Comments

- No comments found

Fintechs have introduced significant disruptions and competition to the traditional banking industry.

While they pose challenges, they also offer opportunities for traditional banks to adapt, innovate, and collaborate.

In the last few years, banks have suffered as fintechs have provided people with functionalities that were once unavailable to them.

Banks have been aware for some time that technological advancements have the potential to disrupt their business models and pave the way for technology conglomerates to enter the banking sector.

The fintech threat to banks has caused the latter to rethink its model of service delivery and administration.

Traditional methods of saving money consisted of depositing money into the bank and relaxing while our savings yielded interests over a span of time. While these banks operated using traditional methods, fintechs brought a wave of transformation that rang a bell of warning across the banking sector. One of the reasons that fintechs instantly gained fame is because of their ability to provide people with functionalities that traditional banks failed to offer. Fintech threat to banks became a harbinger for conventional banks across the globe, plummeting the business for conventional banks as traditional banking methods seemed to grow obsolete.

Even though banks have been the traditional method of making financial transactions and saving money, fintechs brought about a wave of insecurity among the bankers as conventional banking patterns started diminishing. Apart from eliminating traditional banking patterns, fintech organizations also focus on providing customers with functionalities that were previously unavailable.

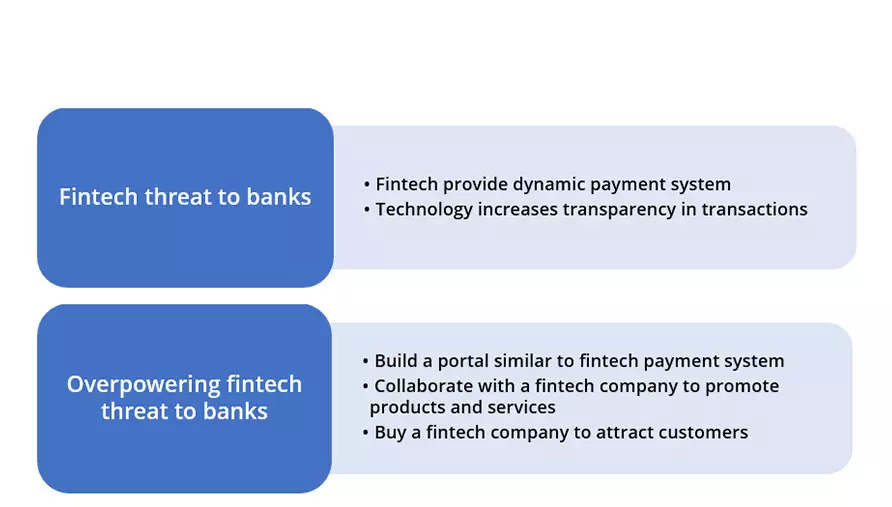

Fintech companies introduced dynamic payment systems that empowered their users to complete their financial transactions without the involvement of a middleman and curtailing transaction charges implied on them by traditional banks. The speed of transactions has also increased with these fintechs. Technologies such as blockchain in the finance sector have helped several fintech companies across the globe to achieve customer satisfaction and loyalty. This technology has helped fintech organizations in improving transparency of transactions in their payment systems which led to improved user interaction and experience.

Fintechs have disrupted the traditional banking landscape in many ways, but whether they are a "danger" to traditional banks depends on how both parties adapt to the changing financial landscape. Here are some key points to consider:

Fintechs have introduced innovative technologies and services that address various pain points in traditional banking, such as cumbersome processes, lack of personalization, and slow customer service. This has forced traditional banks to innovate in order to stay competitive. Fintechs have driven improvements in user experience, convenience, and efficiency within the financial sector.

Fintechs often excel at providing user-friendly digital experiences tailored to customer preferences. As a result, customer expectations for seamless and convenient banking services have risen. Traditional banks that fail to meet these expectations risk losing customers to fintech alternatives.

Fintechs have been able to cater to specific niches or underserved markets that traditional banks might have overlooked. This includes services like peer-to-peer lending, microloans, robo-advisors, and mobile payment solutions. Fintechs' ability to serve these niches has led to diversification in the financial services industry.

Rather than being solely adversaries, many traditional banks have recognized the potential benefits of collaboration with fintechs. Some banks have partnered with fintech companies to leverage their technological innovations, enhance their digital services, and expand their customer base.

Fintechs often operate within regulatory frameworks that can differ from those governing traditional banks. Striking a balance between innovation and regulatory compliance can be challenging. Traditional banks, with their established regulatory relationships, might have an advantage in navigating complex regulatory environments.

Traditional banks often have long-standing relationships and established trust with customers due to their history and reputation. Fintechs, especially newer ones, may face challenges in gaining the same level of trust, particularly with sensitive financial matters.

Banks can employ several strategies to effectively compete with fintech companies and maintain their relevance in the rapidly evolving financial landscape:

Traditional banks should adopt a culture of innovation and invest in research and development to create and implement new technologies. This could involve developing user-friendly mobile apps, offering digital payment solutions, and leveraging AI and machine learning for personalized financial services.

Fintechs often excel in providing seamless and convenient customer experiences. Banks should focus on improving their customer interfaces, streamlining processes, and offering personalized services that meet customers' evolving needs and preferences.

Banks can collaborate with fintech firms to leverage their expertise and technology. By forming strategic partnerships, banks can incorporate innovative fintech solutions into their offerings without starting from scratch.

Banks should work closely with regulators to develop frameworks that accommodate innovation while ensuring consumer protection and financial stability. An agile regulatory approach can enable banks to experiment with new technologies within a controlled environment.

Banks possess vast amounts of customer data. By harnessing this data responsibly and applying advanced analytics, banks can gain insights into customer behavior, needs, and preferences. This can lead to more targeted and personalized services.

Banks should recruit and retain professionals with expertise in technology, data science, and fintech. Having a skilled workforce is crucial for developing and implementing innovative solutions that can compete with those offered by fintech startups.

Banks need to undergo digital transformation to adapt to the changing landscape. This includes upgrading legacy systems, embracing cloud computing, and integrating modern technologies to provide efficient, secure, and user-friendly services.

Cybersecurity is a major concern in the digital era. Banks must prioritize robust security measures to protect customer data and financial transactions, ensuring trust and peace of mind for their customers.

Traditional banks can diversify their offerings to include a broader range of financial services, such as wealth management, insurance, and investment advisory. This can help them attract and retain a wider customer base.

Banks should educate their customers about the advantages of their services, including the security, stability, and regulatory oversight they provide. Clear communication about the benefits of traditional banking can help counter some of the fintech allure.

By implementing these strategies, traditional banks can position themselves as competitive players in the fintech-driven landscape, offering the best of both worlds: technological innovation and the trust and stability that come with their established reputations.

Naveen is the Founder and CEO of Allerin, a software solutions provider that delivers innovative and agile solutions that enable to automate, inspire and impress. He is a seasoned professional with more than 20 years of experience, with extensive experience in customizing open source products for cost optimizations of large scale IT deployment. He is currently working on Internet of Things solutions with Big Data Analytics. Naveen completed his programming qualifications in various Indian institutes.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest