Comments

- No comments found

When Medicare started, health care providers were reimbursed for the specific services they provided.

There was a Part A of Medicare which focused on inpatient hospital care (although it also includes aspects of skilled nursing care, hospice care, and home health care) and Part B of Medicare which focused on physician services (although it also includes ambulance care, some durable home medical equipment, some mental health care, and other services). But there is an obvious issue with fee-for-service care: the provision of health care services is shaped by the needs of the patient, but also by the local practice patterns and economic incentives of health care providers. Thus, although Medicare is a national program, and the payroll taxes to support Medicare are the same everywhere in the country, Medicare prices and services provided can vary considerably by location (for example, see here).

Thus, the next main change to the original structure of Medicare did not follow the fee-for-service approach. In 1997, President Bill Clinton signed a law establishing Medicare Part C, where Medicare patients could decide, instead of getting fee-for-service payments through Medicare A and B, to have the government direct payments to a private health insurance company–in effect, the government bought health insurance for you. This innovation wasn’t completely new: there had been some people getting their Medicare through private insurance going back to the 1970s. But in the late 1990s, the “Medicare Advantage” option, as Part C is often called, became available to all.

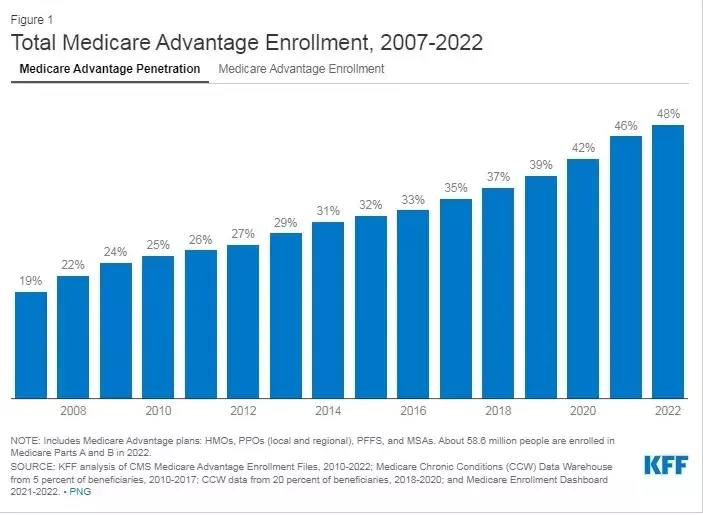

In a study done for the Kaiser Family Foundation, Meredith Freed , Jeannie Fuglesten Biniek, Anthony Damico , and Tricia Neuman look at “Medicare Advantage in 2022: Enrollment Update and Key Trends” (August 25, 2022). They point out that the share of Medicare enrollees signed up for Medicare Part C is nearly half and rising quickly. They cite projections Medicare Advantage may cover more than 60% of all Medicare patients 10 years from now.

Why are people choosing Medicare Advantage plans? The main reasons are that the insurance plan is required to cover everything in Medicare Part A and B, but it is also allowed to provide additional services–at no additional cost to the patient. Some common add-ons include certain vision, hearing, and dental services, and sometimes services like transportation to the doctor and subsidies for joining a health club. In addition, Medicare Advantage plans can be customized, so that they provide more coverage (say, lower co-pays) for the services you know you are more likely to use. In some areas, you can even make a fairly seamless transition from health insurance provided through your employer, by a certain company, to health insurance provided by Medicare, through the same insurance company.

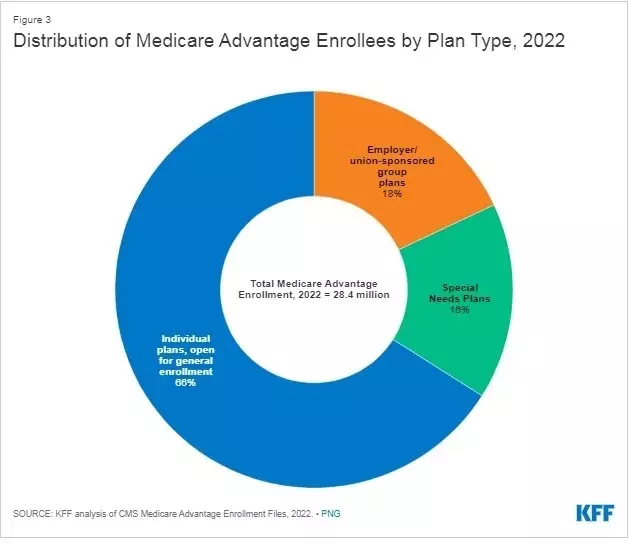

Most of the Medicare Advantage plans are open to anyone, although there are also specific plans organized through certain unions and employers, and also some “special needs” plans limited to the low-income elderly who also have certain chronic or disabling conditions.

The rise of Medicare Part C poses some conundrums for advocates of national health insurance programs.

For example, various versions of “Medicare for All” legislation have been proposed. In some versions, this would be a universal national health insurance plan run by the government. Whatever the merits or demerits of such a proposal, actual real-world Medicare is shifting to a choice of plans run by insurance companies, and only funded by the government. The elderly have a choice between having their health insurance administered by the US government or by a private insurance firm–and they are choosing the private firm. Considering the pros of a Medicare Advantage plan, many favour it more.

An obvious follow-up question is: How can the private insurance companies offer these Medicare Advantage plans–with limited but real choices of coverage along with additional services? Remember, most of the plans are open to all, so the insurance companies are not “skimming the cream” of signing up only the healthier elderly. Private insurance companies need to make a profit, while Medicare Part A and B do not.

I do not have a fully convincing answer here. It’s true that the government pays a little more for Medicare Part C, on average, than for Parts A and B, but it’s only about $300 per person per year, so that’s unlikely to be the main driver. My guess is that big insurance companies are better at managing health care costs, and perhaps no worse at managing paperwork and administrative costs. After all, the insurance companies are paid a flat amount per patient, rather than being reimbursed on a fee-for-service basis like traditional Medicare A and B. One can, of course, raise concerns about just how private insurance might seek to control health care costs. But again, the key point is that the elderly are increasingly showing by their actions that they prefer the Medicare Advantage plans, funded by the federal government, but run by private insurance companies.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest