Comments

- No comments found

Sometimes you start working on a project, and it turns out to be more timely than you had expected.

Back in October 2019, the Hutchins Center on Fiscal & Monetary Policy at the Brookings Institution and the Initiative on Global Markets at the University of Chicago Booth School of Business formed a Task Force on Financial Stability. At the time, I suspect it seemed like a worthy effort that would produce what a friend of mine used to call “good gray books”–where the adjective “gray” referred not to the cover but to the excitement quotient. But then the pandemic hit, and in March 2020 a series of real challenges to financial stability erupted. Thus, when the report came out in June 2021, it could be less about whether the financial stability problems of 2007-9 had been addressed, and more about the evident weaknesses remaining in the US financial system.

(For the record, the members of the task force were Glenn Hubbard, Donald Kohn, Laurie Goodman, Kathryn Judge, Anil Kashyap, Ralph Koijen, Blythe Masters, Sandie O’Connor and Kara Stein.)

The question of “financial stability” basically focuses on this problem: When bad times hit, as they will do now and then, does the financial system keep performing its tasks pretty well in a way that helps ameliorate the crisis, or is the financial system staggered in a way that can propagate the original crisis and make it worse? For example, do loans still get made? Are financial transactions still carried out briskly? Do prices of financial assets fall by a reasonable amount, given the economic bad news, or is there a “fire sale” rush-for-the-exits dynamic that depresses prices very sharply or even makes some assets nearly impossible to sell for a time, until the market situation clarifies and stabilizes?

These issues of what is sometimes called “financial plumbing” are not intrinsically exciting. Like real-world plumbing, the importance of financial plumbing becomes most clear when it has broken down. Regular maintenance on the financial plumbing, by anticipating possible breakdowns, is of high importance.

The good news from the US financial system in the aftermath of the pandemic recession is that the banking sector looked very solid. In the aftermath of the Great Recession in 2007-9, various laws and regulations “it built the banking sector’s strength and resilience through more demanding capital and liquidity requirements as well as rigorous stress tests of the largest banks. … The banking sector, reflecting the effects of earlier reforms, remained resilient and met extraordinary demands for credit created when the interruption of economic activity caused by the pandemic sharply cut business cash flows.” The pandemic recession didn’t lead to plaintive calls from big banks that they needed just one more set of bailouts.

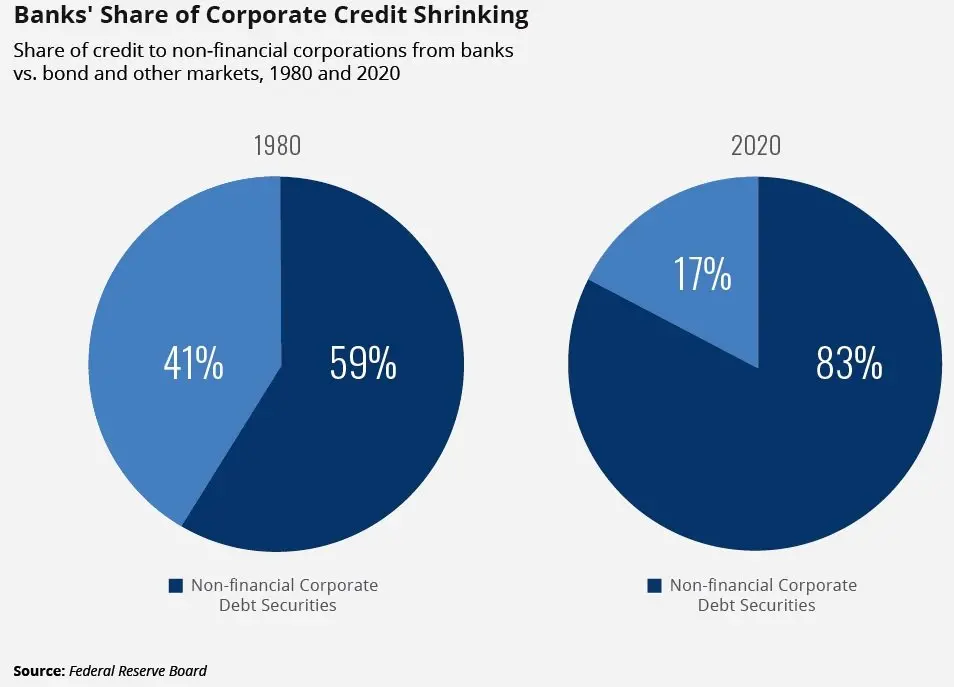

However, one tradeoff of making the banks safer is that an increasing amount of the US financial system now happens outside banks in the “non-bank” sector. Here’s one symptom of that change: it used to be that companies borrowed from banks, but now that banks are more highly constricted, companies borrow using the bond market or syndicated loans that are sold to investors instead.

One of the main reasons that investors hold US Treasury debt is that it is a safe asset, which means that when times go bad and you need cash, you can plan to sell off some of the Treasury debt without worrying that it might lose its value. But in March 2020, the US government wanted to dramatically increase its sales of Treasury debt (to fund additional government spending) at the same time that many private investors and central banks around the world also wanted to sell some of their holdings of Treasury debt and move to cash. For a moment or two, there even seemed to be a risk that the US Treasury would not be able to sell debt as planned–which would have led to chaos throughout global financial markets as investors changed how they value the outstanding $22 trillion or so in Treasury debt. The Federal Reserve stepped in:The report devotes separate chapters to risks in five parts of the non-bank financial system: the market for US Treasury securities, mutual funds, insurance companies, housing finance, and “central clearing counterparties.” The report has details: here, I’ll just offer a few words about each one.

In response, the Federal Reserve purchased more than $1.5 trillion in Treasuries in March and April. By contrast, in the quantitative easing program it undertook in 2012 and 2013 to spur economic recovery from the Global Financial Crisis, the Fed was purchasing $45 billion of Treasury securities each month. The purchases in 2020 were undertaken specifically to “restore market functioning,” the Fed said.

The market for US Treasuries did not crash. But emergency last-minute rescues by the Fed are not the first-best policy option. There are serious arguments that the entire method of selling Treasury debt through a series of private-sector dealers needs to be revamped.

Insurance companies manage a large pool of assets, so that they will have the funds available to pay claims during the next major natural disaster. They typically invest in assets like corporate bonds and Treasury debt. But when the pandemic hit, and corporate bonds dropped in value, the stock values of the big insurance companies also dropped (after all, their financial assets were worth less). The state-level regulators of insurance companies thus began to sound alarms about the safety and solvency of these firms. Thus, the insurance companies wanted to back away from writing new policies or from providing a supply of finance to capital markets–right at a time when many companies needed to borrow.

A similar problem arose in money market funds in March 2020. Those funds typically invest in corporate bonds (remember, companies don’t raise much money by borrowing from banks any more). But in a sudden pandemic, investors worry that companies are likely to default, and the price of those bonds falls. Investors in the money market funds start pulling out their cash. But there is a “maturity mismatch” here: investors can often pull out their money from a money market fund whenever they wish, but the money market fund is holding longer-term corporate bonds, and in the pandemic recession it can only sell those bonds at a loss. There is a risk of a run on the money market fund, similar to a bank run, where investors sprint to withdraw their funds before the value of financial assets behind the fund declines. In the meantime, money market mutual funds are not again harder for firms.

We learned during the Great Recession of 2007-9 that housing finance is closely entangled with the broader economy as a whole. Most housing finance now proceeds through non-bank firms, which bundle borrowing into mortgage-backed securities and sell the securities to big investors–like the money market mutual funds and insurance companies already mentioned, as well as to pension funds, banks, and others. The pandemic recession raised a risk of a spike in the number of mortgage defaults. There for a time less willingness to extend such loans and the value of mortgage-backed securities–remember, these are the financial assets held by other major players throughout the financial system–dropped. As the report notes: “The effects of the COVID-19 recession were cushioned by the Federal Reserve’s unprecedented intervention in the market for agency mortgage-backed securities. However, liquidity strains in the non-agency securities and loan markets disrupted mortgage credit supply. Widespread failures of nonbank mortgage servicers did not materialize, largely because of emergency government intervention. Emergency actions are not a permanent solution and do not address the underlying issue.”

There are two main ways of organizing markets for financial derivatives: “over-the-counter” markets and centralized clearinghouses. In an “over-the-counter” market, financial firms buy and sell with each other directly. One problem with such a market is that it can be hard to see overall patterns in the market as a whole. Thus, a common response in the aftermath of the Dodd-Frank act of 2010 was for a change so that buying and selling financial derivatives would happen instead through a central clearinghouse:”The largest derivative CCPs include divisions of CME Group, Intercontinental Group, and the London Stock Exchange Group.” But of course, a central clearinghouse also has a potential problem: what if under the stress of a negative financial shock, the clearinghouse itself stops being able to operate, or even goes bankrupt? After all, most clearing operations use a business model where sales happen “on margin,” with the buyer putting down only a percentage of the ultimate price, and then making adjustments later. There is a “default fund” if things go wrong. But if the price of financial assets move sharply and unexpectedly and certain players in the financial markets can’t meet their obligations and the default fund isn’t big enough, the clearinghouse itself could conceivably go broke, with potentially dire consequences for the smooth operation of the financial sector and the economy as a whole.

The basic answer to all these financial problems in March 2020, as I have already hinted, was massive intervention by the Federal Reserve. The Task Force report notes:

Under these circumstances, central banks had to intervene with massive and extraordinary actions to restore the functioning of these markets and preserve the access to credit of households, businesses, and governments. The Federal Reserve purchased huge amounts of Treasury and agency securities and agency mortgage-backed securities; it opened special liquidity facilities for securities dealers, for money market funds, for businesses that had lost access to commercial paper markets, and for businesses and state and local governments that encountered problems accessing bond markets. To meet heightened international demands for dollar liquidity, the Federal Reserve increased the size of its dollar swap lines with foreign central banks and expanded the list of central banks with access. In these facilities, the Fed sends dollars to foreign central banks temporarily and gets foreign currency in return. That enables foreign central banks to meet the dollar needs of their own banks. The Fed also established a repo facility for international monetary authorities, in which it lent for a short period against Treasury collateral so that foreign institutions could avoid selling their Treasury securities outright.

The economic recession part of the pandemic (as opposed to the larger public health and economic readjustment parts) was only two months in length, so the short-term Fed fixes were sufficient to help the US financial system through its turbulence. But it seems important to consider the stability of the non-bank financial sector before the next negative economic shock hits.

Timothy Taylor is an American economist. He is managing editor of the Journal of Economic Perspectives, a quarterly academic journal produced at Macalester College and published by the American Economic Association. Taylor received his Bachelor of Arts degree from Haverford College and a master's degree in economics from Stanford University. At Stanford, he was winner of the award for excellent teaching in a large class (more than 30 students) given by the Associated Students of Stanford University. At Minnesota, he was named a Distinguished Lecturer by the Department of Economics and voted Teacher of the Year by the master's degree students at the Hubert H. Humphrey Institute of Public Affairs. Taylor has been a guest speaker for groups of teachers of high school economics, visiting diplomats from eastern Europe, talk-radio shows, and community groups. From 1989 to 1997, Professor Taylor wrote an economics opinion column for the San Jose Mercury-News. He has published multiple lectures on economics through The Teaching Company. With Rudolph Penner and Isabel Sawhill, he is co-author of Updating America's Social Contract (2000), whose first chapter provided an early radical centrist perspective, "An Agenda for the Radical Middle". Taylor is also the author of The Instant Economist: Everything You Need to Know About How the Economy Works, published by the Penguin Group in 2012. The fourth edition of Taylor's Principles of Economics textbook was published by Textbook Media in 2017.

BBN Times connects decision makers to you. Experts in their fields, worth listening to, are the ones who write our articles. We believe these are the real commentators of the future. We quickly and accurately deliver serious information around the world. BBN Times provides its readers human expertise to find trusted answers by providing a platform and a voice to anyone willing to know more about the latest trends. Stay tuned, the revolution has begun.

Leave your comments

Post comment as a guest