Comments

- No comments found

While a U.S. Bitcoin ETF sounds good in theory, peek under the hood and investors will find a futures-based instrument riddled with contradictions that has very little to do with bitcoin anyway.

Considering that there’s an app for practically everything these days, it stands to reason that it was really only a matter of time before Wall Street lobbied Washington sufficiently to roll out its own version of bitcoin — the ultimate bitcoin app for institutional investors.

While many investors cheered the arrival of the ProShares Bitcoin Strategy ETF, the first U.S. ETF to feature all of the flavor of bitcoin, with none of the fat, bitcoin maximalists chuffed at its lack of real bitcoin inside its ETF shell.

Unlike some bitcoin ETFs in Europe and Canada, the American version is backed by bitcoin futures traded on the Chicago Mercantile Exchange, which themselves are cash-settled instruments.

But what’s the big deal?

To understand why a futures-backed ETF, especially one that is cash-settled, is a bit like saying a pop tart is full of fruit, it’s first necessary to understand what an ETF is in the first place.

In a nutshell, an ETF is a type of investment fund that can be traded on a stock exchange.

Similar to a mutual fund, the key difference between an ETF and a mutual fund is that shares in an ETF are bought and sold throughout the day as long as a stock exchange is open, whereas with mutual funds, these are bought and sold back to the issuer (also known as a redemption) based on the net asset value of the shares in that mutual fund at day’s end.

ETFs and mutual funds also differ in terms of liquidity.

Because the assumption is that having an open market like a stock exchange which any investor can plug into and buy or sell a security, ETFs are typically seen as more liquid instruments as compared to a regular mutual fund, which only has one liquidity provider of last resort, typically the issuer themselves.

But even before getting to understand what ETFs are, it’s important to get a glimpse into what caused them to exist to begin with.

Prior to 1993, there wasn’t an easy way for investors to purchase a single share that gave them exposure to a broad index of American stocks.

Think of an index like a buffet.

For most of us, there’s no conceivable way to stuff a full portion of every single dish at a buffet, but broken down to bite-sized chunks, it is possible to sample a wide variety of foods.

So is it with an index.

When the benchmark S&P 500 was created, it was intended as an index to represent a broad swathe of American companies and indirectly, the performance of the U.S. economy.

As soon as the index was created, there was a demand from investors, especially retail investors, to find a way to participate in such an index at relatively accessible ticket sizes.

The problem is that copying an index like the S&P 500 would be prohibitively expensive for an individual investor because they would need to hold shares of 500 American companies in the proportion of their weightage in the S&P 500 index.

Just one Google share alone would cost an investor almost US$3,000, while shares of Tesla, just over a thousand bucks, and even then we’re just getting started.

Complicating the matter, the composition of the S&P 500 is updated from time to time and investors who were trying to create their own version would need to stay on top of that as well.

Which is why in 1993, State Street Global Investors created the S&P 500 Trust ETF, called the SPDR or “spider” for short, which till today, remains one of the most actively traded ETFs, as a means to provide regular investors a way to gain that broad exposure, in a bite-sized chunk.

So now if an investor wants to buy an exposure to the stocks in the S&P 500, instead of needing to buy each individual stock, they can simply buy shares in the ETF, which will then use those proceeds to purchase the underlying shares, with a small fee for the service.

Investors in the ETF indirectly own the assets of the fund and will typically receive annual reports and a share of the profits such as interest, or dividends — as good as if the investors themselves owned constituent shares of the S&P 500 in their own right — and that’s an important distinction.

Whereas U.S. bitcoin ETFs invest in cash-settled futures, something like the SPDR actually buys shares of the very asset that it is intended to track.

When an SPDR ETF investor sells the ETF on the exchange, either another investor buys it, or the ETF issuer sells the underlying assets to realize the proceeds of that sale.

If more investors want to purchase more of an ETF, these additional funds will then be used to buy more of the underlying asset.

And in a nutshell, that’s what an ETF is.

Some of the largest ETFs have an annual fee of just 0.03% of the amount invested, which is a real steal, considering the amount of service that you get in return.

Since then, ETFs have been created for a whole range of assets, from commodities to stock indices and you guessed it, bitcoin.

Given their convenience and accessibility, it’s no surprise then that ETFs have soaked up a ton of investor dollars.

As of August this year, some US$9 trillion was invested in ETFs globally, with the U.S. accounting for some US$6.6 trillion alone.

The market for U.S. ETFs, at the risk of sounding lewd, continue to be the deepest and most liquid in the world.

So is it any wonder then that since as far back as 2013, cryptocurrency advocates have been pushing to list a U.S. bitcoin ETF?

But many of those early U.S. bitcoin ETF applications were for instruments that would actually hold bitcoin as the underlying asset, and shares of the ETF would track the value of the underlying bitcoin based on supply and demand for the ETF itself.

So far so good.

The problem of course was that the U.S. Securities and Exchange Commission wasn’t keen on allowing “physical” bitcoin to underpin an ETF because of concerns over potential manipulation of bitcoin prices by bitcoin “whales” as well as concerns over wash trading, where the same institution is on both sides of the trade.

Which is why when crypto and blockchain-savvy Gary Gensler took the helm at the SEC, expectations were high that he would give the greenlight to a U.S. bitcoin ETF.

Gensler did, just not in the way most crypto advocates would have hoped for.

Gensler still had the same concerns over a bitcoin ETF that actually held bitcoin and so the SEC greenlit a bitcoin ETF that held bitcoin futures instead, but not just any futures, CME Group’s cash-settled bitcoin futures.

Which brings us to another concept that U.S. bitcoin ETF investors have to understand — what are futures?

Essentially, a futures contract is a standardized legal agreement to buy or sell something at a predetermined price at a specified time in the future.

The first known futures exchange was the Dojima Rice Exchange of the Edo Period in Japan, in the early 17th century.

In the early 17th century, Japanese rice farmers needed a way to guarantee the price of rice when brought to harvest to help hedge against the risk of being a farmer.

Because there is a time lapse between when a farmer decides what and how much to plant and when the rice goes to market, prior to the invention of futures, the life of a farmer was one of constant feast and famine.

Is it any wonder then that farmers started off as some of the most superstitious people?

Because in years where harvest was bountiful, the price of rice would collapse, but in years with thin harvests, what little rice that they did bring to market attracted a premium.

Given these conditions, a Japanese rice farmer before the 17th century was just one more harvest away from financial ruin.

Rice futures contracts provided a possible way to hedge that risk altogether.

Investors could speculate on the future price of rice, while the farmer could sell the futures contract and was guaranteed a price for their produce come harvest time.

Between the time of physical delivery of the rice on the futures contract and the sale of that futures contract, the futures contract itself could be traded between investors, and so, the world’s first futures market was born, in the Dojima Rice Exchange.

Since that time, futures for a whole range of commodities have risen and have been used both as a hedging tool as well as an instrument for speculation.

But part of the complexity when it comes to the U.S. bitcoin ETF is that it invests in cash-settled bitcoin futures and not in bitcoin itself.

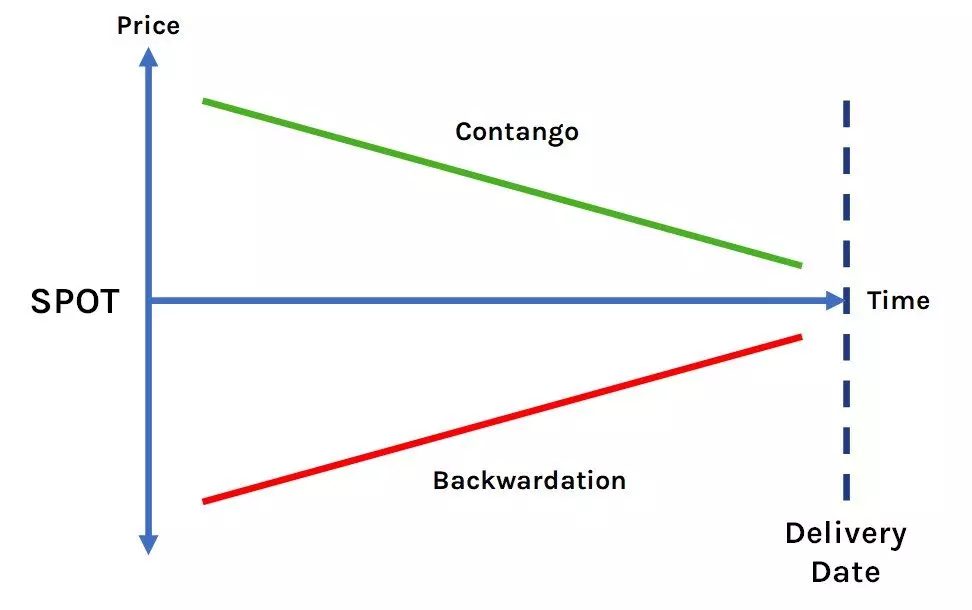

We’ll get to the cash-settled portion shortly, but let’s dive into some of the peculiarities with respect to futures first, starting with the concept of contango.

To understand contango let’s take a look at the following chart, where the horizontal axis represents time and the vertical axis is the price.

Contango is the situation where the futures price of the underlying asset is higher than the current spot price and can be caused by several factors, including inflation expectations.

So let’s take bitcoin for instance.

Forward futures for bitcoin may be trading at higher than the current spot price because investors are expecting that the price of bitcoin will rise in the future on inflation expectations.

Other factors like expected future supply disruptions, for instance a bitcoin halving (where the reward for mining bitcoin halves), could also see futures prices at a premium to the spot price.

But wait, there’s more.

Futures are also subject to a phenomenon known as backwardation, where the futures trades at a discount to the spot price.

Backwardation can occur as a result of a higher demand for an asset currently than the contracts maturing in the future through the futures market and the primary cause of backwardation is a shortage of the commodity in the spot market.

Since the futures price, whether in contango or backwardation converges as the futures contract nears its delivery date, when backwardation occurs, it favors investors who are net long on the underlying asset.

And therein lies the problem for investors in a bitcoin ETF that is underpinned by futures.

Because bitcoin futures lock in the price for the months ahead, the performance of the ETF can differ markedly from the spot price of bitcoin on any given cryptocurrency exchange.

In part, this is because the bitcoin futures being traded in the ProShares Bitcoin Strategy ETF utilizes CME Group’s bitcoin futures, whose prices are based on composites at five crypto exchanges.

Making matters worse, an ETF that relies on futures can and most likely will, underperform the underlying asset it is supposed to track.

Futures contracts expire on a fixed date and have to be “rolled over” into newer versions, the transaction costs and management fees for thousands of new contracts comes out of the ETF, acting as a drag on performance.

By one estimate from Refinitiv, the United States Oil Fund, a US$2.4 billion oil futures ETF has underperformed the price of WTI crude that it is supposedly meant to track, by a whopping 70% over the past decade.

According to Solactive, an index provider, bitcoin futures have made about 13% less than the cryptocurrency’s 120% rise so far this year, and while that may not seem like a lot, it adds up over time.

And all this comes on top of a 0.95% management fee.

But wait, there’s more.

Because the U.S. bitcoin ETF is intended to closely track bitcoin’s price, the most in-demand futures contract will be the one that expires closest to the current date, to try and avoid the contango and backwardation that affect futures.

These contracts, known as the front month or spot contracts will most closely converge with bitcoin’s current spot price and is the reason why ProShares holds all its 3,900 futures positions in November contracts.

But there’s a catch.

CME Group imposes limits on the number of contracts any one counterparty can buy, to prevent a single entity from cornering the market, especially because the market for bitcoin futures is relatively small.

When a counterparty hits the limit of 4,000 contracts, it has to buy longer-dated futures contracts, for which there are no limits, exposing investors to the phenomenon of backwardation and contango that we talked about earlier.

Because as long as the futures contract is not for the front month, spreads can really start to widen the further out a trader goes.

If the market expects the price of bitcoin to rise over the longer term, then the price of longer term futures contracts will rise above the short term contracts, or contango, incurring higher costs for the fund, when the futures contract is rolled into the next month and literally forcing the ETF to sell low (the front month contracts) and buy high (long-dated contracts).

These costs, also known as “roll costs” means that a futures-based bitcoin ETF will underperform the price of bitcoin itself, and industry estimates put the underperformance at between 5–10% per year making a bitcoin ETF that invests in bitcoin futures, more expensive for investors wanting to hold a position over the longer term.

And what does your money in a U.S. bitcoin ETF buy anyway?

Well for starters, these futures-based bitcoin ETFs aren’t even completely constituted of futures.

Around 25% of the ProShares Bitcoin Strategy ETF is made up of money on margin, while the remaining 75% will go into money-market instruments such as Treasury bills, constituting a hedge against resulting exposures.

Because a futures ETF will only give investors modest exposure to bitcoin via any ordinary brokerage account and returns will be eroded by the relatively high costs, investors who are looking to own bitcoin should just go ahead and buy it outright.

Which brings us to our final hang up when it comes to a bitcoin futures-based ETF — there isn’t any actual bitcoin involved in the entire ecosystem.

Considering that cryptocurrencies are a conceptual form of value, it seems somewhat disingenuous to then take an abstract of an abstract, hammer it into an ETF, and then declare it investable.

A futures-based bitcoin ETF is as far away from bitcoin as an Impossible Burger is to a cow, and therein lies the problem with the specific form of bitcoin futures selected for the U.S. ETF — a cash-settled futures.

At least with the Dojima Rice Futures, a futures trader could still have the option for physical delivery of the commodity — they could literally have their rice and eat it.

Not so with cash-settled bitcoin futures — all they are is a betting contract.

So all of that talk about bitcoin’s inflation hedging properties — poof, up in smoke like the value of the dollar.

So who are U.S. bitcoin futures for then?

Traders primarily.

Short term traders who are looking to get in and out quickly or fund a simple basis trade — buying spot and selling futures, can make a cool 30% per annum by arbitraging the wide spreads between forward futures and spot prices (at time of writing).

The other type of investors are institutions for whom buying bitcoin outright is simply not an option because it is outside their investment mandates.

According to JPMorgan, in the first two days of trading, retail investors accounted for only around 12% to 15% of net buying of the ProShares Bitcoin Strategy ETF, meaning that the bulk of buyers were institutional investors.

For global investors who want all the exposure of bitcoin, but none of the cryptocurrency, there are ETF products that hold the underlying bitcoin in institutional custody in Canada and Europe.

While it’s not clear if the holders of these ETFs have any redemption rights in the underlying bitcoin itself in a time of liquidation, at the very least, these ETFs that purchase and custody bitcoin are exerting buy-side pressure on the underlying asset.

But for retail investors who actually want to hold on to bitcoin for its alleged inflation-hedging properties, buying the bitcoin ETF makes little sense.

Institutional investors have little choice but to stay within the matrix, they have to take the blue pill, and for them their trip is over.

But for retail investors who want to genuinely have exposure to bitcoin, the red pill is the only option, they will need to apply themselves, figure out how to handle a bitcoin wallet, complete their KYC on a cryptocurrency exchange of their choice and buy and hold some actual bitcoin.

Patrick is an innovative entrepreneur and a lawyer passionate about cryptocurrencies and the business world. He is the CEO of Novum Global Technologies, a cryptocurrency quantitative trading firm. He understands the business concerns of founders and business people helping them to utilise the legal framework to structure their companies to take advantage of emerging technologies such as the blockchain in order to reach greater heights. His passion for travel, marketing and brand building has led him across careers and continents. He read law at the National University of Singapore and graduated with Honors in the Upper Division and joined one of Singapore’s top law firms, Allen & Gledhill where he was called to the Singapore Bar as an Advocate & Solicitor in 2005. He created Purer Skin, a skincare and inner beauty company which melds the traditional wisdom of ancient Asian ingredients such as Bird's Nest with modern technology. In 2010, his partner and himself successfully raised $589,000 from the National Research Foundation of Singapore under the Prime Minister’s Office. He has played a key role in the growth of Purer Skin from 11 retail points in Singapore to over 755 retail points in Singapore and 2 overseas in less than a year. He taught himself graphic design, coding, website design and video editing to create the Purer Skin brand and finished his training at a leading Digital Media Company.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest