Comments

- No comments found

One remarkable shift during and after the pandemic recession was a remarkable rise in the US savings rate.

This was was driven in part by the government spending programs enacted during the pandemic: the checks sent directly to households, the expansion of unemployment insurance, and the Paycheck Protection Program to help smaller businesses keep people employed. It was also driven by the fact that during the pandemic, options for spending money were limited both by various shutdowns (as an example, options for travel and entertainment were constricted) as well as by hold-ups in the supply chain.

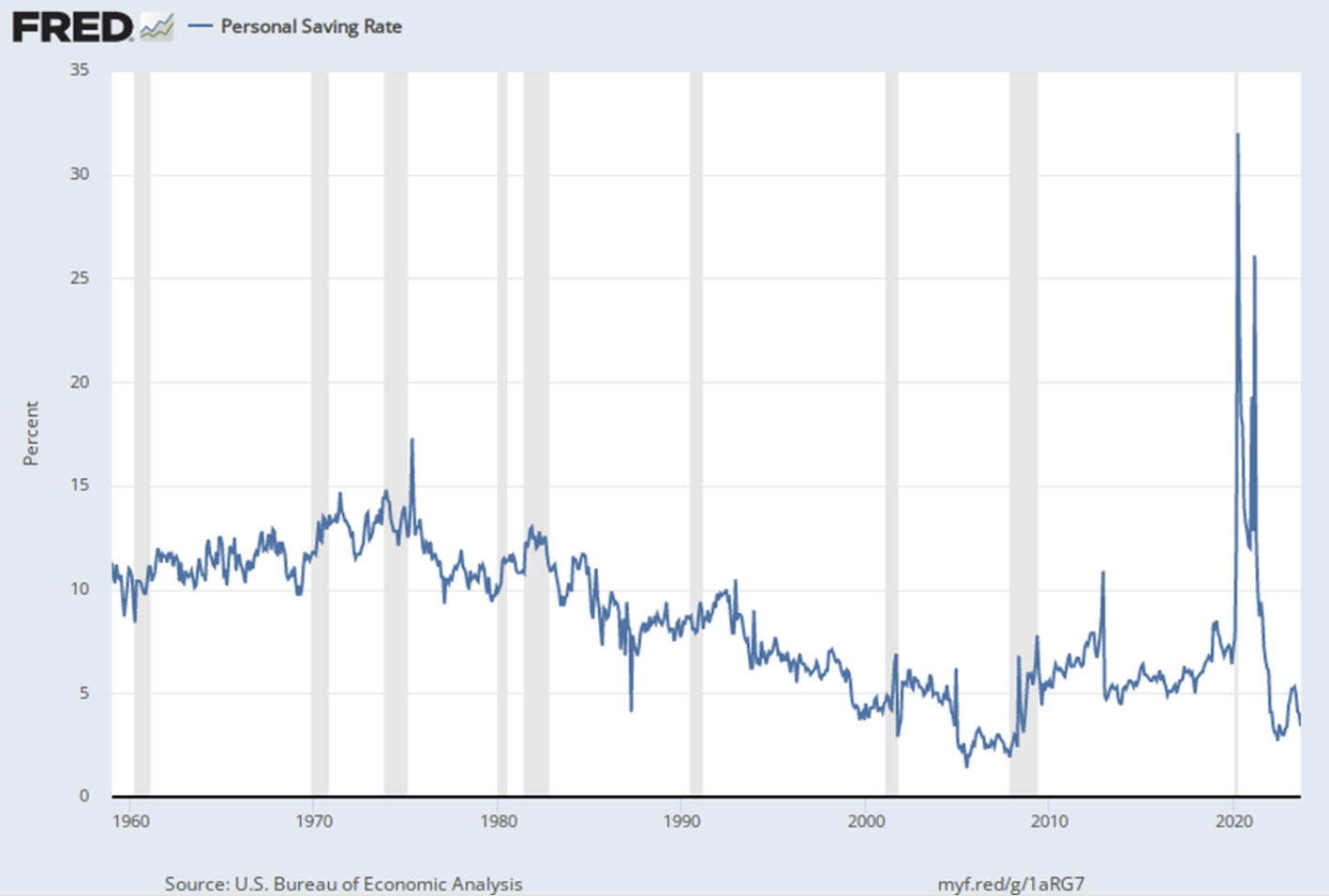

Here’s the US personal saving rate on a quarterly basis since about 1960. You can see the gradual decline from the 1970s up to the early 2000s (a story in itself for another time), and then what looks like a rising trend up in the lead-up to the pandemic. During the pandemic and its aftermath, the saving rate spike wildly, and then falls back to the below-average levels of the early 2000s.

Have American households mostly spent the savings their pandemic savings? Or are they still sitting on a substantial share?

The answers matter for a number of reasons. In a general sense, inflation is driven by “too many dollars chasing too few goods.” Households seeking to spend the federal spending largesse that had built up in their savings was one of the drivers that kicked off inflation in 2021. Thus, if households are still sitting on a cache of savings to be spent in the next year or so, inflationary concerns are larger than if households have mostly spent down their savings. Other topics like the labor force participation rate or the willingness of entrepreneurs to start new firms are also interrelated with whether households feel as if their cushion of savings is more than they plan to have in the long-run, or about right.

Omar Barbiero and Dhiren Patki of the Federal Reserve Bank of Boston have written a short “Current Policy Perspectives” essay on the question “Have US Households Depleted All the Excess Savings They Accumulated during the Pandemic?” (November 7, 2023). They point out that estimates vary widely of the extent of excess saving that remains. They argue that a main issue is how to interpret the modest-looking rise in personal saving that was already happening just before the pandemic. They write:

Most estimates of excess savings differ because of seemingly innocuous assumptions about the long-term saving trend in the US economy. Excess savings are now depleted only if we assume that households need to set aside a higher share of their income today compared with before the pandemic. If we assume instead that the underlying saving rate should be equal to the pre-pandemic average (6.2 percent), only slightly more than one-third of the excess savings has been depleted. Our new method for estimating excess savings across the income distribution allows us to assign excess dollars to a specific US county. After mapping counties to their income levels, we find that as of the end of 2022, most income groups still had access to significant amounts of savings and that there is no substantive difference in the savings-reduction rate across income groups.

Personally, I have a hard time looking at the US personal savings rate over the decades and believing that a permanent move to a savings rate well above the pre-pandemic average was underway. Thus, my sense is that households are still sitting on substantial savings accumulated during the pandemic that they would be willing to spend in the next few years.

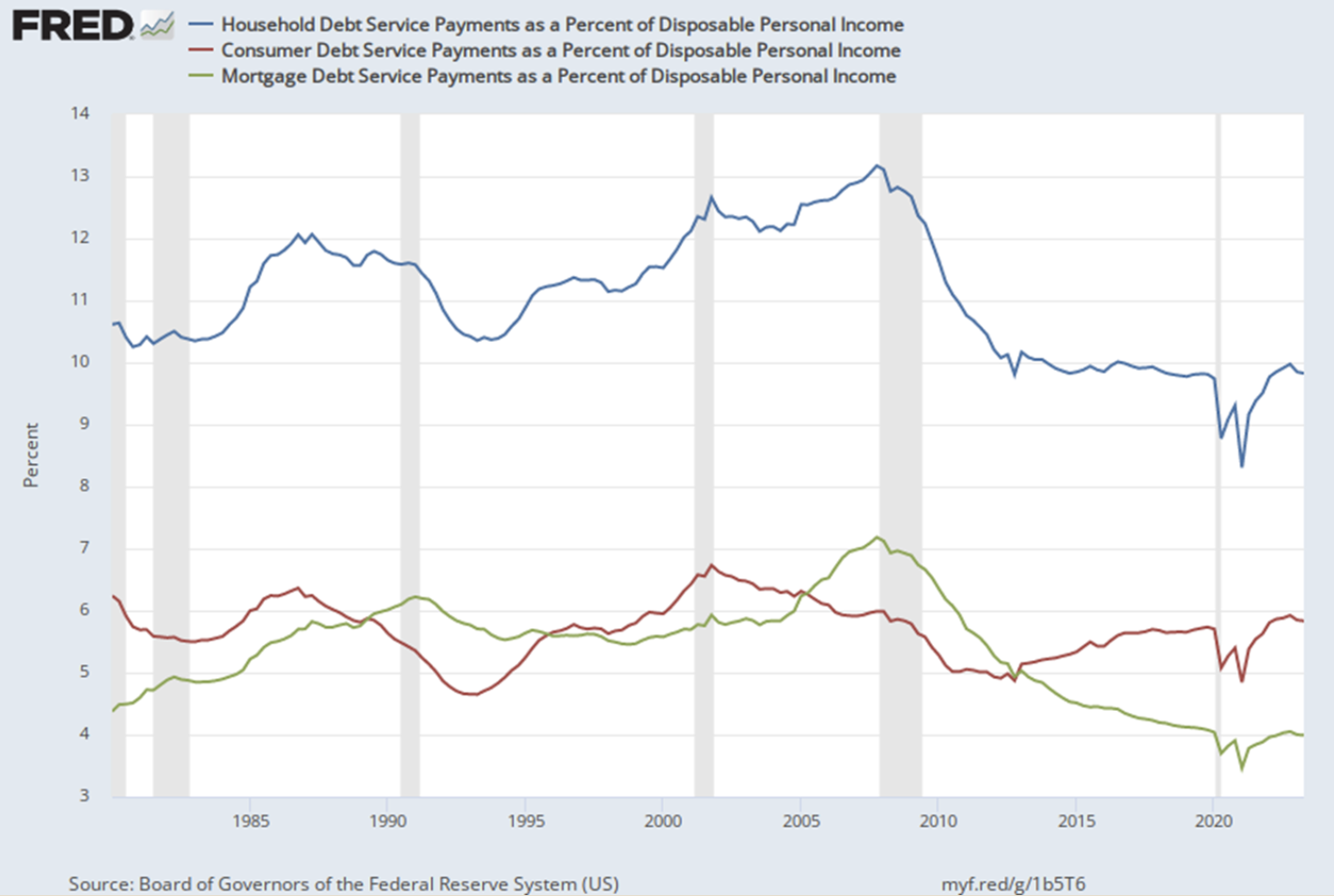

At least so far, it doesn’t appear that households are overly encumbered by debt, either. In the figure below, the top line shows total household debt payment as a share of personal income. The total can be broken into two parts: mortgage debt payments (the green line) and other consumer debt payments (the red line). The figure shows that mortgage debt payments ran up during the housing boom/bubble before the Great Recession, but have declined during the period of low interest rates since then. However, other consumer debt has stayed at about the same level since 2010 or so–and even seems to have increased a little.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest