of risk for which they are compensated. The first is credit risk. Credit risk refers to the probability of a party failing to make a contractual payment. The most common kind relates to principal and interest payments on loans. However, credit risk also applies to derivative contracts—where parties agree to pay each other under specified conditions like changes in interest rates—lease agreements, and, to a lesser extent due to their optional nature, dividend payments. Note, that in this context, credit risk relates only to a party performing its contractual obligations, which for investing means making monetary payments.

The second risk investors assume relates to capital appreciation. In many cases, returns are generated from the rise in value of an investor’s asset. Stocks are the most common form of this. However, foreign exchange, commodities, and options profits also require rising asset prices. These assets don’t (materially) cash flow and appreciation is not contractually embedded. Thus, investors assume the risk that their stakes will rise in value and yield a profit, a characteristic I call equity risk.

Every instance of investing requires the assumption of equity or credit risk. Some types, like distressed debt, dividend stocks, and certain real estate properties, have components of both. However, none have none. Equity and credit risk are the sources of investor profits.

Note, that alternatives carry the same types of risks as traditional assets. Private debt investors assume credit risk like public bondholders; private equity and hedge fund managers hope their assets appreciate like listed stocks; publicly traded REIT stocks own similar assets as non-traded ones. Alternatives are not alternatives with respect to their investment risks. They differ only in the specific markets in which they operate (which are primarily illiquid ones).

Thus, I don’t consider alternatives a separate asset class worthy of distinct allocation. Rather, I see them as different flavors of investments. To be sure, their return profiles might vary from public stocks and bonds. However, they merely reflect their distinctive risk characteristics such as illiquidity. Don’t get me wrong, investors may still benefit from owning alternatives. My point is simply that to view alternatives alternatively, seems superficial.

To illustrate, consider an analogy to food. Humans require food to live like investors need assets to profit. However, it’s not food, per se, that sustains human life; it’s the nutrients food contains that do. Nutrients like Vitamin C, though, rarely exist on their own. Instead, we absorb them from what we eat. Human bodies require a variety of nutrients. Thus, we eat a variety of foods: meats, fruits, vegetables, dairy products, and grains.

However, foods taste differently depending on its preparation. Chicken can be roasted in an oven, smoked on a wood-burning barbeque, slow-cooked in wine, or sautéed in a curry sauce. Yet, the nutritional value of each will be similar. Thus, we have lots of choices when it comes to food preparation. Good cooks, however, don’t haphazardly combine flavors. They integrate them into particular cuisines to optimize the eating experience.

Health experts, though, don’t focus on taste. They concern themselves with macronutrient content for optimum health. It’d be silly for one to prescribe a weekly diet of 3 servings of Italian food, 5 French, 4 Chinese, etc. He/she would be focusing on the wrong element of health—taste—and neglecting the essential one (nutrition). While cuisine choices play an important role in eating, they are nonetheless optional.

Similarly, assets’ cashflows create investment returns, not the assets in and of themselves. Cashflows stem from credit and equity risk. However, investors can’t access these risks (and returns) in raw forms. Instead, we buy assets much like we eat food. Each asset has its own cashflow characteristics.

Rarely can a single type meet an investor’s every need. Thus, we construct portfolios containing many just like our diverse diets. Public stocks, private debt, real estate, commodities, hedge funds, and foreign exchange provide us with different options to achieve our investment goals like cuisines do for ingesting the nutritional content of food. By combining different assets, investors can create diverse sets of risk and return profiles.

Alternatives are an investment cuisine. While they share similar traits—mainly not being traditional assets—none are essential ones like credit and equity risk. Instead, alternatives’ similarities resemble qualities of taste. They are merely additional components to be used to construct different (and interesting!) portfolio flavors.

Investments in alternatives have grown rapidly over the years. Drawn to their higher (absolute) returns and professed portfolio benefits, investors redirected capital away from traditional assets like publicly traded stocks, bonds, and cash and into private equity, private debt, real estate, and the like.

While non-traditional, alternatives don’t possess unique investment characteristics; they’re just harder to buy and sell. Each contains a blend of credit and equity risk like their traditional counterparts. These two risk exposures are the primary source of investment returns.

Thus, treating alternatives as a distinct (and homogenous) asset class deserving of a portfolio allocation is backwards. Alternatives are akin to cuisines in food. They represent a style of investing and are as optional for portfolios as taste is for nutrition.

That said, I believe portfolios should be constructed like diets. They should be nutritious and delicious.

Cashflows come first but can be met with a variety of asset combinations that should integrate to serve the investor’s specific needs, built from the bottom up, not mandated from the top down. The best diets, of course, also taste good. However, no lunches are ever free.

Seth Levine is a professional, institutional investor focused on selecting high yield bond positions for a financial services company. He is also the creator of The Integrating Investor where he blogs about macroeconomic and investment strategy related themes. Seth holds a Bachelor of Science degree in Mechanical Engineering from Cornell University and is a CFA charterholder. You can learn more about Seth at www.integratinginvestor.com and follow him on Twitter at @SethLevine2. Please note that any opinions and views he expresses are solely his own and do not reflect those of his current or former employers.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest