Comments

- No comments found

The benefits received from the US Social Security system and the taxes paid have evolved over time, and the changes have not been the same across income groups.

The Congressional Budget Office describes some of the shifts in “CBO’s 2022 Long-Term Projections for Social Security” (December 16, 2022).

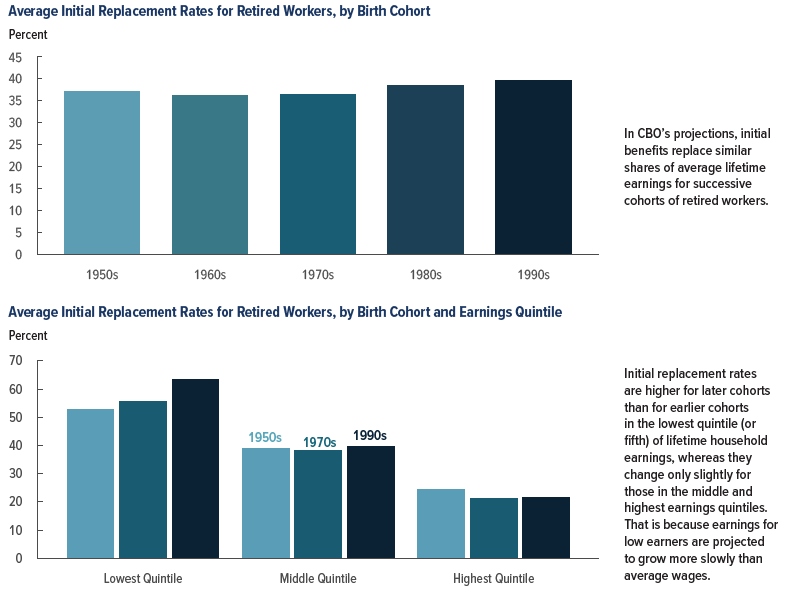

The top figure shows the initial average benefits received by a retired worker from Social Security, adjusted for inflation. It rises over time, because wages have gradually risen over time, which has also led to rising revenues from payroll taxes, and thus (by formula) to higher benefits. The bottom panel is a breakdown by income level, for those born in the 1950s (and thus retiring now) along with projections for those born in the 1970s and 1990s. Again, because Social Security links your payroll taxes to your benefits received, albeit with some degree of redistribution from higher to lower incomes, those in the upper quintile of incomes will receive higher Social Security benefits.

A different way to look at this data is in terms of “replacement rates”–that is, what share of your previous earnings is being replaced by Social Security, and how has this amount shifted over time. The top panel shows that over time, the average replacement rate hasn’t changed by much. The bottom panel shows that the replacement rate for those with lower incomes is higher than for those with higher incomes. This isn’t a surprise, because the Social Security taxes are capped at a certain income level ($147,000 in 2022), so the program is not designed to have a high replacement rate for those who consistently have income above that level. You also notice that in the current design of the program, the replacement rate is rising for those with lower incomes, and falling for those with higher incomes.

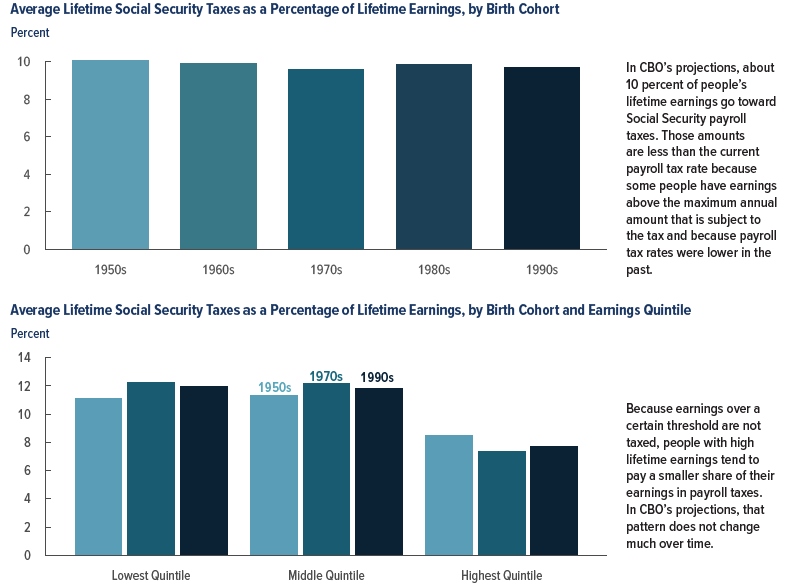

Here’s a view from the tax side, showing Social Security taxes as a share of lifetime income. The calculations make the standard assumption that Social Security taxes “paid” by the employer are actually “paid” by the employee in the form of lower wages. Again, the average share doesn’t change much over time. Those with lower income levels pay a higher share of lifetime income in Social Security taxes, because they don’t hit the annual income ceiling for these payroll taxes.

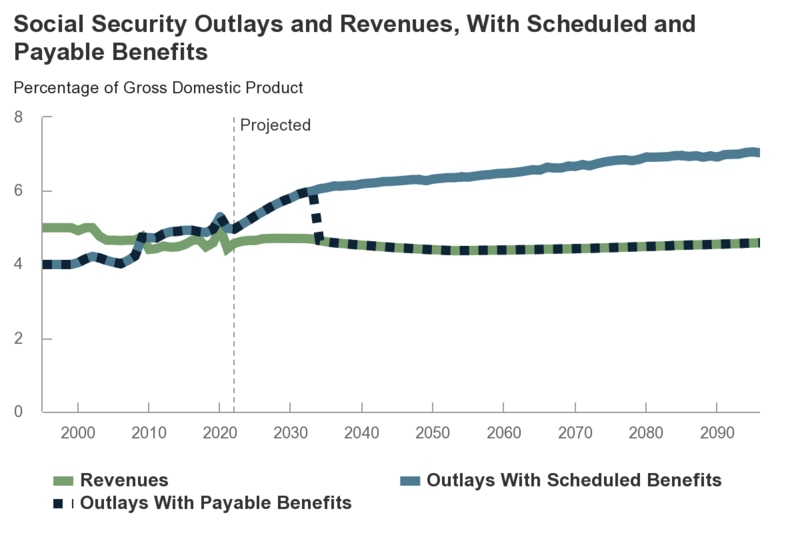

Of course, the ultimate evolution of Social Security by cohort is that the system is financially unsustainable under current law. During the 1980s and the 1990s, the Social Security system took in more in payroll taxes than it paid out in benefits. The idea was to build up a trust fund, so that when the “baby boomer” generation born in the 15 year or so after World War II started retiring in force around 2020, there would be funds to cover that demographic transition–at least for a few decades. During 2010, Social Security spending caught up with revenues, and as the ratio of America’s elderly to workers rises, Social Security spending kept rising, too. The trust fund that was built up in the 1980s and 1990s runs out in 2033, on current estimates. There will still be payroll taxes incoming to pay for some benefits, but not enough to pay for what has been promised.

I’ve written often enough in the past about the need for solutions (for example, here) but as other writers have pointed out, it seems more likely that our political parties will wait until the insolvency of the system is upon us before taking action. Why solve today what you can put off for tomorrow? In addition, a sizable share of Republicans only want to fix Social Security if they can turn at least part of it into a system of private retirement accounts, and a sizable share of Democrats only want to fix Social Security if they can include substantial increases in the payments made to the elderly poor. For both groups, actually fixing the existing system comes second behind other priorities–at least until the insolvency hits. Meanwhile, those of us who paid higher payroll taxes in the 1980s and 1990s to buy extra time for the retirement of the post-World War II “baby boom generation through the 2010s and 2020s are looking at a system that won’t have the funds to cover the promises made for our own retirements in the 2030s. It’s enough to make a person feel cynical.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest