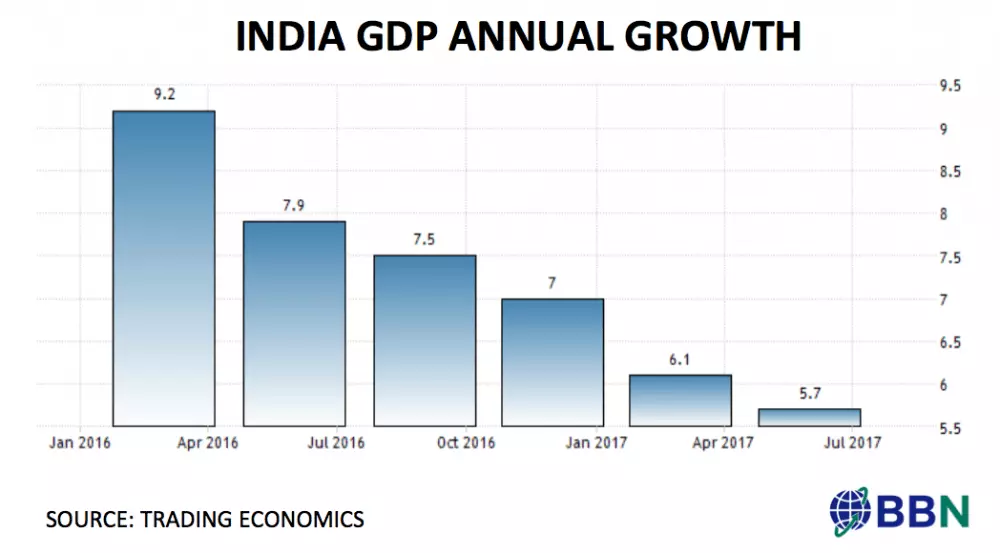

A year into the demonetisation decision, India's growth has tumbled only faster - It had come in at 6.6% in the October-December 2016 quarter, but has been at 5.6% in the two quarters that followed. While it can be argued that the real economic impact of the initiative was thus felt post Q3, 2016-17, the fact of the matter is that the impact had started becoming visible even earlier on as I argue in this post based on the talk. Appended below is the original.

Decoding the Growth Mystery

India’s economic growth numbers for the October-December 2016 period have been subject to much discussion in the past days, given that they were expected to encompass the impact of the demonetisation drive that was announced on November 8, 2016. However, since the time that the numbers have been announced, the air has been rife with confusion on how good or bad they are. This post is an attempt to clear some issues:

#1. Has growth been impacted by de-monetisation? There is only one answer to that question: Yes. Initially, there were report of India’s growth numbers coming in at 7%. By the looks of it, that sounds fairly robust, especially when you compare it with forecasts that suggested that growth will be down to 6%. However, this is not the right number to look at. This is the figure for GDP at market prices, while the accurate figure to look at is Gross Value Added at basis prices, which is a change in terminology that came about with the last base (and methodology) revision and has caused much confusion since. GVA at basic prices came in at 6.6%, not nearly as robust. Further, this is the slowest growth in 7 quarters.

One way of measuring whether growth is robust or not, is to compare it to trend growth. Unfortunately, given the still limited data available on growth with respect to the 2011-12 series, making it a somewhat difficult exercise. Further, rough trend growth for the Indian economy is 7.2% based on estimates that combine trends from the old and the new series. Therefore, the latest growth numbers are down by at 0.6 percentage points from that level. If the entire decline is not explained by demonetisation, at least some part of it is.

#2. But does this mean that the forecasts were wrong? A look at the latest numbers only, seems to suggest that they were. But the fact of the matter is that, there have been revisions to numbers starting all the way to the start of 2014-15 as per the latest release. Since forecasts were based on these unrevised numbers, the results were different. If the base numbers had not been revised downwards, growth in the latest quarter would have been at 6.3%, which is almost 1 percentage point down from the trend growth rate for the economy. In fact, without the base revision this would be the first time in 7 quarters that growth is significantly below 7%. (It was at 6.9% in Q3, 2015-16 but that is close enough to 7%). The only answer to this sharp decline has to be explained by an out of the ordinary impetus, namely, demonetisation.

#3. Which segments have been clearly impacted by demonetisation? There is a clear impact on the services sector from the latest numbers. The services sector grew by 6.8%, the slowest rate in 11 quarters. The last time the sector grew by a slower rate was in Q4, 2013-14 when it increased by 5.4%. In terms of specific sub-segments within services, ‘Finance, insurance, real estate and professional services’ grew by a particularly low rate of 3.1%, the lowest growth rate seen in this sub-segment since the start of the new series growth rates in 2012-13. The fact that it accounts for almost 19% share in GVA, suggests the impact of a softening on overall growth. In fact it is instructive to look at growth from a counter-factual perspective. If the sub-segment had grown at the average rate of 9% witnessed over the past 4 quarters, the services sector during this quarter would have grown by a whole 9.1% as opposed to 6.8% now. The overall economic growth would have been 7.7% - a whole 1.1 percentage point higher than what has been seen now.

#4. Is de-monetisation the only factor playing on growth this quarter? The fact that there are counterbalancing factors at work during this quarter have kept growth relatively buoyed this quarter. These are: (i) A strong agriculture season and (ii) Festive season demand. A good southwest monsoon has meant that agriculture production has been strong for the Kharif season. This is seen in 6% growth in agriculture, which too is the highest ever witnessed as per the new series as well. In this case too, it is instructive to see how growth would have turned out if agriculture had grown at a slower rate of 4% (account for a low base effect of -2.2% growth during the corresponding quarter of the previous year), overall growth would have fallen by 40 basis points to 6.2%. Coming to the second point on festive season demand, the fact that consumer expenditure is strong during the quarter – the highest in 17 quarters to be exact, at 10.1%, the overall growth number has been significantly supported. This also ties in with strong agriculture growth, which has likely provided an impetus to the rural economy, resulting in an exceptional increase in overall growth. Further, government spending growth has also been quite strong, in fact, the highest ever at 19.9% in the new series, which explains the support to overall growth.

#5. Can we take the numbers at face value? This is the underlying question in many minds since the growth numbers have come out. How far can we believe the numbers that have been put out? We would not dismiss the numbers without doing a thorough analysis on them. Here’s why. Our own proprietary measure – the Orbis Economics Consumer Conditions Measure – which has a strong correlation with private final consumption expenditure numbers, had shown a sharp uptick in Q3, 2016-17, and therefore we are more inclined to believe the consumption numbers than not. What we would like to see more details on are the industry number for Q3, 2016-17. Industry numbers have come in at 6.6%, the fastest growth in three quarters. While part of this was expected on account of the festive season, the fact remains that industrial production still suggests weakness and with raw material or commodities’ prices inching up in the recent months, the margins have likely been squeezed. As a result it is not clear what underlying factors are at play here. We will have to wait for consolidate corporate earnings for Q3 to be made available to assess the scenario. Till such time, however, we would like to hold back speculation on the veracity of the numbers.

#6. A little digression: The larger question, though around numbers, is how valid they are for a long time. The last number we had for the old series was in Q2, 2014-15. Just a comparison of the two series suggested that the new series were playing up growth. Which might be right. In fact, the CSO has explained many of the changes made as well. But doubts continue to persist. And these doubts will continue until analysts looking at the economy have historical data to work with. Unfortunately, that data is available only from 2012-13 onwards even now. Second, revisions to previous data in India are almost made by stealth, finding their way into new data sets or not as and when new accounts are released. It would do a whole lot of good to have separate releases for previous data or at least announce them in the releases as is done in the case of some monthly numbers like IIP and CPI. Also, we still don’t have details of the segmental details, which would help a lot in analysis.

#7. Does the government itself believe that demonetisation has not impacted the economy? I very much doubt that. Here we need to distinguish between political speak and actual on the ground actions. Despite a recent dig at Harvard and Oxford economists made by the PM, the Union Budget seems to reflect otherwise. In fact, let us take a step back to even before the budget, to the Economic Survey numbers. The survey had itself state that on account of the demonetisation drive, growth could slow down to 6.75-7.5%, with the lower part of the range actually being lower than the 7.1% number forecast by the CSO earlier. In fact, even 2 of the tax related policy moves by the government, namely, reduction in corporate income tax rate to 25% from 30% for companies with a turnover of up to INR 50cr as well as a reduction in personal income tax rate to 5% from 10% for the income tax slab of 250,000-500,000 is likely a tacit acknowledgement of the loss on account of demonetisation and a way of making up for it.

#8. So what is the upshot? Growth has undoubtedly weakened – and to sub-7% levels. The way to look at demonetisation’s impact is to see where growth could have been if not for demonetisation. Our analysis suggests that it would have been closer to 8% than the present 6.6%. Therefore, the analysis that the move has in fact shaved off at least percentage point from growth is not wrong. What is wrong, however, is the level growth predicted, which were based on everything else being equal and had not taken into account the spike due to seasonal demand.

Leave your comments

Post comment as a guest